Assessing Emerson Electric (EMR) Valuation After New AI And Corrosion Management Partnerships

Emerson Electric Co. EMR | 0.00 |

Why Emerson Electric (EMR) is back on investors’ radar

Emerson Electric (EMR) has moved closer to the center of industrial digital transformation after pairing its rugged industrial PCs with SiMa.ai’s AI chip platform and teaming up with Aramco on advanced corrosion management solutions.

The stock is trading at US$141.65, with the share price up 4.29% year to date and recent 7 day and 30 day share price returns of 3.83% and 3.06%, while the 1 year and 3 year total shareholder returns of 21.11% and 82.06% suggest momentum has been strong over both shorter and longer horizons.

If Emerson’s push into industrial AI has your attention, this can be a good moment to look beyond a single stock and scan 47 AI infrastructure stocks.

With Emerson trading at US$141.65, solid recent returns, and a price that sits below the average analyst target, the key question is whether the current valuation still leaves room for upside or if the market already prices in future growth.

Most Popular Narrative: 13.5% Undervalued

At $141.65, the most followed narrative pegs Emerson Electric’s fair value at $163.72, which frames current pricing against a higher long term earnings path.

The accelerating adoption of digital automation and artificial intelligence solutions in global industrial markets is fueling demand for Emerson's advanced software platforms and AI-enabled products, such as Ovation 4.0 and Nigel AI adviser. This is resulting in order growth and positions the company for revenue expansion. Large-scale investments in power generation, LNG, and life sciences, driven by rising energy security concerns, electrification, and sustainability initiatives, are driving greenfield and modernization projects, particularly in regions like North America, Asia, and the Middle East. This is visible in higher orders and is expected to continue supporting revenue and earnings growth over the coming years.

Want to see what is backing that higher fair value? The narrative leans on steady revenue gains, firmer margins, and a future earnings multiple that mirrors specialist automation leaders.

Result: Fair Value of $163.72 (UNDERVALUED)

However, investors still need to weigh risks around tariffs and currency swings that could pressure margins, as well as potential disruption from new AI driven automation rivals.

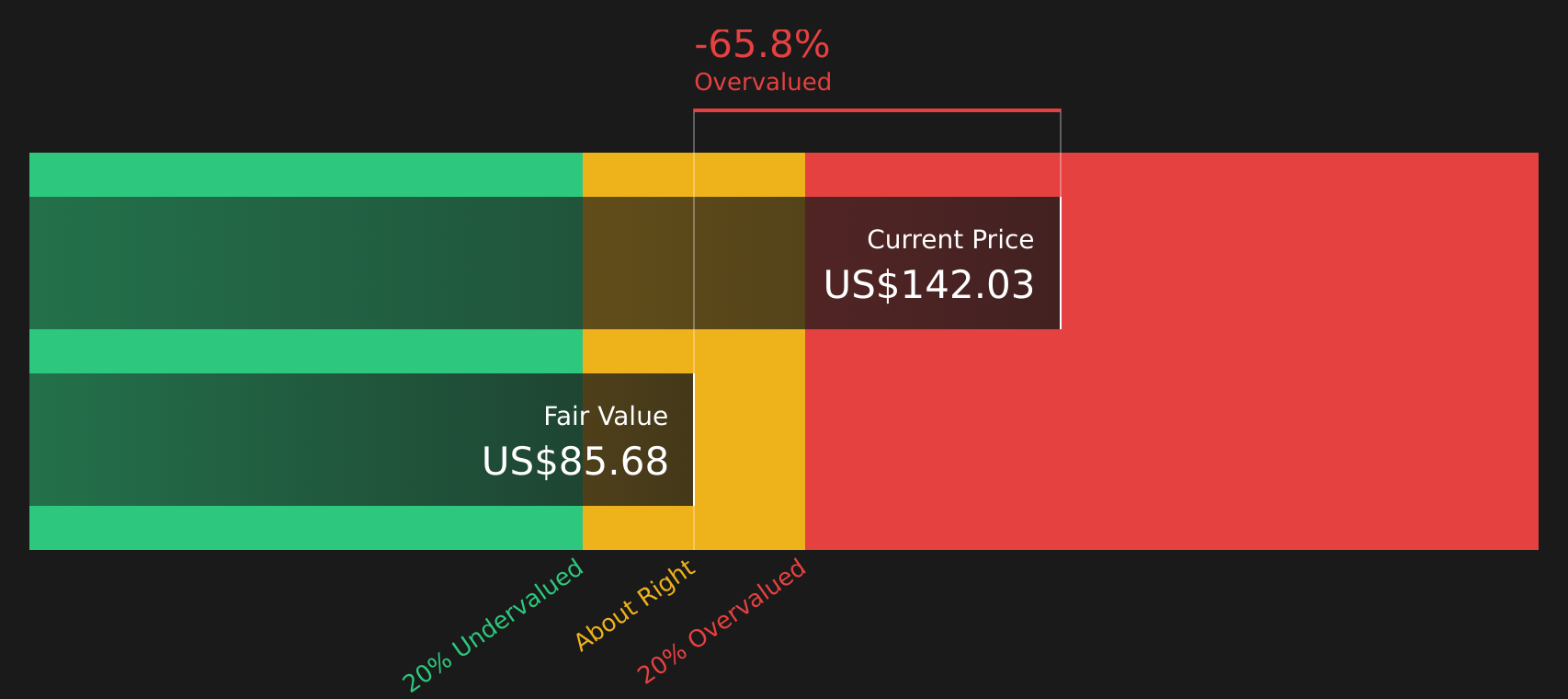

Another Way to Look at Value

While analysts see Emerson Electric as 13.5% undervalued with a fair value of $163.72, the SWS DCF model points in the opposite direction, with a future cash flow value of $85.76, well below the current $141.65 share price. That gap raises a simple question: which story do you trust more, earnings multiples or cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Emerson Electric for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals on value, it makes sense to check the numbers yourself and decide how compelling the story really is right now. To see both sides of the argument in one place, review the 5 key rewards and 1 important warning sign

Looking for more investment ideas?

Do not stop with a single stock when you can quickly scan a wider field of opportunities built from clear data, fundamentals, and risk checks.

- Target long term compounding by checking out 47 high quality undervalued stocks, where quality companies trade at prices that may not fully reflect their fundamentals.

- Prioritize resilience and sleep better at night by reviewing 62 resilient stocks with low risk scores, focused on stocks with lower risk profiles and sturdier business metrics.

- Spot under the radar potential by scanning the screener containing 22 high quality undiscovered gems, where strong fundamentals have yet to attract widespread attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.