Assessing Flywire (FLYW) Valuation After Strong Q1 Beat Penn State Deal And Buyback Completion

Flywire Corp. FLYW | 0.00 |

Q1 earnings and Penn State deal put Flywire (FLYW) in focus

Flywire (FLYW) is back on investors’ radar after first quarter 2026 results topped consensus expectations, a shift to net profit, a new Penn State education contract, and completion of a sizeable share repurchase program.

At a share price of $16.35, Flywire has posted a 30 day share price return of 33.69% and a 90 day share price return of 49.04%. The 1 year total shareholder return of 44.31% contrasts with a 3 year total shareholder return that is down 47.58%, suggesting recent momentum has picked up after a tougher stretch since listing.

If Flywire’s recent swing back into profit has you looking for other payment and software driven growth stories, you can widen your search with 39 AI infrastructure stocks

With the stock up sharply over the past quarter, net income back in the black and the price still below the average analyst target, the key question is whether Flywire is still mispriced or whether markets are already crediting future growth.

Most Popular Narrative: 30% Overvalued

Simply Wall St's most followed narrative places Flywire's fair value at $16.31, very close to the last close of $16.35. It builds a detailed case around long term earnings power using a 7.2% discount rate.

Flywire is experiencing robust growth outside traditional markets, with international education revenues in regions like Singapore, Spain, France, Mexico, and Japan outpacing company averages, ongoing global expansion efforts and market share gains are expected to drive long-term revenue growth and diversify dependency on the mature Big 4 education markets.

Read the complete narrative. Read the complete narrative.

Want to see what is built into that fair value? The narrative leans heavily on compounding revenue, rising margins, and a richer earnings multiple. The full set of assumptions is where the story really sits.

Result: Fair Value of $16.31 (OVERVALUED)

However, student visa pressure in key education markets and competition from other payment providers could easily cap transaction growth and challenge the current fair value case.

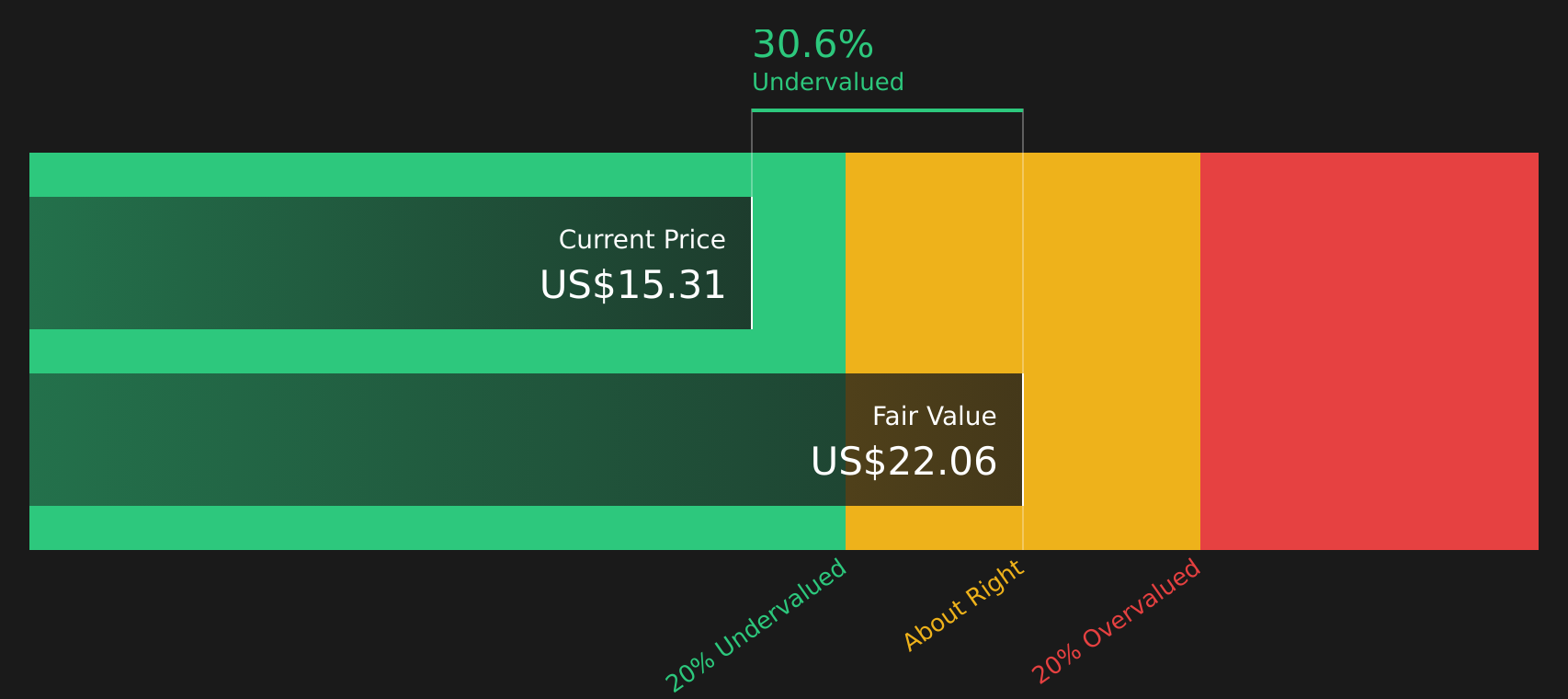

Another View: Cash Flows Point to Undervaluation

While the popular narrative pegs Flywire at roughly fair value around $16.31, our DCF model paints a different picture. On this view, Flywire is priced below an estimated future cash flow value of $21.76 per share, which suggests the market may be underpricing its cash generation potential. Which story do you think fits better with your own expectations?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Flywire for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between fair value and upside potential, it makes sense to move quickly and test the assumptions against your own expectations. To see what investors are optimistic about and pressure test those views against the underlying data, start with the 3 key rewards

Looking for more investment ideas?

If Flywire has sparked fresh thinking about your portfolio, do not stop here. Broaden your opportunity set with a few focused stock idea lists built from clear fundamentals.

- Target potential value upside with companies that combine quality fundamentals and attractive pricing using the 45 high quality undervalued stocks.

- Prioritise resilience and capital preservation by scanning stocks flagged as having relatively low risk profiles through the 68 resilient stocks with low risk scores.

- Hunt for lesser known opportunities that still show strong financial foundations by checking the screener containing 23 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.