Assessing China Yuchai International (NYSE:CYD) Valuation After New Minibus Launch And Intelligent Manufacturing Push

China Yuchai International Limited CYD | 0.00 |

China Yuchai International (CYD) has attracted fresh attention after unveiling commercial minibuses in Hong Kong using its YCY24-65kW Flywheel Range Extender System, alongside forming a new intelligent manufacturing subsidiary with an employee equity incentive plan.

The recent product launch and manufacturing reorganisation come against a backdrop of strong market momentum, with a 39.77% 1 month share price return and a very large 1 year total shareholder return, indicating that investors are reassessing both growth prospects and risk.

If you are looking beyond a single stock and want to see what else is benefiting from shifts in mobility and automation, take a look at 34 robotics and automation stocks

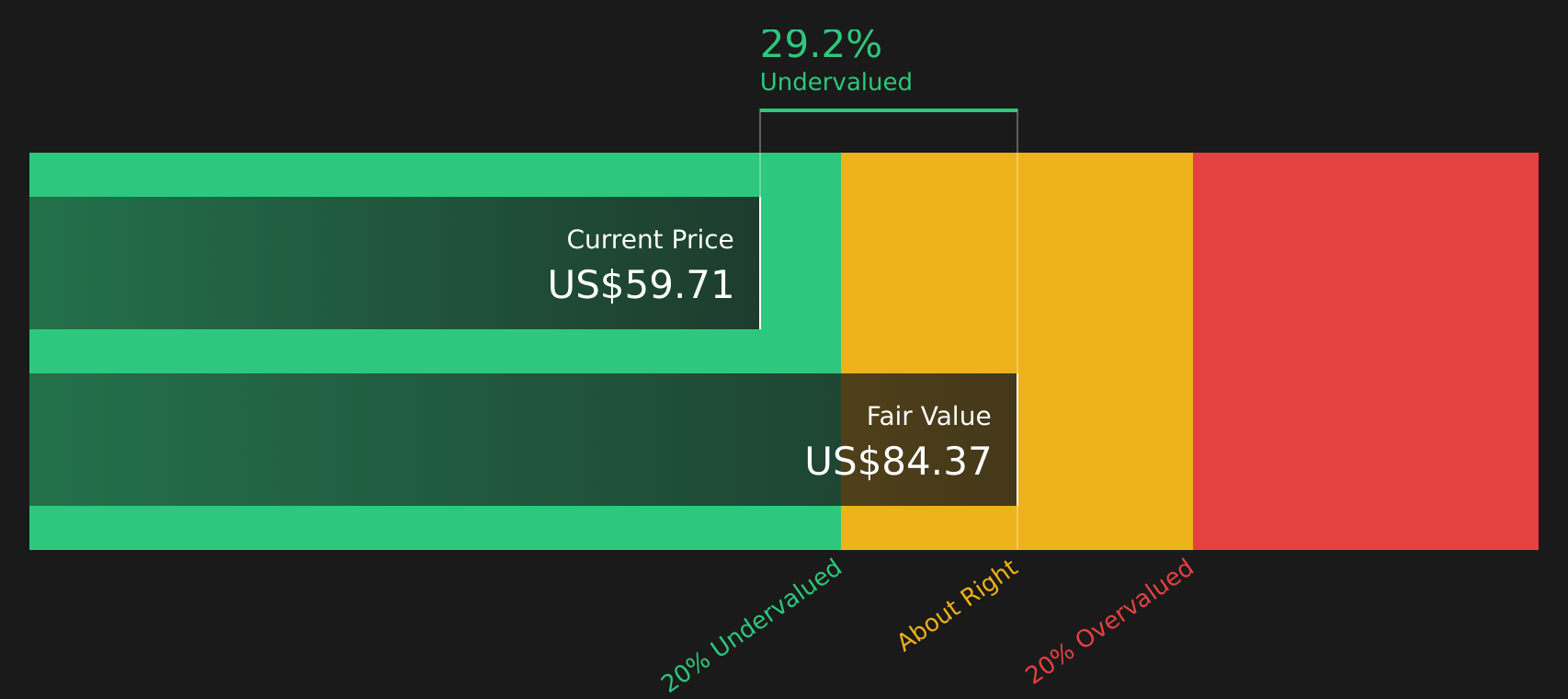

With China Yuchai delivering strong recent returns and trading at an estimated 30% discount to one intrinsic value measure, investors now face a key question: is there still mispricing here, or is the market already baking in future growth?

Most Popular Narrative: 15% Overvalued

China Yuchai International's most followed narrative pegs fair value at about $51.42, below the last close of $59.04. This frames the recent rally in a very specific way.

The current high valuation may reflect investor optimism about China Yuchai's ability to sustain extraordinary export growth and market share gains despite signs that replacement and expansion demand in trucks, buses, and construction vehicles may plateau as the effects of urbanization and infrastructure investment in China and ASEAN normalize. This could create downside risk to future revenue growth if end-market demand reverts to mean levels.

Curious what earnings path and margin profile sit behind that fair value gap, and why the projected future P/E steps down from today? The full narrative spells out the revenue glide path, the profit squeeze baked into the model, and the exact return hurdle used to bring those forecasts back to a single present day number.

Result: Fair Value of $51.42 (OVERVALUED)

However, there are still clear swing factors here, including whether high horsepower capacity expansion pays off and whether new energy exports scale enough to offset ICE headwinds.

Another View: Cash Flow Points to Undervaluation

While the most followed narrative sees China Yuchai as about 15% overvalued at $59.04 versus a $51.42 fair value, the SWS DCF model lands in a very different place. It suggests fair value of about $84.32, which is roughly a 30% gap in the other direction.

This split between an earnings based fair value and a cash flow based one leaves you with a practical question: do you lean more on current multiples and analyst assumptions, or on long run cash generation estimates?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out China Yuchai International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment split between earnings and cash flow views, it helps to move quickly and test the assumptions yourself using the 3 key rewards.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that may better match your goals, risk comfort, and timeline.

- Target long term compounding potential by running your filters through 46 high quality undervalued stocks which already combines quality metrics with pricing signals.

- Strengthen your income stream by scanning for resilient payers using the 10 dividend fortresses that focuses on higher yielding companies.

- Prioritise capital protection first with the 65 resilient stocks with low risk scores that highlights companies with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.