Assessing DuPont de Nemours (DD) Valuation After Recent Share Price Pullback

E. I. du Pont de Nemours and Company DD | 0.00 |

Short term performance check

DuPont de Nemours (DD) has seen the stock fall 4.2% over the past day and 6.1% over the past week, extending a decline of about 10.9% over the past month.

Looking beyond the recent pullback, DuPont de Nemours has a 10.25% year to date share price return and a 58.11% 1 year total shareholder return, which suggests recent momentum has cooled after a stronger run for patient holders.

If the recent volatility has you comparing alternatives in materials and industrials, it could be a good time to scan 19 top founder-led companies

With DuPont de Nemours trading at $45.06 and sitting about 27% below the average analyst price target and roughly 34% below an indicated intrinsic value, it raises a key question for you: is this genuine mispricing, or has the market already factored in the company’s growth prospects?

Most Popular Narrative: 20% Undervalued

On the most widely followed narrative, DuPont de Nemours screens as undervalued, with a fair value of $56.13 against the latest close at $45.06, which puts the current discount in sharp focus.

Persistent strength and investment in Healthcare and Water tap into growing global demand for clean water and healthcare solutions, supporting more resilient revenue and margin profiles over time. Combined with a sharpened portfolio focus after recent separations and divestitures, this positions DuPont to prioritize higher quality specialty businesses and a more stable earnings base that underpins its long term valuation case.

Curious what sits behind that long term valuation case, and how analysts connect revenue, margins, and profit multiples to reach that fair value and upside gap.

Result: Fair Value of $56.13 (UNDERVALUED)

However, that upside story can be knocked off course if PFAS legal risks escalate or if portfolio moves like the Qnity separation leave earnings more volatile.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View on DuPont de Nemours' Valuation

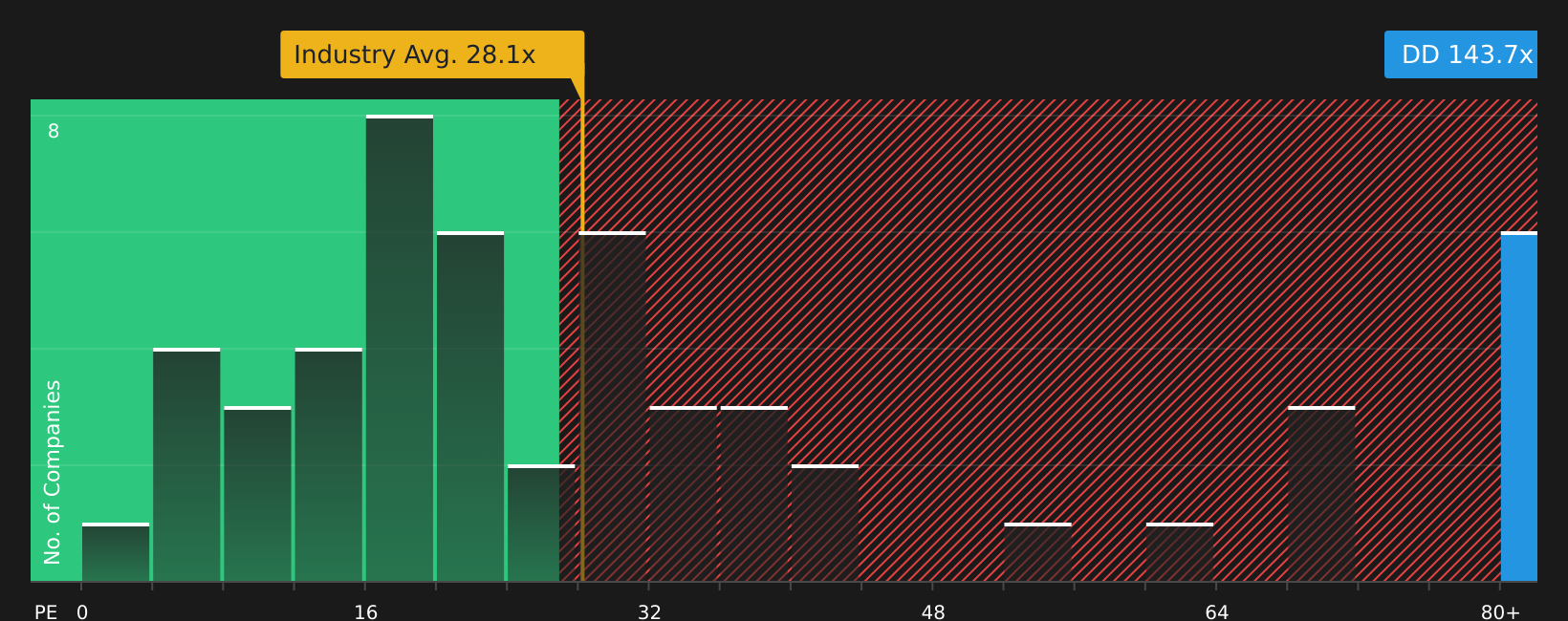

The earlier fair value story leaned on future cash flows and growth assumptions, but the current P/E of 138.3x paints a very different picture. It sits well above the Chemicals industry at 27.1x, the peer average at 21.2x, and a fair ratio of 31.1x. This points to valuation risk if sentiment cools or earnings stumble.

If you prefer to keep things grounded in current earnings and market comparables, this wide P/E gap is a useful cross check on the cash flow based upside story. It is also a prompt to ask which yardstick you trust more for DuPont de Nemours right now.

Next Steps

Given the mix of optimism about upside and concern about risks in this story, it makes sense to review the details for yourself and act while the market is still weighing both sides through 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If this valuation story has you thinking bigger, now is the moment to branch out and line up your next set of potential opportunities before others move first.

- Spot potential outliers early by scanning 25 elite penny stocks with strong financials that already show stronger financial foundations than many expect from this corner of the market.

- Focus on quality at a sensible price by reviewing 47 high quality undervalued stocks that combine supportive cash flows with balance sheets that can handle tougher conditions.

- Prioritize resilience by checking 63 resilient stocks with low risk scores that score well on stability so your portfolio is not leaning only on higher volatility holdings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.