Assessing Cummins (CMI) Valuation After Record Distribution Revenue And New Hybrid Mining Truck Grant

Cummins Inc. CMI | 0.00 |

Cummins (CMI) is back in focus after reporting record revenue in its distribution segment and attracting strong institutional interest, while also securing a US$2.1 million grant to advance hybrid mining truck systems.

That backdrop of record distribution revenue, strong institutional buying and fresh funding for low emission mining trucks has come alongside strong momentum, with a 39.33% 3 month share price return and a very large 5 year total shareholder return of 174.86%.

If Cummins' recent strength has you looking more broadly at industrial and manufacturing trends, it could be worth checking out other auto manufacturers that are catching investor attention right now.

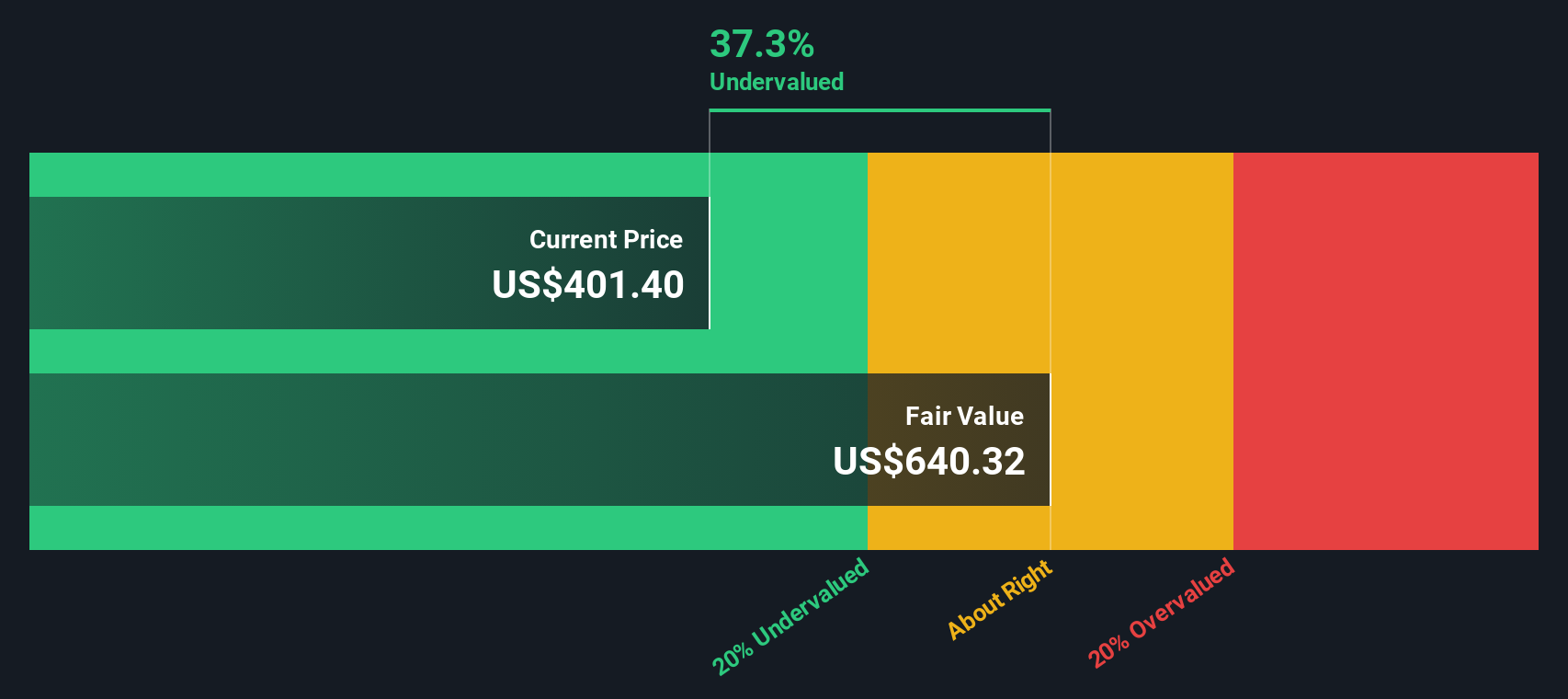

With Cummins trading around US$582 and only a small intrinsic discount indicated by recent estimates, the real question is whether today’s price reflects all that progress or if the market is still underestimating future growth.

Price-to-Earnings of 30.1x: Is it justified?

Cummins is trading on a P/E of 30.1x, which sits above both its Machinery industry average and its closest peer group, even with the recent share price strength.

The P/E ratio compares the current share price to earnings per share, so a higher figure usually means investors are willing to pay more for each dollar of earnings. For a diversified industrial group like Cummins, that can point to expectations for sustained profitability, solid returns on equity and continued earnings growth.

Here, Cummins' 30.1x P/E is described as expensive relative to both the US Machinery industry at 27.2x and a peer average of 26.3x, so the market is clearly assigning a premium. At the same time, that multiple sits below an estimated fair P/E of 35.5x, which suggests there is still headroom if earnings and returns track what this fair ratio implies the market could move toward.

Result: Price-to-Earnings of 30.1x (ABOUT RIGHT)

However, that premium story can quickly wobble if industrial demand softens or if Cummins' investments in electrified and low emission systems take longer than expected to translate into earnings.

Another angle from the SWS DCF model

While the 30.1x P/E looks full compared to the Machinery industry and peers, our DCF model presents a slightly different picture, with Cummins trading at about US$582 versus an estimated future cash flow value of US$599.3, roughly a 2.9% discount.

That is not a huge gap. However, it suggests the price is closer to fair than frothy, at least on cash flow assumptions. The tension for you is whether to trust earnings-based signals that flag a premium or a cash flow view that points to a small discount.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Cummins for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 881 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Cummins Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can build a custom view in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Cummins.

Looking for more investment ideas?

If Cummins is on your radar, do not stop there. Widening your watchlist with fresh ideas can help you spot opportunities others might skip.

- Scan for potential mispricings by reviewing these 881 undervalued stocks based on cash flows that might not yet be fully appreciated by the wider market.

- Tap into fast moving themes by checking out these 23 AI penny stocks riding advances in automation, data processing and machine learning applications.

- Add income angles to your watchlist through these 13 dividend stocks with yields > 3% that offer yields above 3% alongside stock market exposure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.