تقييم شركة كالوميت (CLMT) بعد خسائر الربع الأول ومخاطر تنفيذ مشاريع الطاقة المتجددة

Calumet, Inc. CLMT | 0.00 |

لفتت شركة كالوميت (CLMT) أنظار المستثمرين بعد إعلانها عن نتائج الربع الأول من عام 2026. وسجلت الشركة مبيعات بلغت 1,029.7 مليون دولار أمريكي، وخسارة صافية أكبر بلغت 317 مليون دولار أمريكي، ويعزى ذلك جزئياً إلى اضطرابات تشغيلية.

لم تؤثر خسائر شركة كالوميت في الربع الأول على زخم نموها بشكل كامل، إذ بلغ عائد سعر السهم خلال 90 يومًا 16.81%، وعائد سعر السهم منذ بداية العام 68.13%، بينما بلغ إجمالي عائد المساهمين خلال عام واحد 132.30%. يشير هذا إلى أن المستثمرين ما زالوا يعيدون تقييم التوازن بين إمكانات نمو الطاقة المتجددة والمخاطر التشغيلية.

إذا لفت انتباهك هذا النوع من قصص التحول، فقد يكون من المفيد مقارنتها بشركات أخرى ومعرفة ما يميزها في قائمة تضم أفضل 20 شركة يقودها مؤسسوها.

مع ارتفاع سعر السهم بقوة خلال العام الماضي وتداوله بنحو 13% أقل من أهداف المحللين، فإن السؤال الرئيسي هو ما إذا كان السعر الحالي يعكس بالفعل طموحات شركة كالوميت في مجال الطاقة المتجددة أم أن التقلبات الأخيرة قد خلقت فرصة محتملة للمستثمرين.

الرواية الأكثر شيوعًا: 40.2% مبالغ في تقييمها

عند إغلاق نهائي عند 32.87 دولارًا مقابل قيمة عادلة سردية تبلغ 23.45 دولارًا، يشير الإطار الأكثر متابعة إلى تقييم مرتفع ويعتمد بشكل كبير على زيادة إنتاج الوقود المتجدد.

يسير مشروع MaxSAF 150 على المسار الصحيح لبدء التشغيل في النصف الأول من عام 2026، مما سيمكن شركة Calumet من إنتاج 120-150 مليون جالون سنويًا من وقود الطيران المستدام (SAF) بتكاليف رأسمالية منخفضة نسبيًا، وتحقيق علاوات تتراوح بين 1 و2 دولار/جالون مقارنة بالديزل المتجدد، والاستفادة من الطلب المتزايد على وقود الطيران المستدام الإلزامي والطوعي على مستوى العالم؛ ومن المرجح أن يؤدي ذلك إلى زيادة كبيرة في الإيرادات وتوسيع هامش الأرباح قبل الفوائد والضرائب والإهلاك والاستهلاك بمجرد بدء التشغيل.

هل ترغب في معرفة مقدار الزيادة المتوقعة في الإيرادات، وتغير هامش الربح، ومضاعف الأرباح المستقبلية التي تستند إليها هذه القصة، وكيف ترتبط هذه الافتراضات بقيمة السهم العادلة؟ النتيجة: القيمة العادلة 23.45 دولارًا (مبالغ في تقييمها).

لكن هذا يتوقف على استمرار دعم الجهات التنظيمية وبقاء أسواق الدين متاحة. فأي تراجع في السياسات أو انتكاسة في التمويل قد يُهدد سريعاً هذا التفاؤل بشأن القيمة العادلة.

زاوية أخرى للتقييم

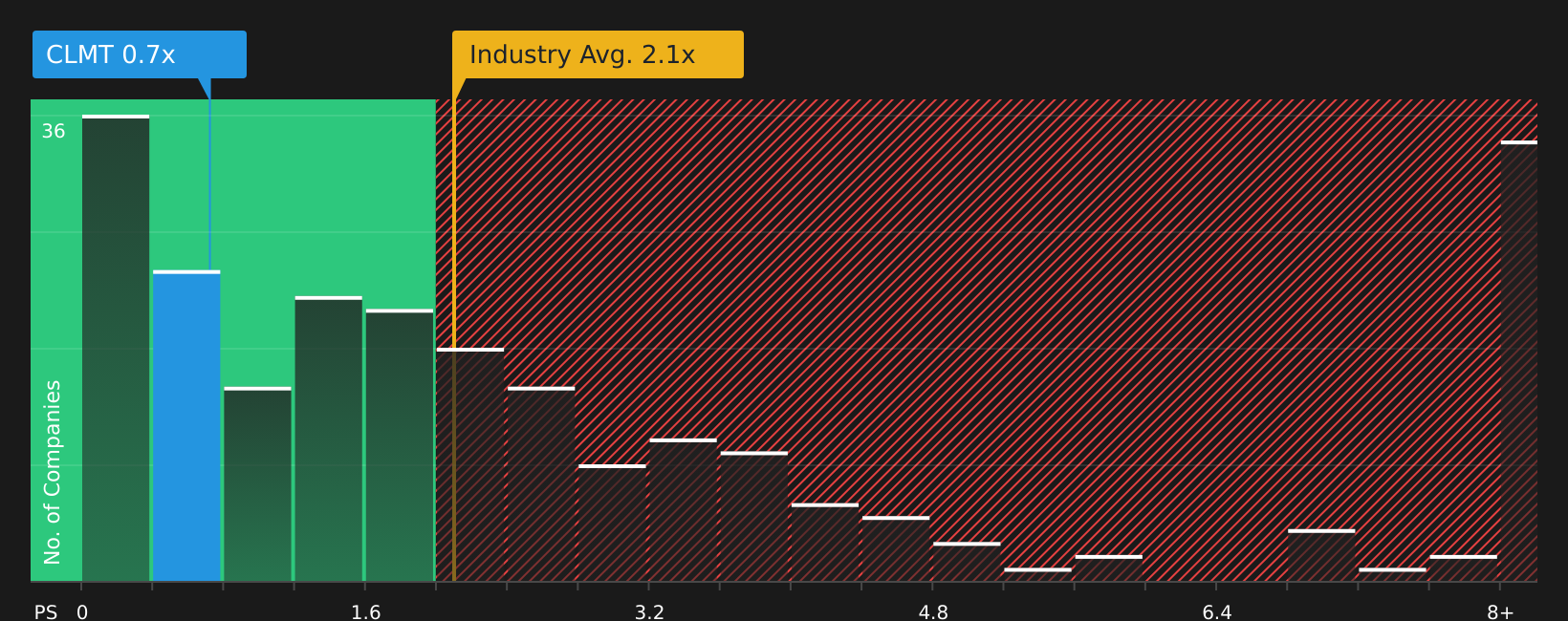

يشير السعر العادل المُقدّر بـ 23.45 دولارًا إلى أن سعر سهم كالوميت مُبالغ فيه، لكن نسبة السعر إلى المبيعات ليست واضحة تمامًا. فعند 0.7 ضعف المبيعات، يُتداول السهم بأقل بكثير من متوسط قطاع النفط والغاز الأمريكي البالغ 2.1 ضعف، ولكنه أعلى من متوسط نظرائه البالغ حوالي 0.2 ضعف، ويتماشى مع النسبة العادلة البالغة 0.7 ضعف. هذا المزيج من الخصم والعلاوة يطرح سؤالًا بسيطًا: هل يُقلل السوق من شأن مخاطر كالوميت، أم أنه يُقدّر خططها في مجال الطاقة المتجددة حق قدرها؟

لمعرفة كيف تترجم فجوة السعر/المبيعات هذه مقارنة بالأقران والصناعة والنسبة العادلة إلى مخاطر التقييم العملية، انظر ماذا تقول الأرقام عن هذا السعر - اكتشف ذلك في تحليل التقييم الخاص بنا.

الخطوات التالية

مع وجود إشارات متضاربة بشأن التقييم والمخاطر والعوائد، قد ترغب في إلقاء نظرة على الصورة الكاملة بنفسك، والتصرف بينما لا تزال المشاعر حاضرة، وموازنة المكافأة الرئيسية وعلامتي التحذير المهمتين.

هل تبحث عن المزيد من أفكار الاستثمار؟

إذا ساهمت تجربة كالوميت في تحسين تركيزك، فلا تتوقف عند هذا الحد. وسّع قائمة مراقبتك بأفكار جديدة توازن بين الجودة والدخل والتحكم في المخاطر.

- اكتشف الصفقات المحتملة مبكراً من خلال فحص 53 سهماً عالي الجودة مقوم بأقل من قيمته الحقيقية، تتمتع بأساسيات قوية، والتي قد لا يدركها السوق بشكل كامل بعد.

- اضمن دخل محفظتك الاستثمارية من خلال مراجعة 10 صناديق استثمارية ذات عوائد مرتفعة تجمع بين العوائد المرتفعة والتركيز على المرونة.

- قلل المخاطر عن طريق التحقق من 66 سهماً مرناً ذات درجات مخاطر منخفضة والتي تحقق نتائج جيدة من حيث قوة الميزانية العمومية والتقلبات.

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.