Assessing Copa Holdings (NYSE:CPA) Valuation After Strong Q1 Results And Ongoing Shareholder Payouts

Copa Holdings, S.A. Class A CPA | 0.00 |

Copa Holdings (NYSE:CPA) is back in focus after reporting Q1 revenue of US$1.05b and net income of US$212.47m, along with a 5.12% dividend yield and ongoing US$141m share buybacks.

The stock has climbed in recent months, with a 30 day share price return of 10.24% and an 11.11% year to date share price return. The 1 year total shareholder return of 32.55% points to stronger gains over a longer horizon.

If Copa Holdings has caught your attention, it can be helpful to compare it with other opportunities using a focused screener such as 20 top founder-led companies

With a recent share price of US$135.37, solid reported earnings and a 5.12% dividend yield supported by buybacks, the key question is whether Copa is still trading below its worth or if the market is already factoring in its future prospects.

Most Popular Narrative: 16.4% Undervalued

Analysts following Copa Holdings see a fair value of $161.93 per share, above the last close of $135.37. This frames the current valuation debate around future earnings power and capital allocation.

The company's disciplined cost management, ongoing seat densification, and delivery of more fuel-efficient Boeing 737 MAX aircraft enable Copa to maintain industry-leading net and operating margins, giving it resilience and earnings growth potential even in a competitive environment with downward pressure on yields.

Curious what underpins that margin story and fair value gap? The narrative focuses on steady revenue expansion, richer profitability, and a future earnings multiple that assumes investor confidence holds up.

Result: Fair Value of $161.93 (UNDERVALUED)

However, this depends on Copa maintaining its pricing power and avoiding major disruption at the Panama City hub, where any shock could quickly pressure revenue and margins.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

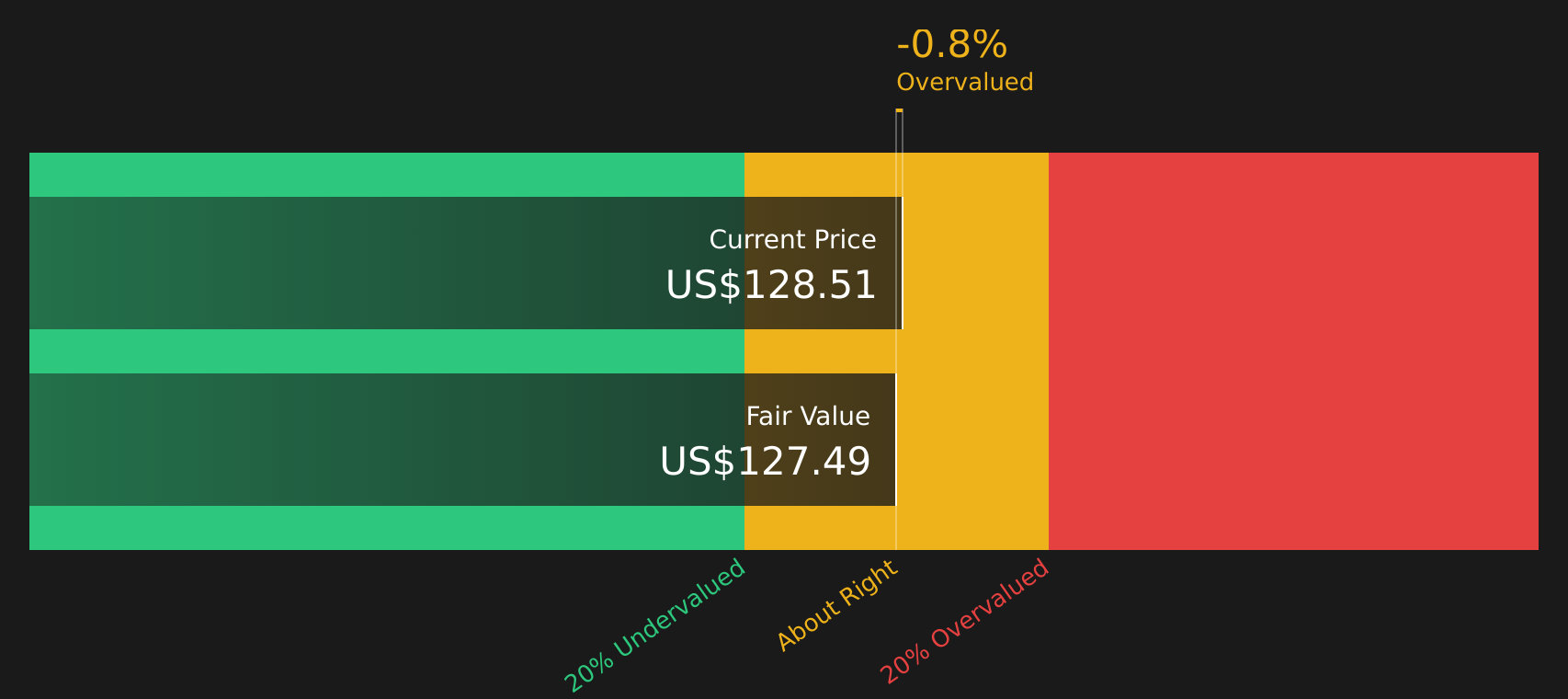

Another View: DCF Puts Copa Closer to Fairly Priced

Analysts see Copa trading 16.4% below their fair value of $161.93, yet Simply Wall St's own DCF model points to a value of about $126.94, below the current $135.37. That suggests less of a clear bargain. Which story do you think fits your expectations better?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Copa Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Positive or cautious after all this, the key is to move quickly, look through the data yourself, and weigh both the 5 key rewards and 1 important warning sign

Looking for more investment ideas?

If Copa has earned a spot on your watchlist, do not stop there. Widen your search now so you are not relying on a single story.

- Spot potential high return opportunities early by scanning 24 elite penny stocks with strong financials, which already show stronger financial footing than many expect from this corner of the market.

- Target quality at a reasonable price by using the 46 high quality undervalued stocks to focus on companies with solid fundamentals that may not be fully reflected in current valuations.

- Prioritise consistency and resilience with the 63 resilient stocks with low risk scores and concentrate on stocks that score better on financial strength and risk checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.