Assessing Copa Holdings (NYSE:CPA) Valuation After Strong Recent Share Price Momentum

Copa Holdings, S.A. Class A CPA | 114.59 | -2.82% |

Why Copa Holdings is on investors’ radar

Copa Holdings (NYSE:CPA) has drawn fresh attention after recent trading, with the stock closing at US$154.09. That price sits against annual revenue of US$3,533.554m and net income of US$664.795m.

The recent jump to a 1-month share price return of 20.93%, alongside a 1-year total shareholder return of 78.06%, suggests momentum has been building rather than cooling off for Copa Holdings.

If this strength in the airline space has caught your attention, it could be a good moment to widen your watchlist with 22 top founder-led companies as another set of companies to review.

With the shares up strongly over 1 month and 1 year, and trading only slightly below the US$158.40 analyst price target, the key question is whether Copa still offers a mispricing opportunity or if the market is already factoring in future growth.

Most Popular Narrative: 2% Undervalued

At $154.09, Copa Holdings sits slightly below the most followed fair value estimate of about $156.87, which is built on detailed traffic, margin and growth assumptions.

The company's disciplined cost management, ongoing seat densification, and delivery of more fuel-efficient Boeing 737 MAX aircraft enable Copa to maintain industry-leading net and operating margins, giving it resilience and earnings growth potential even in a competitive environment with downward pressure on yields.

Curious what earnings power and revenue runway need to line up for that fair value to hold? The narrative leans heavily on sustained margin strength and a richer profit multiple. Want to see exactly how that combination supports a price tag above today’s level?

Result: Fair Value of $156.87 (UNDERVALUED)

However, this hinges on Copa holding its margins and traffic, with fuel price swings and competition in key Latin American routes acting as potential spoilers for the story.

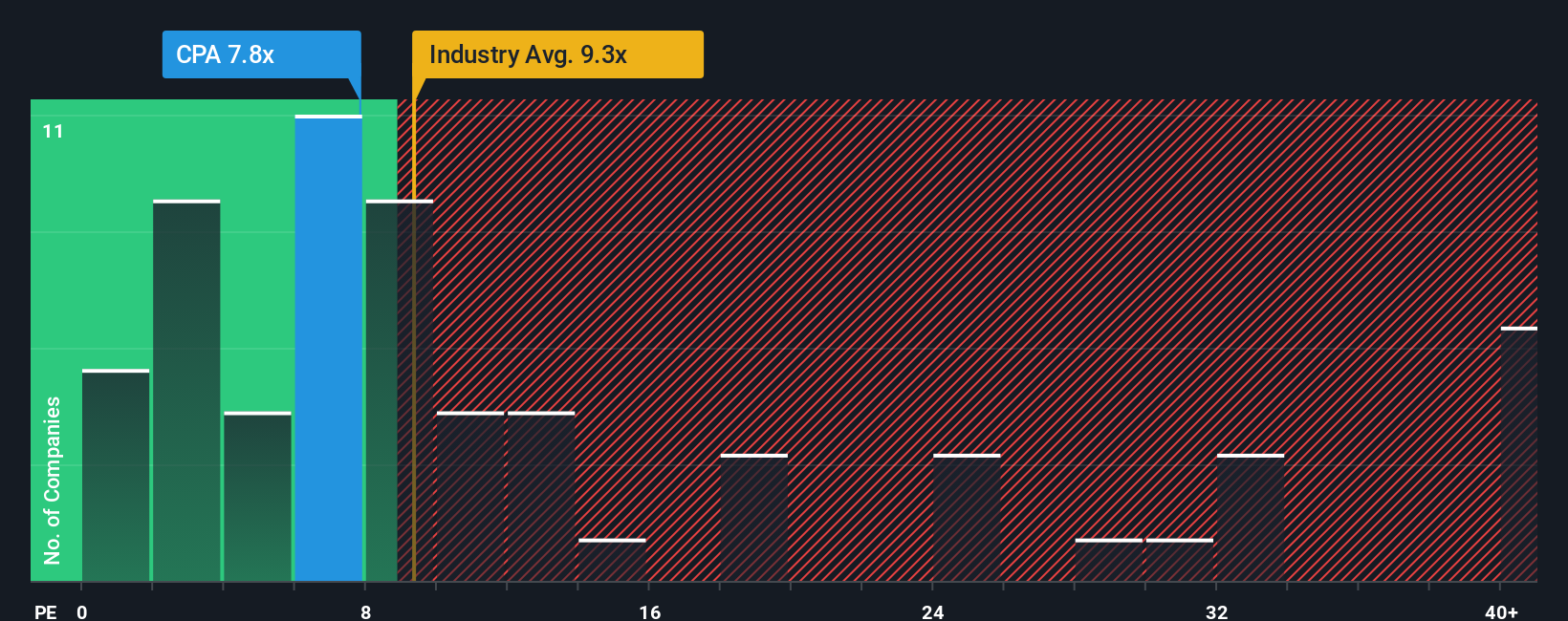

Another View: What the P/E Ratio Signals

Our fair value narrative paints Copa as about 2% undervalued, yet the current P/E of 9.6x complicates that picture. It sits slightly above the global airlines average of 9.5x, well below the US market at 19.3x, and below a fair ratio of 15.2x. Is the market underestimating Copa or already pricing in the good news?

Build Your Own Copa Holdings Narrative

If you see the numbers differently or like to test assumptions yourself, you can build a fresh thesis in just a few minutes: Do it your way

A great starting point for your Copa Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Copa has sharpened your focus, do not stop here, the same tools can help you spot other opportunities that fit your style and risk comfort.

- Target value first and see which companies stand out in our 53 high quality undervalued stocks based on strong fundamentals and attractive pricing signals.

- Prioritize resilience by scanning our 86 resilient stocks with low risk scores for companies that score well on stability and business quality.

- Hunt for tomorrow's standouts with our screener containing 25 high quality undiscovered gems that highlight quality companies flying under most investors' radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.