Assessing First National Bank Alaska (OTCPK:FBAK) Valuation After Its Latest First Quarter 2026 Earnings Release

FIRST NATIONAL BANK ALASKA FBAK | 0.00 |

First quarter earnings set the tone

First National Bank Alaska (FBAK) recently released first quarter 2026 results, reporting net interest income of US$48.98 million and net income of US$21.17 million. These figures give investors fresh insight into the bank’s current profitability.

FBAK's share price has gained 10.42% over the past 90 days and delivered a 44.66% total shareholder return over the past year, indicating that momentum has been building around the stock as investors review these latest earnings figures.

If you are looking beyond regional banks for your next idea, this could be a good moment to widen the lens and check out 19 top founder-led companies

With the stock up sharply over the past year and an estimated 24% discount to intrinsic value, the key question is whether FBAK still offers mispricing or whether the market is already baking in brighter days ahead.

Price-to-Earnings of 13.3x: Is it justified?

On a P/E of 13.3x and a last close of $339, FBAK trades at a richer earnings multiple than both the wider US Banks industry and its direct peers.

The P/E ratio compares the current share price to earnings per share. A higher P/E usually means investors are willing to pay more for each dollar of earnings. For a bank like FBAK, that can reflect expectations around earnings quality, growth, or perceived resilience in its core Alaska focused franchise.

Here, the data shows FBAK is priced above both benchmarks. The stock trades on a P/E of 13.3x, compared with 11.1x for the US Banks industry and 11.9x for its peer group. This suggests the market is attaching a premium to its earnings rather than marking it in line with the sector averages.

Given this set up, the current multiple implies investors are accepting a higher entry price than for typical US banks, even though the comparison points indicate cheaper alternatives on a pure earnings basis.

Result: Price-to-Earnings of 13.3x.

However, investors still need to weigh concentration in Alaska and the relatively higher P/E, as both could amplify sensitivity to local conditions or earnings disappointments.

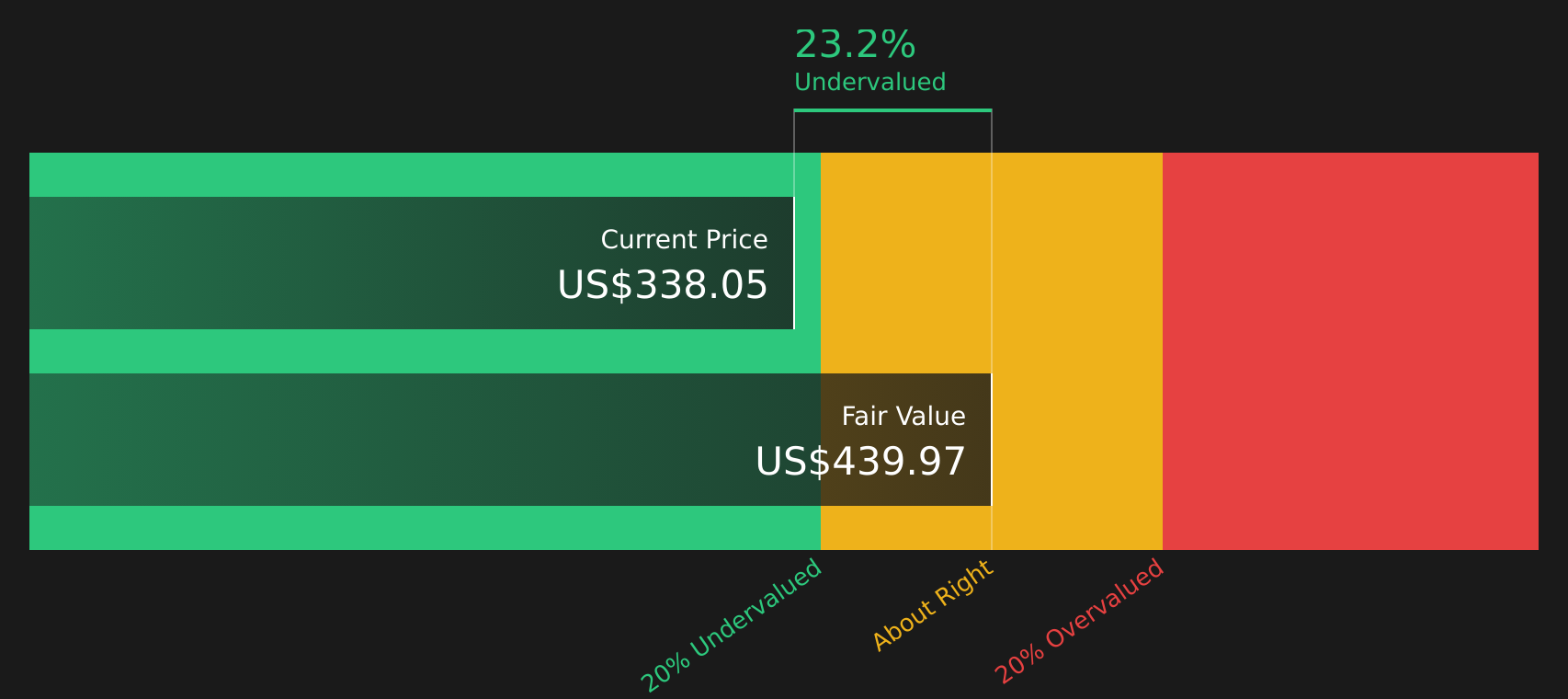

Another view: cash flows tell a different story

While the P/E of 13.3x makes FBAK look expensive next to the US Banks industry and peers, the SWS DCF model points in the opposite direction. On that framework, the stock price of $339 sits about 24% below an estimated fair value of $444.08, which presents the recent premium multiple in a very different light. For you, the tension is whether to rely on what earnings multiples indicate today or on what long term cash flow estimates suggest about the future.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out First National Bank Alaska for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With a mix of positives and concerns in the story so far, it makes sense to move quickly, review the numbers yourself and decide where you stand. To get a balanced view of both the potential benefits and the key risks, start with these 2 key rewards and 1 important warning sign

Looking for more investment ideas?

Do not stop your research with a single stock. Take a few minutes to scan wider opportunities and you might spot something that fits your goals even better.

- Target reliable income by reviewing companies in the 13 dividend fortresses.

- Hunt for potential bargains using the screener containing 21 high quality undiscovered gems.

- Prioritize resilience by checking stocks in the 65 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.