Assessing Datadog (DDOG) Valuation After Storage Management Launch and Upbeat Growth Guidance

Datadog DDOG | 118.67 | +0.53% |

Datadog (DDOG) just rolled out its new Storage Management solution, targeting cloud object storage costs for organizations dealing with data and AI heavy workloads. The announcement arrives alongside impressive year-over-year revenue growth and an uptick in full-year guidance.

Datadog’s momentum is showing no signs of fading, with a 15.6% gain in the last month and an impressive 41.5% total shareholder return over the past year. While the share price cooled slightly this week, recent product rollouts and upbeat guidance continue to feed long-term optimism.

If you’re curious which other tech innovators are riding strong trends, explore See the full list for free. for more discovery opportunities.

With Datadog’s robust growth and fresh guidance lifting expectations, investors must now weigh whether the recent rally leaves room for further gains or if the stock’s current price already captures much of its future potential.

Most Popular Narrative: 10.1% Overvalued

With Datadog’s widely followed fair value estimate at $168.91, the last close price of $185.97 pushes the stock into premium territory. This sets the stage for a valuation built around aggressive growth expectations and ongoing platform dominance.

Ongoing product innovation, such as autonomous AI agents, enhanced security modules, and expanded log and data observability, is increasing platform breadth and relevance. This provides cross-selling opportunities and drives higher average revenue per user and net retention rate, which in turn improves recurring revenue predictability and gross margins.

Want to know what powers Datadog’s hefty price tag? The growth forecasts, built on platform expansion and a jump in profitability, might surprise you. Can the business truly deliver the scale and margin leap that the narrative demands? Unpack the make-or-break projections fueling this forward-looking value call.

Result: Fair Value of $168.91 (OVERVALUE D)

However, persistent heavy R&D investment and mounting competition from cloud hyperscalers could put pressure on Datadog’s margins and future growth outlook.

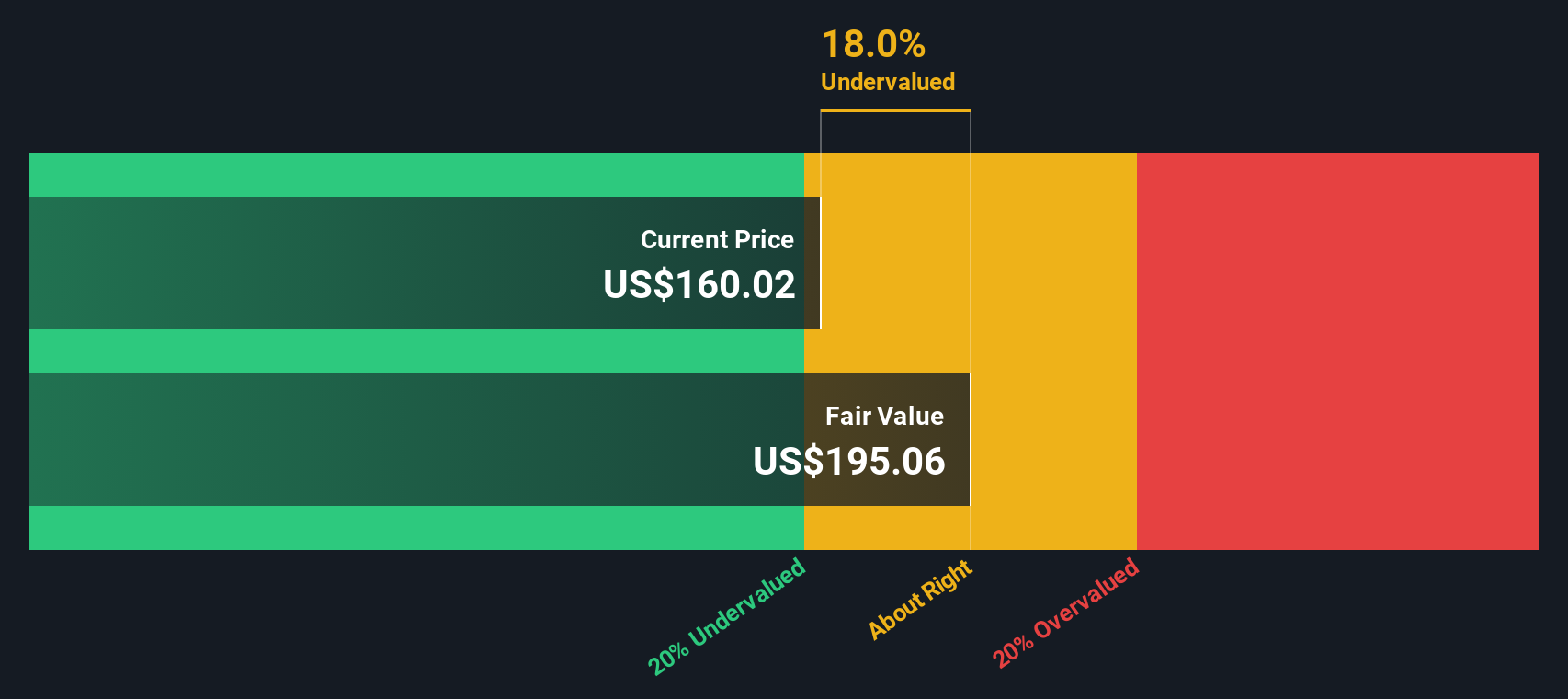

Another View: DCF Model Offers a Different Signal

Looking at our SWS DCF model, a different story emerges. Datadog's current share price is about 11.7% below its estimated fair value of $210.50. This suggests that, despite premium outlooks from multiples, there may be more upside left than the overvalued narrative implies. Could this signal justify further optimism, or does it flag hidden risks beneath the surface?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Datadog for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 885 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Datadog Narrative

If you have a different take on Datadog’s outlook or want to dig into the data yourself, you can craft your own story in just minutes. Do it your way

A great starting point for your Datadog research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Seize the chance to uncover tomorrow’s standout stocks with unique angles and growth potential. Don’t let the next opportunity pass you by.

- Tap into future healthcare breakthroughs by checking out these 31 healthcare AI stocks and see which companies are advancing AI-driven patient solutions.

- Spot value before the crowd by reviewing these 885 undervalued stocks based on cash flows, where cash flow fundamentals highlight companies trading below their intrinsic worth.

- Boost passive income potential by considering these 15 dividend stocks with yields > 3% featuring businesses offering reliable yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.