Assessing FirstEnergy (FE) Valuation As New Capital Plan And Regulatory Priorities Take Shape

FirstEnergy Corp. FE | 0.00 |

Event driven look at FirstEnergy after new capital and regulatory moves

FirstEnergy (FE) has put a fresh capital and regulatory blueprint in front of investors, pairing a new US$3b universal shelf registration with updated long term plans and a senior notes exchange extension.

At a share price of US$46.42, FirstEnergy’s recent moves on the US$3b shelf registration, updated regulatory roadmap, and the JCP&L senior notes exchange come against a backdrop of mixed momentum. The 1 day share price return of 1.71% contrasts with a 90 day share price return that is down 8.69%, while the 1 year total shareholder return of 18.83% underlines how income has supported long term holders.

If you want to see how other grid and infrastructure stocks are setting up around similar themes, it is worth scanning our dedicated 33 power grid technology and infrastructure stocks

With revenue of US$15.3b, net income of US$1.1b and a share price sitting at US$46.42 compared with an average analyst target of US$52.23, is FirstEnergy quietly offering value, or has the market already priced in its future growth?

Most Popular Narrative: 11.1% Undervalued

With the most followed narrative putting FirstEnergy's fair value at US$52.23 against a last close of US$46.42, the story hinges on regulated investment and earnings power rather than short term moves.

Large-scale infrastructure modernization and grid hardening initiatives, including the $28 billion investment plan through 2029 and a 15% CAGR in transmission rate base, enable higher returns on equity, improved reliability, and ultimately enhance net margins and earnings growth.

Curious what kind of revenue path and margin reset are needed to support that valuation and still justify a lower future earnings multiple? The narrative leans on compounding grid investments, tighter cost control, and a specific mix of growth, profitability and discount rate assumptions that do a lot of heavy lifting in the model.

Result: Fair Value of US$52.23 (UNDERVALUED)

However, this depends on regulators cooperating, and heavy grid spending or faster decarbonization rules could pressure free cash flow and eventually dilute earnings per share.

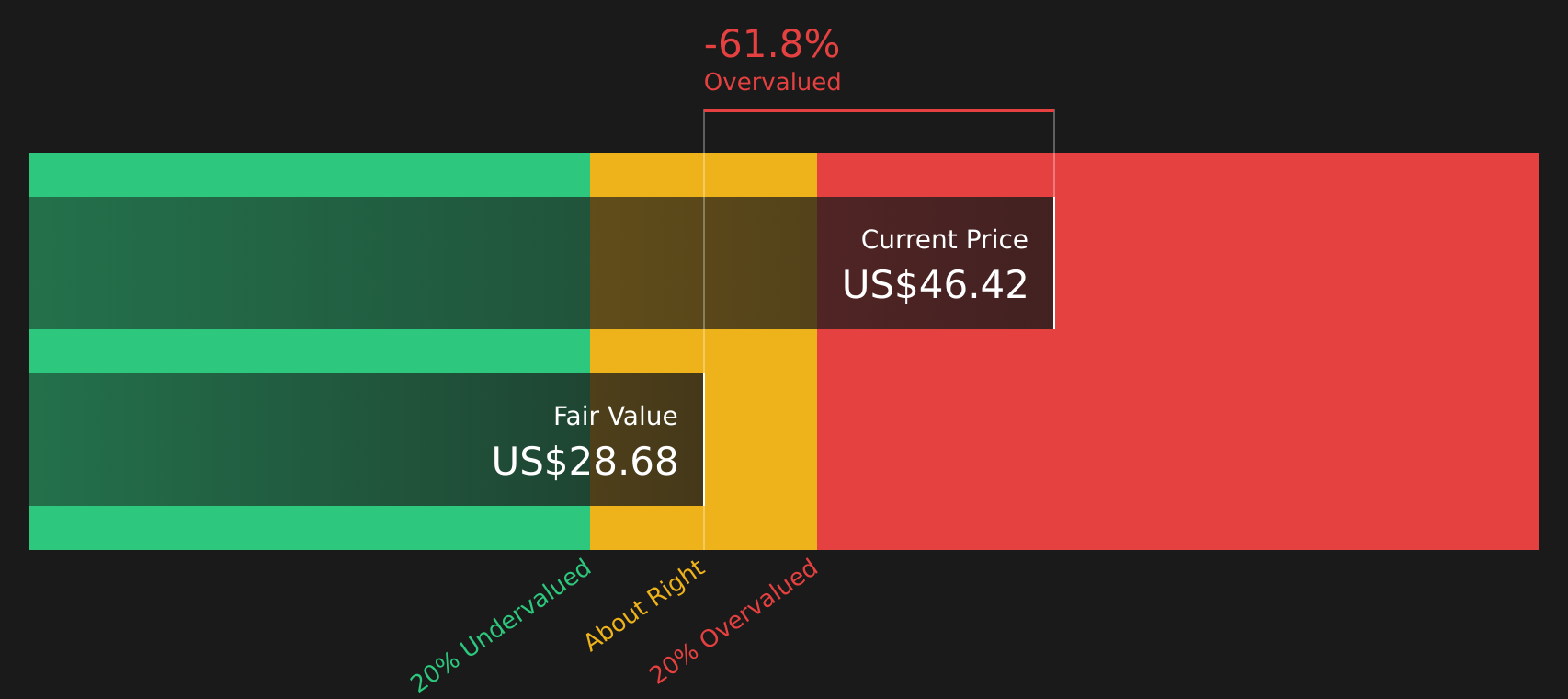

Another View: Cash Flow Model Paints A Very Different Picture

While the popular narrative suggests FirstEnergy is about 11.1% undervalued at US$52.23, the Simply Wall St DCF model points the other way. On that basis, the stock at US$46.42 sits well above an estimated future cash flow value of US$28.75, which raises the question of which yardstick you trust more.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out FirstEnergy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of potential upside and clear risks in this article might feel finely balanced, so take a closer look at the data and move quickly to form your own view by weighing its 1 key reward and 3 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might suit your goals even better, so put a few fresh ideas on your radar.

- Spot potential value opportunities early by scanning screener containing 22 high quality undiscovered gems that combine strong fundamentals with relatively low market attention.

- Strengthen your core holdings by reviewing solid balance sheet and fundamentals stocks screener (46 results) focused on companies with healthier finances and more resilient balance sheets.

- Dial down portfolio stress by assessing 64 resilient stocks with low risk scores that score well on stability and lower overall risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.