Assessing F5 (FFIV) Valuation After Raised Guidance And Strong Quarter In AI Security And Multicloud

F5, Inc. FFIV | 0.00 |

Why F5’s latest quarter is back in focus

F5 (FFIV) is back on investors’ radar after reporting quarterly results that showed higher revenue and profit, raising full year revenue growth guidance and pointing to firm demand in hybrid multicloud and application security.

That upbeat earnings release sits alongside strong recent share price momentum, with a 1-day share price return of 1.17% and a 90-day share price return of 24.75%. The 3-year total shareholder return of 155.95% points to gains that extend beyond the latest quarter.

If you are looking for other ways to position around AI driven infrastructure and security, it could be worth scanning 40 AI infrastructure stocks

With F5 shares up 24.75% over 90 days and now trading slightly above the average analyst target, yet still showing an estimated 13.06% intrinsic discount, the key question is whether there is still an opportunity for investors to consider or if the market is already fully reflecting expectations for future growth.

Most Popular Narrative: 2.3% Overvalued

F5 closed at $345.02 compared with a most popular narrative fair value of $337.40, so the narrative currently places the stock slightly above its modelled worth using an 8.67% discount rate.

The ongoing shift to high-margin, recurring software and SaaS subscription revenue, along with strong renewal and expand activity from existing customers, is improving revenue visibility and predictability while supporting operating margin and EPS growth. Effective operational discipline, evident in robust cash flow, continued cost management, and targeted share repurchases, enhances the company's ability to drive EPS growth, maximize shareholder returns, and weather industry cyclicality.

Want to see what sits behind that comment on margins and cash flow? The narrative leans on specific revenue, profit and valuation assumptions that may surprise you.

Result: Fair Value of $337.40 (OVERVALUED)

However, there are still pressure points to watch, including slower take up of software and SaaS offerings, as well as intense competition from both hyperscalers and specialist security vendors.

Another way to look at F5’s valuation

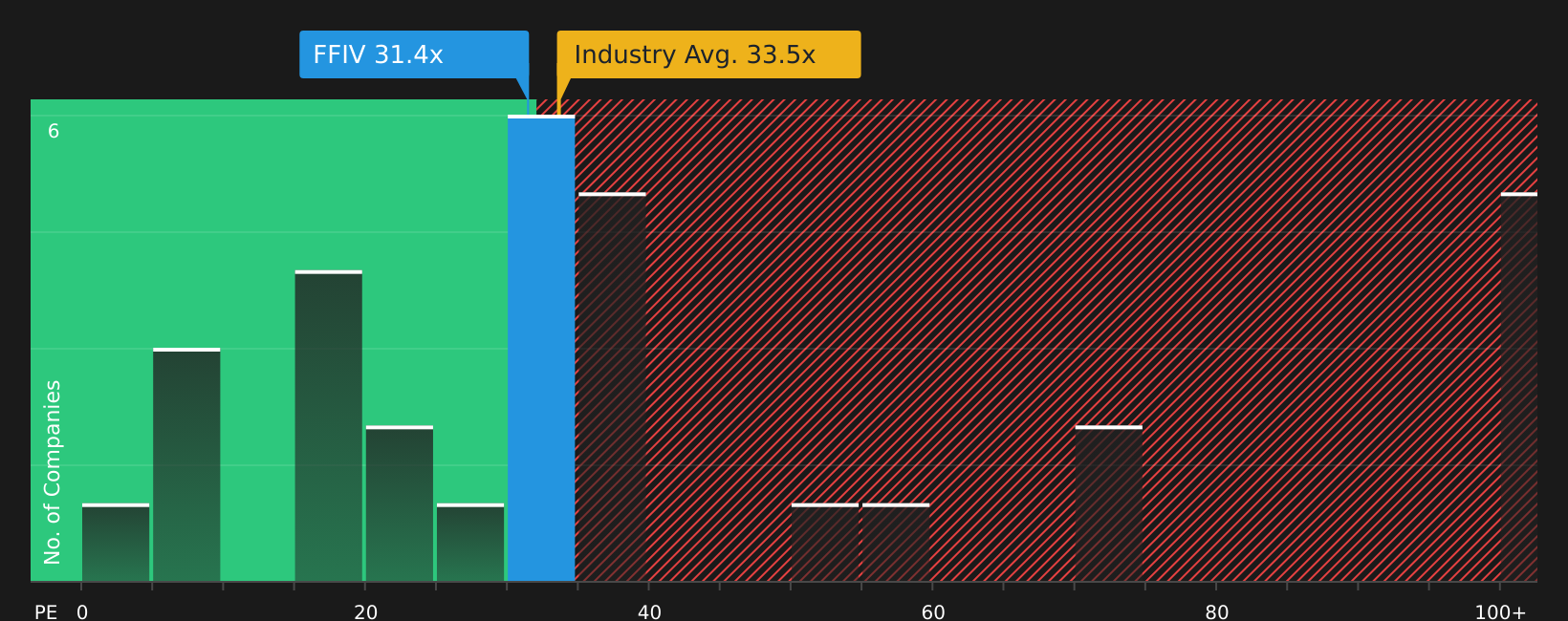

While the narrative fair value of $337.40 suggests F5 is slightly overvalued, the current P/E of 27.5x tells a different story. It sits well below the peer average of 91.9x and only just under a fair ratio of 28.9x. This points to tighter valuation risk than the headline gap implies. So which signal should carry more weight for you right now?

Next Steps

The mix of upbeat signals and clear watchpoints makes this a stock you may want to assess on your own terms by using the full breakdown of 4 key rewards and 1 important warning sign

Ready for more investment ideas?

If you stop at just one stock, you risk missing other opportunities that could fit your goals even better, so broaden your watchlist while momentum is on your side.

- Target potential mispricing by scanning 51 high quality undervalued stocks that pair solid fundamentals with room for the market to reassess expectations.

- Strengthen your income playbook by hunting through 12 dividend fortresses built around higher yields and balance sheet support.

- Prioritise resilience by focusing on 71 resilient stocks with low risk scores where financial risk scores sit on the lower side.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.