Assessing AZZ (AZZ) Valuation After A Strong Multi Year Share Price Run

AZZ Inc. AZZ | 126.38 | +0.10% |

AZZ stock: recent performance snapshot

AZZ (AZZ) has drawn fresh attention after a strong run in recent months, with total return around 41% over the past year and roughly 2.5x over three years.

With the share price at US$137.46 and a 90-day share price return of 40.78%, recent momentum has been strong and complements AZZ’s 43.04% 1-year total shareholder return and 252.73% 3-year total shareholder return.

If AZZ’s strong run has you thinking about what else is moving, it could be a good time to scan our 24 power grid technology and infrastructure stocks as a fresh source of ideas.

After such a strong run and with AZZ trading near its analyst price target, the key question now is whether the stock still trades at an attractive valuation or if the market is already pricing in future growth.

Most Popular Narrative: 2.3% Overvalued

AZZ’s most followed narrative pegs fair value at about $134.33, which sits a touch below the last close at $137.46 and frames the recent rally against a slightly richer valuation.

The analysts have a consensus price target of $125.889 for AZZ based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $141.0, and the most bearish reporting a price target of just $105.0.

Curious what sits behind that tight gap between fair value and the current price? The narrative leans on modest revenue growth, softer margins and a higher future earnings multiple. Want to see exactly how those moving parts are stitched together into that valuation call?

Result: Fair Value of $134.33 (OVERVALUED)

However, investors also need to weigh weather-related production disruptions and rising competition, either of which could pressure margins and call this valuation story into question.

Another angle on valuation

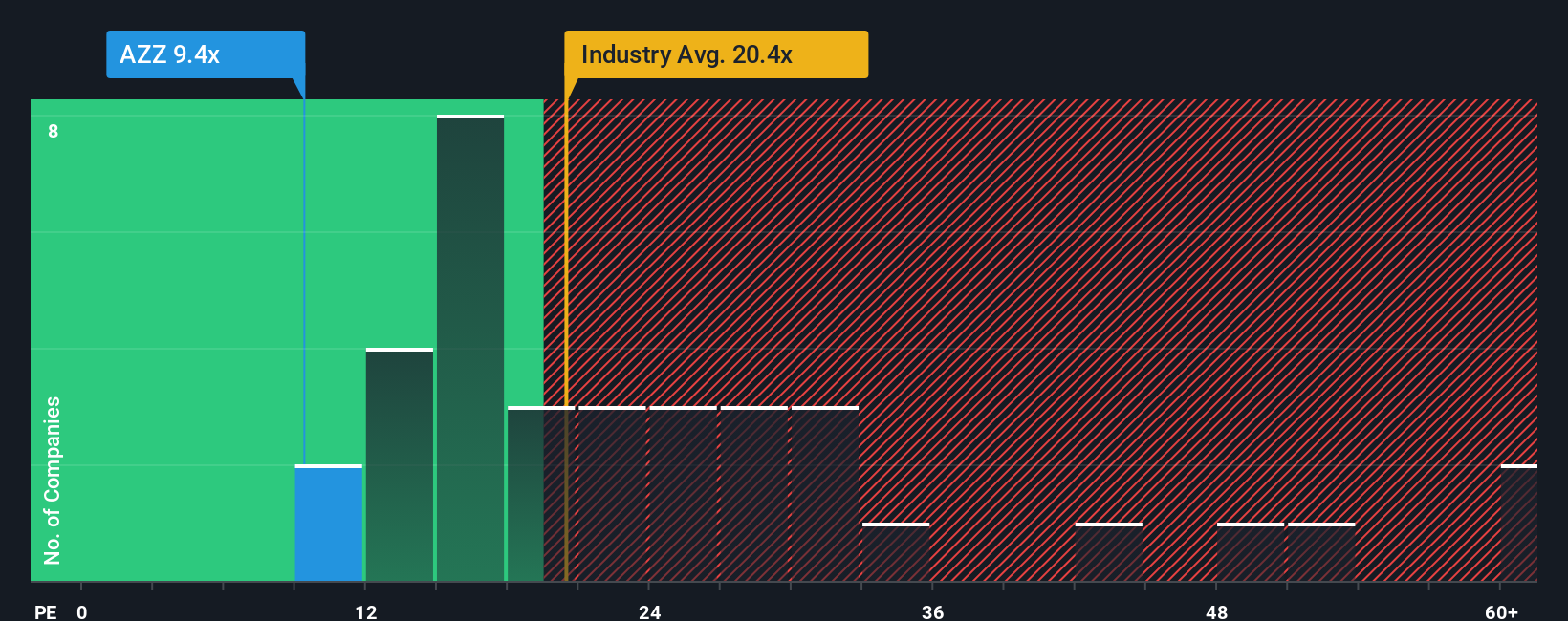

The narrative describes AZZ as about 2.3% overvalued compared with a fair value estimate of $134.33. At the same time, its P/E of 12.8x appears low relative to the US Building industry at 23.8x, the peer average at 47.6x, and even its own fair ratio of 12.9x. This raises the question of whether the current price reflects more risk than these comparisons indicate.

Build Your Own AZZ Narrative

If you look at these numbers and reach a different conclusion or simply want to test your own assumptions, you can build a personalized view of AZZ in just a few minutes, starting with Do it your way.

A great starting point for your AZZ research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If AZZ has sharpened your focus, do not stop here. Use these screeners to quickly surface focused ideas that fit different investing styles before the next move.

- Spot potential mispricing opportunities early by scanning our 51 high quality undervalued stocks that combine earnings power with balance sheet strength.

- Strengthen your income watchlist by reviewing our 13 dividend fortresses for companies offering higher yields with an emphasis on resilience.

- Reduce portfolio stress by checking our 85 resilient stocks with low risk scores that highlight businesses with steadier risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.