Assessing Erie Indemnity (ERIE) Valuation After Investor Concerns And Earnings Uncertainty

Erie Indemnity Company Class A ERIE | 249.51 | +1.02% |

Erie Indemnity (ERIE) has drawn fresh attention after its shares hit a new 52 week low of US$269.74, following a 6.30% single day drop and a 29.02% 1 year decline.

That new 52 week low comes after a 1 year total shareholder return decline of 26.7%, although the 3 year and 5 year total shareholder returns of 23.38% and 21.18% suggest longer term gains, while recent momentum has been fading.

If this drop has you reassessing opportunities around financials and insurance names, it could be a good moment to broaden your watchlist with 23 top founder-led companies.

So with Erie Indemnity sitting on a 52 week low after a 26.7% 1 year total return decline but still carrying solid 3 and 5 year gains, is this weakness a buying opportunity, or is the market already pricing in future growth?

Price-to-Earnings of 22.8x: Is it justified?

On the numbers we have, Erie Indemnity screens as expensive on a P/E of 22.8x, given the last close of $282.94 and how peers are priced.

The P/E ratio compares the current share price to earnings per share, so a higher multiple usually means investors are paying more today for each dollar of current earnings. For an insurance business where steady profitability is common, a premium P/E often implies the market is factoring in stronger quality of earnings or more resilient growth than the average insurer.

Here, that premium is clear. ERIE's P/E of 22.8x sits well above both the US Insurance industry average of 12.5x and the peer group average of 12.2x, and also above an estimated fair P/E of 16.2x that our work suggests the market could eventually lean toward if expectations cool.

Result: Price-to-Earnings of 22.8x (OVERVALUED)

However, you still need to weigh risks, such as a potential de rating from that premium P/E or a slowdown in revenue and net income growth.

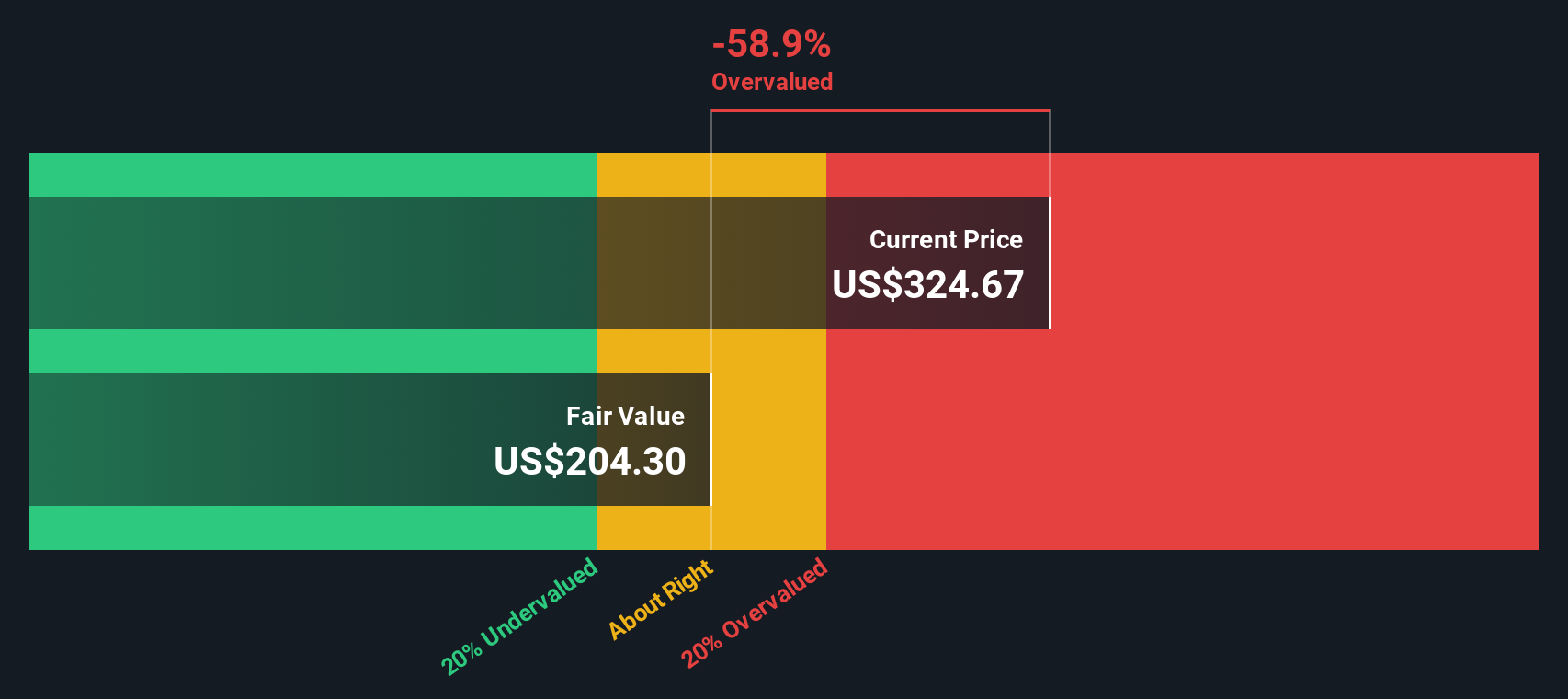

Another View: What Our DCF Model Says

While the 22.8x P/E suggests Erie Indemnity is priced richly, our DCF model points the same way. With the shares at $282.94 versus an estimated future cash flow value of $228.07, the stock screens as overvalued on this second yardstick too. If both methods are signaling rich valuation, how comfortable are you with the market’s optimism?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Erie Indemnity for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Erie Indemnity Narrative

If you see the data differently or would rather test your own assumptions directly, you can build a full Erie Indemnity view in minutes, starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Erie Indemnity.

Looking for more investment ideas?

If Erie Indemnity has sharpened your focus, do not stop here. Use the Simply Wall St Screener to uncover other opportunities that match your style and risk comfort.

- Target potential value opportunities by reviewing our list of 55 high quality undervalued stocks that pair solid fundamentals with more modest pricing.

- Strengthen your income focus by scanning 16 dividend fortresses that aim to combine higher yields with more resilient payouts.

- Tilt toward stability by checking 85 resilient stocks with low risk scores that stand out for lower risk scores and more resilient profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.