Assessing First Advantage (FA) Valuation After A Strong Short Term Share Price Rebound

First Advantage Corp. FA | 0.00 |

Recent share performance and business snapshot

First Advantage (FA) has drawn fresh attention after a strong recent share move, with the stock up 3.6% on the day, 5.7% over the past week and about 21.8% over the past month.

That move sits against a mixed return profile, with shares up about 38.1% over the past 3 months but down roughly 6.6% over the past year, and a market value near US$2.63b.

The recent 3 month share price return of 38.1% contrasts with a 1 year total shareholder return that is down 6.6%. This indicates that momentum has improved in the short term as investors reassess growth prospects and risks around First Advantage at a share price of US$15.9.

If this kind of move has you looking beyond a single stock, it could be a good moment to see what else is setting up for potential growth through our curated list of 21 top founder-led companies

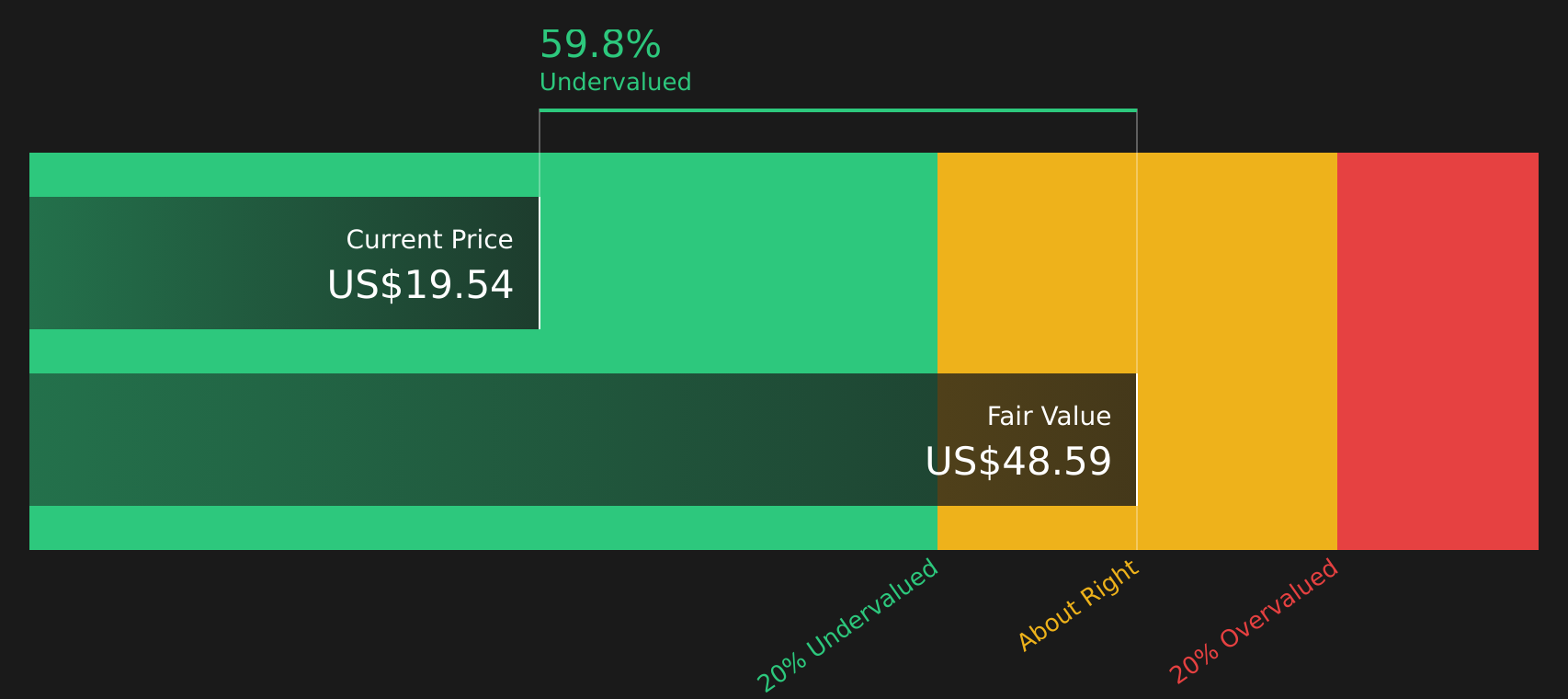

With First Advantage trading at US$15.9, annual revenue of US$1.61b and annual net income of US$8.54m, plus a value score of 3 and an indicated intrinsic discount, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 6% Overvalued

With the most followed narrative pointing to a fair value of $15 against a last close of $15.9, the current price sits slightly above that framework while still leaning on long term growth assumptions.

Ongoing investments in proprietary AI-enabled technology, automation, and integrated platforms (particularly following the Sterling acquisition) are unlocking operational efficiencies and enabling more high-margin value-added services, creating potential for margin expansion and higher net earnings.

Want to see what kind of revenue path and margin profile those investments are built around? The narrative leans on stronger profitability and a richer earnings multiple to bridge from today’s earnings base to that fair value.

Result: Fair Value of $15 (OVERVALUED)

However, that story hinges on steady hiring volumes and successful integration of Sterling. Any stumble there could quickly challenge the earnings and fair value narrative.

Another way to look at value

The most followed narrative points to a fair value of $15, suggesting First Advantage is about 6% above that mark at $15.9. Yet our DCF model paints a very different picture, with a future cash flow value of $41.94, or roughly 62% above the current price. Which framework do you find more convincing: a multiple based story or a cash flow based one?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out First Advantage for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With a mix of optimism and caution running through this story, it makes sense to look at the full picture yourself and then move quickly to decide what you think about First Advantage by weighing its 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If First Advantage has your attention, do not stop here. Widen your watchlist now so you are not late to other potential opportunities.

- Target quality at a discount by scanning for companies that look mispriced on fundamentals using the 46 high quality undervalued stocks.

- Strengthen your core holdings by focusing on financially robust businesses through the solid balance sheet and fundamentals stocks screener (46 results).

- Hunt for potential future leaders before the crowd notices with the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.