Assessing CRH (NYSE:CRH) Valuation After Q1 Growth, Impairment-Driven Loss And Reaffirmed Outlook

CRH public limited company CRH | 0.00 |

Q1 results and guidance reaffirmation set the tone for CRH (NYSE:CRH)

CRH (NYSE:CRH) stock reacted to first quarter 2026 results that paired higher revenue and adjusted EBITDA with a wider net loss, as the company reaffirmed rather than raised its full year earnings guidance.

CRH’s share price is US$112.63 after a 1 day share price return of a 2% decline and a 7 day share price return of a 4.9% decline. Its 1 year total shareholder return of 21.2% and 3 year total shareholder return of around 14x suggest momentum has built over a longer horizon, even as investors reassess near term risks around the reaffirmed outlook and recent impairments.

If this kind of infrastructure exposure interests you, it can be useful to compare CRH with other companies tied to long lived assets by checking out 36 power grid technology and infrastructure stocks

After a double digit 1 year return and a share price that sits well below the average analyst target, along with ongoing buybacks, investors may question whether CRH is undervalued or whether the market already reflects expectations for future growth.

Most Popular Narrative: 21.2% Undervalued

CRH’s most followed valuation narrative pegs fair value at about $142.95, comfortably above the last close at $112.63, and frames the gap through measured growth and margin assumptions rather than aggressive bets.

The ongoing rollout of U.S. federal infrastructure funding (less than 40% of the IIJA highway funds have been spent) and an encouraging outlook for the next highway bill create a substantial, multi-year runway for demand in CRH's core public infrastructure segments, offering the prospect for sustained revenue growth and backlog visibility.

Analysts are not banking on hyper growth here. They lean on steady revenue expansion, firmer margins, and a richer future earnings multiple to justify that higher fair value. Want to see which of those inputs carries the most weight in pushing value toward $140 plus, and how share count changes factor into the story?

Result: Fair Value of $142.95 (UNDERVALUED)

However, you also need to weigh political risk around U.S. infrastructure funding and execution risk from large acquisitions like Eco Material, as either could pressure margins.

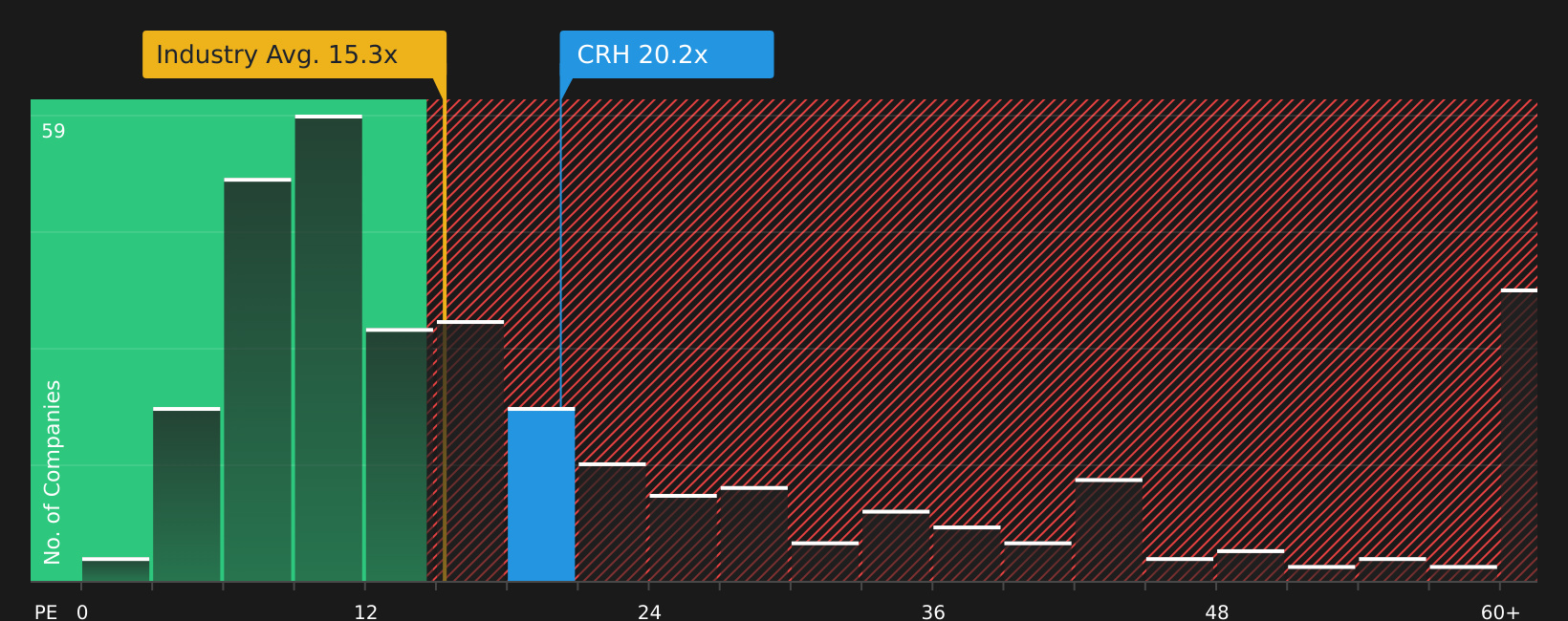

Another Take: What The P/E Ratio Is Saying

That 21.2% undervalued narrative leans on analyst forecasts and a fair value of about $142.95. The market, though, is currently pricing CRH at a P/E of 20.6x, below its fair ratio of 25.7x and peer average of 30.2x, yet above the Global Basic Materials industry at 15.9x.

In simple terms, you are paying a premium to the wider industry but a discount to closer peers and the fair ratio. This leaves an open question: is the current price reflecting an opportunity, or a margin of safety that could disappear if sentiment shifts?

Next Steps

If this mix of optimism and caution feels familiar, it may be a good time to review the numbers yourself, decide what matters most to you, and then weigh both sides with the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

Once you have formed a view on CRH, do not stop there; the next smart move is to broaden your watchlist with other clear, data driven opportunities.

- Target potential mispricing by scanning a focused list of companies that appear cheap relative to their quality using the 51 high quality undervalued stocks.

- Prioritise resilience by checking companies that pair cleaner balance sheets with solid fundamentals through the solid balance sheet and fundamentals stocks screener (44 results).

- Spot lesser known opportunities before the crowd by reviewing the screener containing 23 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.