Assessing D.R. Horton (DHI) Valuation After Renewed Investor Interest

D.R. Horton, Inc. DHI | 145.25 | +0.64% |

Why D.R. Horton (DHI) is back on investors’ radar

D.R. Horton (DHI) has attracted renewed attention after recent share price moves, with the stock showing mixed short term performance but double digit total returns over the past year and multi year periods.

For investors watching the homebuilding space, D.R. Horton’s current share price around $158.13, its recent value score of 1, and its recorded revenue and net income figures are providing fresh context for reassessing the stock.

Recent trading has been firm, with a 7 day share price return of 5.13% and a 30 day share price return of 9.43%. The 1 year total shareholder return of 17.84% and 5 year total shareholder return of 99.72% point to momentum that has been sustained over several years rather than just a short term rebound.

If this has you thinking about where else capital could work hard in housing related themes, it might be worth scanning 22 power grid technology and infrastructure stocks as a way to spot other infrastructure linked opportunities.

With D.R. Horton earning a value score of 1, trading near $158.13, and sitting only about 1.5% below one analyst price target of $160.50, you have to ask: is this an undervalued homebuilder, or is the market already pricing in future growth?

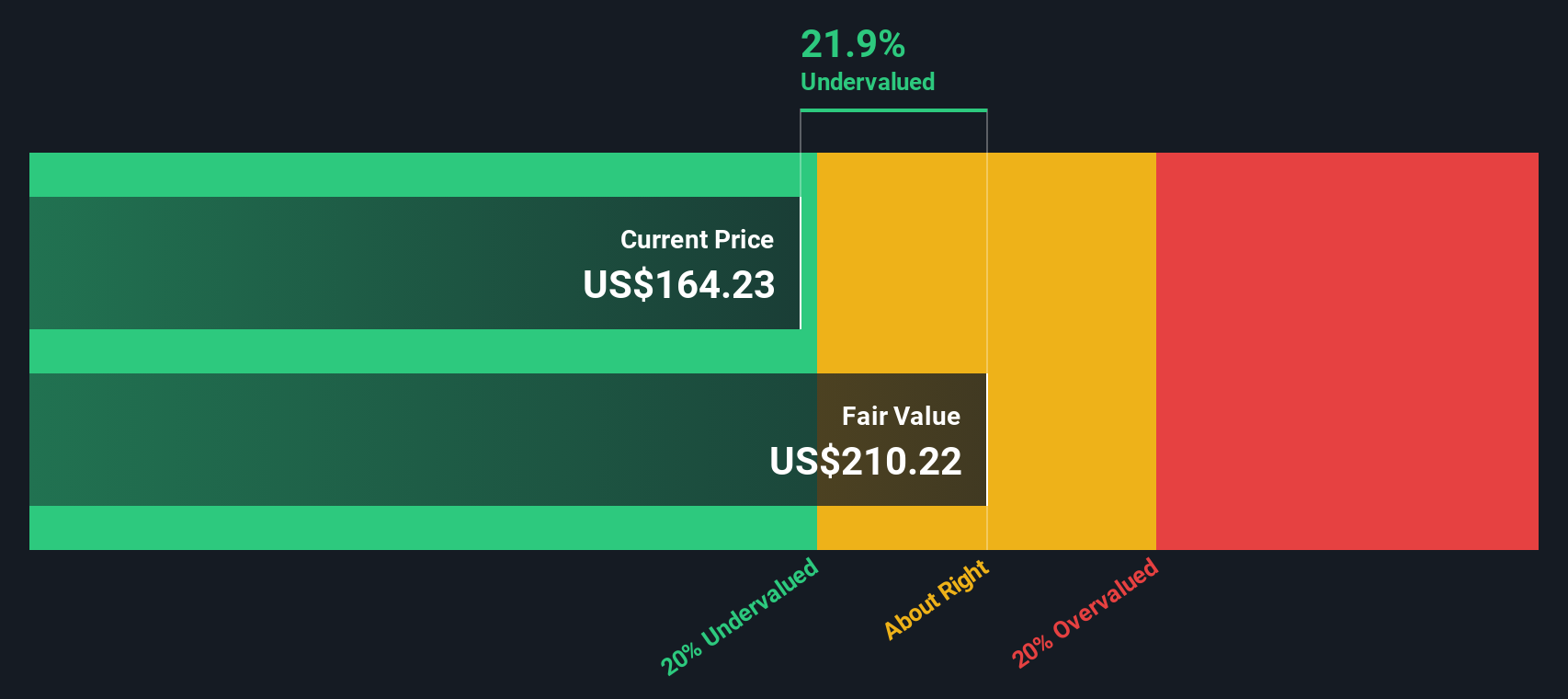

Most Popular Narrative: 4.5% Undervalued

At a last close of $158.13 against a most followed fair value estimate of about $165.67, D.R. Horton is framed as modestly undervalued. That gap rests on a detailed long term housing story rather than just recent price moves.

The company's continued strategic expansion of entry-level and affordable home offerings enables it to address affordability concerns, tap into a wider buyer pool, and maintain high absorption rates, mitigating cyclical margin compression and sustaining revenue even in softer market conditions.

Curious how this focus on affordability links to that fair value gap? The narrative connects steady revenue growth, margins that hold their ground, and a future earnings multiple that has to compress to make the numbers work. If you want to see exactly which assumptions carry the most weight, the full story lays them out line by line.

Result: Fair Value of $165.67 (UNDERVALUED)

However, rising incentives and higher land costs could pressure margins, while heavy exposure to entry level buyers leaves earnings sensitive to weaker credit or employment conditions.

Another Way to Look at Value

Our SWS DCF model offers a different perspective from the 4.5% undervalued fair value narrative. On this view, D.R. Horton at $158.13 sits above an estimated future cash flow value of $127.25, which indicates the shares are overvalued rather than modestly cheap. Which interpretation seems more convincing to you?

Build Your Own D.R. Horton Narrative

If parts of this story do not quite fit your view, or you prefer to test every input yourself, you can build a custom D.R. Horton thesis using our tools in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding D.R. Horton.

Looking for more investment ideas?

If you are serious about putting your capital to work, do not stop at one company. The right mix of opportunities can make a real difference.

- Spot potential value plays early by scanning 55 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect their underlying strength.

- Prioritise resilience by reviewing solid balance sheet and fundamentals stocks screener (46 results) so you are focusing on companies with sturdier finances when conditions get tougher.

- Hunt for fresh ideas beyond the usual tickers through our screener containing 25 high quality undiscovered gems, so you are not missing companies that are still off most investors’ radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.