Assessing Becton Dickinson (BDX) Valuation After New Biologics Syringe And AI Research Platform Launches

Becton, Dickinson and Company BDX | 154.51 | -1.17% |

Becton Dickinson (BDX) has been in focus after two product announcements: a 5.5 mL Neopak XtraFlow syringe for large volume biologics, and the global launch of BD Research Cloud 7.0 with AI driven panel design tools.

The recent syringe development with Ypsomed and the launch of BD Research Cloud 7.0 come as Becton Dickinson trades at US$201.79, with short term momentum softening after a 2.1% 1 day share price decline but a 90 day share price return of 8.6%. Over longer periods, total shareholder returns of 15.3% over 1 year and around 15% over 3 and 5 years indicate that recent share price gains have not yet translated into strong longer term outcomes for holders.

If these healthcare product launches have your attention, this could be a good moment to widen your watchlist with healthcare stocks.

With Becton Dickinson trading close to analyst targets yet sitting on a 39% modeled intrinsic discount, plus weak one-year and multi-year returns, is this a reset that creates an opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 1.5% Undervalued

The most followed narrative puts Becton Dickinson’s fair value at about $205 per share, just above the recent $201.79 close, framing a relatively tight valuation gap.

The pending separation of the Biosciences and Diagnostic Solutions business will transform BD into a pure play medical technology leader with a consumables heavy portfolio (>90% of revenue). This is expected to enable higher cash flow predictability and margin improvement, while anticipated aggressive share buybacks directly support EPS growth.

Want to see what underpins that reset story, the margin rebuild, and the buyback assumptions, without guessing the numbers yourself? The full narrative lays out the revenue path, profitability targets, and valuation multiple needed to support that fair value.

Result: Fair Value of $204.83 (UNDERVALUED)

However, the reset story could be challenged if tariff and trade pressures, or a bumpy Biosciences and Diagnostics separation, hit margins harder than analysts anticipate.

Another Take: Earnings Multiple Sends A Caution Signal

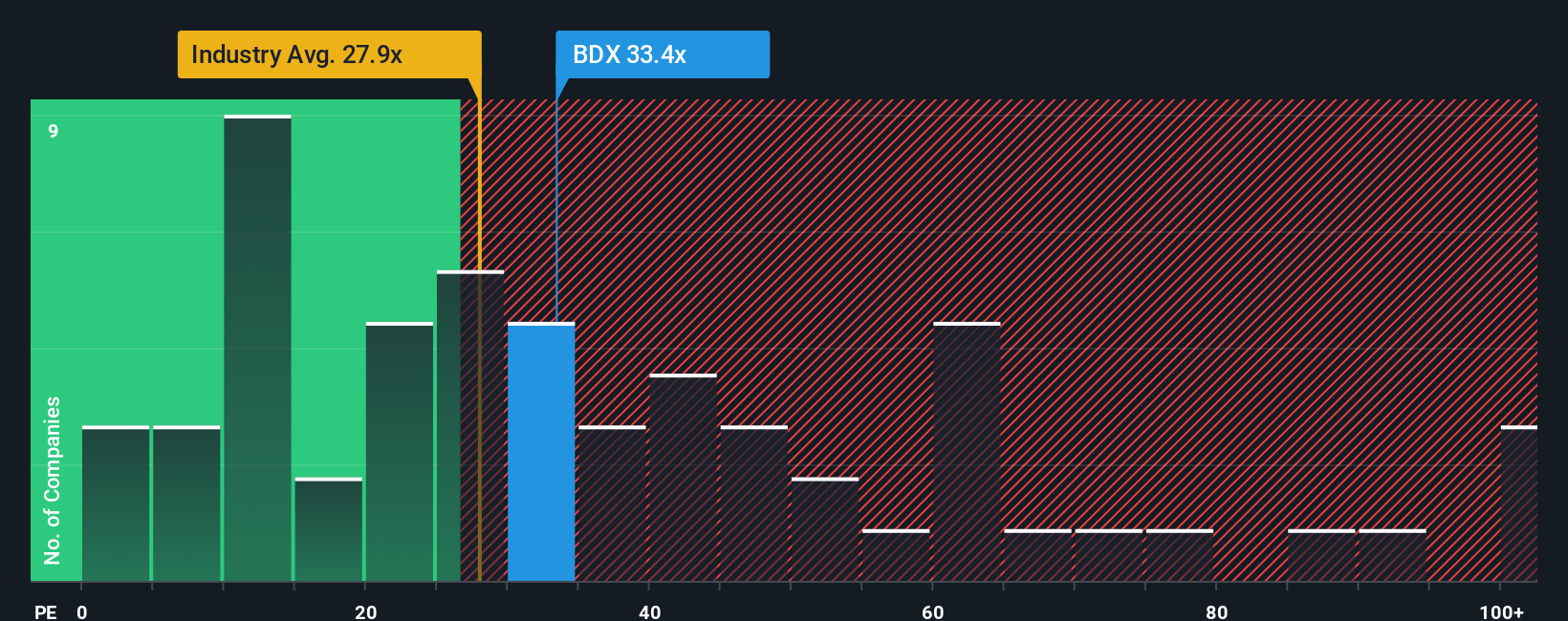

While the narrative and SWS DCF work point to Becton Dickinson trading at a 38.7% discount to fair value, the P/E picture is less comfortable. At 34.3x earnings, the stock is priced above its fair ratio of 33.6x, the US Medical Equipment industry at 32x, and peers at 33x. This suggests there is less margin for error if growth or margins undershoot.

Build Your Own Becton Dickinson Narrative

If you see the numbers differently, or would rather stress test the assumptions yourself, you can build a complete Becton Dickinson story in just a few minutes: Do it your way.

A great starting point for your Becton Dickinson research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Becton Dickinson is on your radar, do not stop there. Use the same framework to quickly spot other opportunities that might fit your style.

- Scan for income candidates and compare payouts with these 13 dividend stocks with yields > 3% that may suit a portfolio built around regular cash returns.

- Target potential mispricings by reviewing these 864 undervalued stocks based on cash flows where prices and estimated cash flows look out of sync.

- Get ahead of sector shifts by checking these 18 cryptocurrency and blockchain stocks that link equity markets with digital asset themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.