Assessing CorVel (CRVL) Valuation As Recent Share Price Momentum Contrasts With Longer Term Weakness

CorVel Corporation CRVL | 0.00 |

Why CorVel Stock Is Drawing Attention Now

Without a specific news catalyst in play, CorVel (CRVL) is attracting interest mainly because of its current valuation metrics, recent return pattern, and the scale of its workers’ compensation and claims management business.

Recent trading illustrates that CorVel’s 30 day share price return of 7.34% and 90 day share price return of 17.80% sit against a year to date share price decline of 6.07% and a 1 year total shareholder return decline of 44.50%. This suggests momentum has picked up in the short term while longer term holders are still under pressure.

If you are weighing CorVel against other potential ideas, this is a good moment to broaden your watchlist with a curated set of 40 healthcare AI stocks

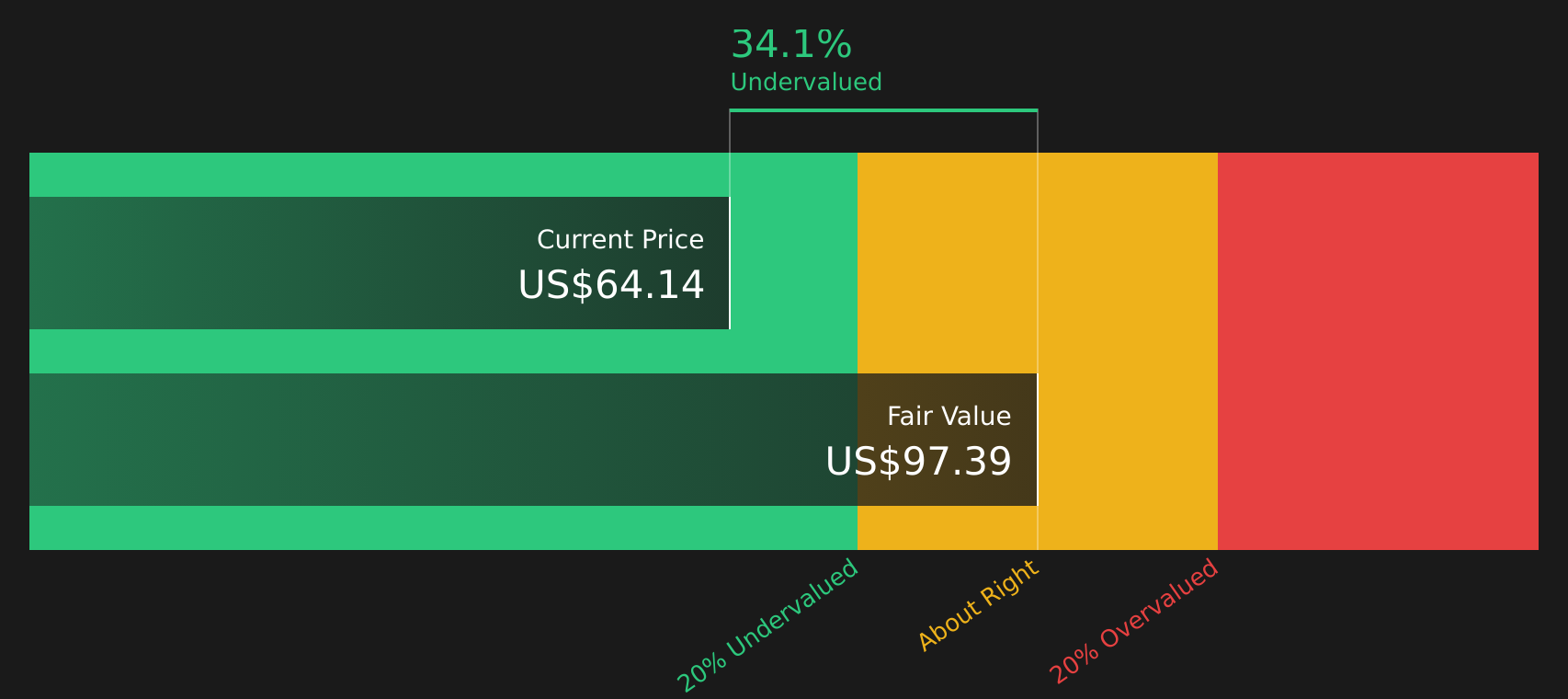

With CorVel trading at an estimated 36.60% discount to its assessed intrinsic value yet carrying a mixed return record, you have to ask: is this a genuine opening, or is the market already baking in future growth?

Price to Earnings of 28.4x: Is It Justified?

On one hand, CorVel screens as good value against its estimated future cash flows, with the SWS DCF model indicating a fair value of $97.39 versus a last close of $61.75. On the other hand, the stock trades on a P/E of 28.4x, which is lower than a peer average of 86.8x but higher than the broader US Healthcare industry average of 23.2x.

The P/E multiple compares CorVel’s current share price to its earnings per share and is a quick way of seeing how much investors are paying for each dollar of profit. For a business generating $958.5m of revenue and $110.3m of net income, with earnings growing 14.5% per year over the past 5 years and return on equity of 28%, a higher than industry P/E suggests investors are paying a premium for its earnings profile.

Against peers, CorVel’s 28.4x P/E looks restrained, especially given that some similar companies trade on much richer multiples that lift the peer average to 86.8x. Yet compared with the wider Healthcare industry at 23.2x, CorVel does not come across as cheap. This indicates the market is assigning it a higher price for each dollar of earnings than many industry peers while still far from the loftiest valuations in its space.

Result: Price to earnings of 28.4x (ABOUT RIGHT)

However, this setup could easily be knocked off course if the 1 year shareholder return slide continues or if regulatory shifts pressure workers’ compensation margins.

Another Angle On CorVel’s Valuation

Even though the SWS DCF model suggests CorVel is trading at a 36.6% discount to its estimated future cash flow value of $97.39 per share, that is only one lens. DCFs rely heavily on long term assumptions. What if the future unfolds differently to those inputs?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CorVel for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on returns and valuation, how does CorVel really stack up for you right now? Take a moment to review the figures yourself, weigh the trade off between its risks and potential rewards, and then tap into the 2 key rewards and 1 important warning sign

Looking For More Investment Ideas?

If CorVel has you thinking harder about where to put fresh capital, do not stop here; widen the lens and let data rich screeners surface new angles.

- Target potential mispriced opportunities by scanning 46 high quality undervalued stocks that combine attractive valuations with solid business profiles.

- Prioritise resilience first and filter for companies in the 64 resilient stocks with low risk scores that score well on risk and financial quality checks.

- Hunt for less crowded opportunities by reviewing the screener containing 22 high quality undiscovered gems, where strong fundamentals have not yet drawn broad attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.