Assessing Delek Logistics Partners (DKL) Valuation As Mixed Signals Emerge On Growth And Cash Flow Potential

Delek Logistics Partners LP DKL | 0.00 |

Why Delek Logistics Partners Stock Is On Investor Radar

Delek Logistics Partners (DKL) has caught investor attention after recent trading left the units at US$49.58, with the partnership showing a market value of about US$2.7b and a multi segment midstream footprint.

Recent trading shows mixed momentum, with a 1 day share price return of 1.62% but a 30 day share price return decline of 6.03%, while the 1 year total shareholder return of 47.44% points to much stronger longer term results.

If Delek Logistics Partners has your attention, now can be a good time to widen your lens and check out 31 power grid technology and infrastructure stocks

With units trading around US$49.58, only a small discount to the US$49.00 analyst price target but a much larger implied intrinsic discount, the key question is whether DKL is undervalued or if the market already prices in future growth.

Most Popular Narrative: 1% Overvalued

With Delek Logistics Partners closing at $49.58 against a narrative fair value of $49, the current price sits slightly above that central estimate while still reflecting a tight gap between market view and modeled outcome.

The full commissioning and expected ramp to capacity of the new Libby 2 gas plant in the Delaware Basin, along with associated investments (amine unit and AGI wells), positions Delek Logistics to capitalize on rising energy demand and stable domestic energy infrastructure needs, likely boosting gathering and processing volumes, EBITDA, and revenue growth.

Curious what kind of revenue mix, margin path, and profit multiple are baked into that fair value, and how much weight sits on the Libby 2 timeline.

Result: Fair Value of $49 (OVERVALUED)

However, you still need to weigh risks around Delek Logistics Partners' higher leverage, its heavy dependence on fossil fuel demand, and its reliance on Permian focused customers.

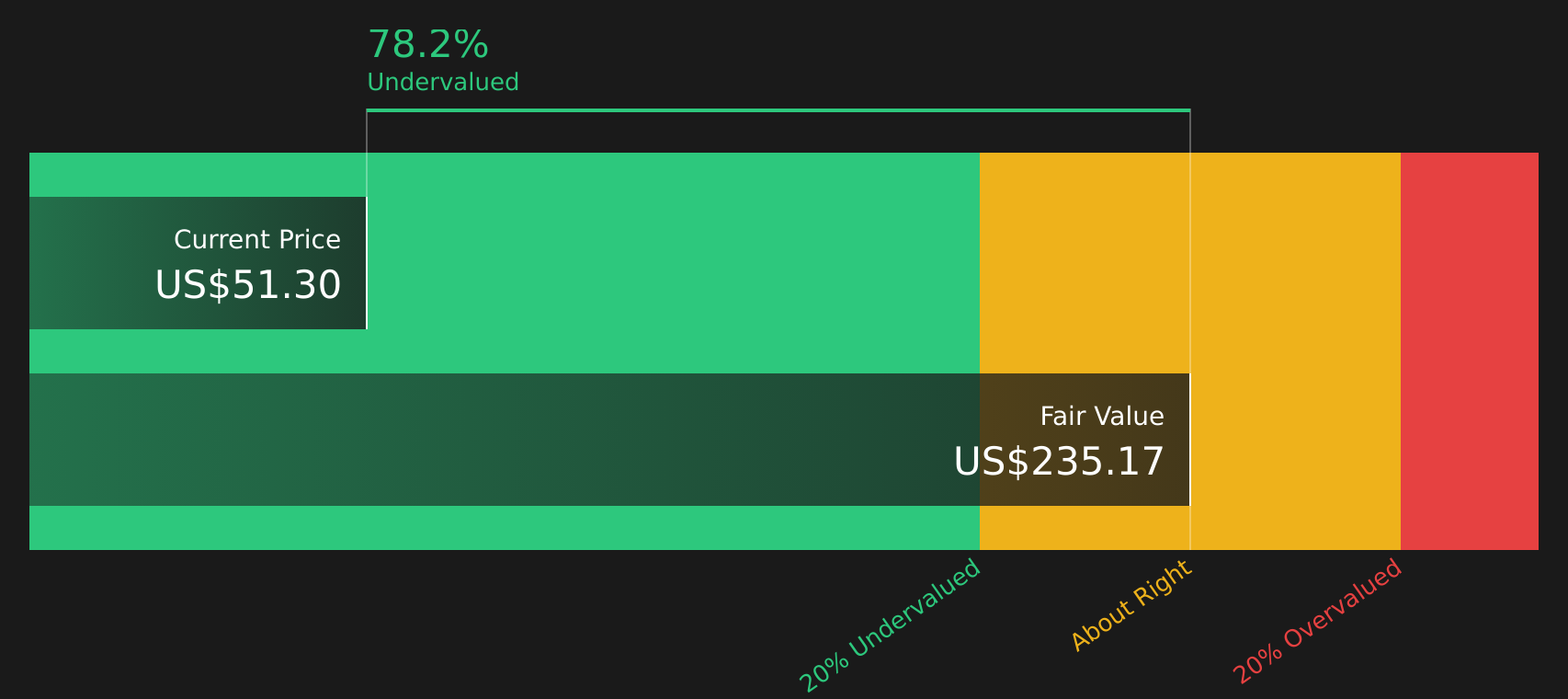

Another View: Cash Flows Point to a Very Different Story

While the analyst narrative pegs Delek Logistics Partners at a fair value of $49 and labels the units as slightly overvalued, the SWS DCF model tells almost the opposite story, with an estimate of future cash flow value of $379.35, suggesting a very wide valuation gap.

That kind of spread between a cash flow model and an earnings based target raises a practical question for you: which set of assumptions feels closer to how Delek Logistics Partners will actually generate and retain cash over time?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Delek Logistics Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 60 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The split views and wide valuation gap make this a good moment to check the numbers yourself and move quickly while sentiment is still forming, starting with 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you could miss out on other opportunities that fit your goals, risk comfort, and income needs across the market.

- Target potential value plays that combine quality with pricing power by checking out the 60 high quality undervalued stocks.

- Strengthen the defensive side of your portfolio by focusing on companies with strong finances using the solid balance sheet and fundamentals stocks screener (42 results).

- Build a stream of potential income ideas by scanning companies with higher yields through the 12 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.