Assessing Hubbell (HUBB) Valuation After Recent Share Price Pullback And Conflicting Fair Value Signals

Hubbell Incorporated HUBB | 0.00 |

Recent share performance and business scale

Hubbell (HUBB) has drawn attention after the stock fell about 12% over the past month and about 8% over the past 3 months, prompting investors to reassess its recent run and current fundamentals.

The company, headquartered in Shelton, Connecticut, reports annual revenue of US$5.996b and net income of US$904.3m. Its operations are split between its Utility Solutions and Electrical Solutions segments, with most revenue generated in the United States.

While the share price has eased recently, with the 30 day share price return down 11.65% and the 90 day return down 8.03%, the 1 year total shareholder return of 26.22% and 5 year total shareholder return of 177.10% point to a stronger longer term trend.

If grids and electrification are on your radar, it could be worth broadening your watchlist. You can do this by using a screener focused on power grid technology companies such as 38 power grid technology and infrastructure stocks

With Hubbell shares easing in recent months but still showing strong multi year returns, and with the stock trading below the average analyst price target, the key question is whether there is still a buying opportunity or if the market is already pricing in further growth.

Most Popular Narrative: 12% Undervalued

At a last close of $482.03 versus a narrative fair value of $547.15 using a 10.28% discount rate, Hubbell is framed as having some upside based on consensus assumptions.

The Utility Solutions segment is experiencing organic growth resurgence, particularly in grid infrastructure, supported by strong transmission and substation markets due to increasing grid modernization and electrification. This growth trend should drive higher future revenues.

Want to see what level of revenue growth and margins sit behind that fair value gap? The narrative leans on earnings expansion and a richer future earnings multiple. Curious how those ingredients combine to justify the valuation path laid out for 2029?

Result: Fair Value of $547.15 (UNDERVALUED)

However, this narrative could be challenged if tariff and raw material cost inflation squeeze margins, or if weaker grid automation demand slows the Utility Solutions segment.

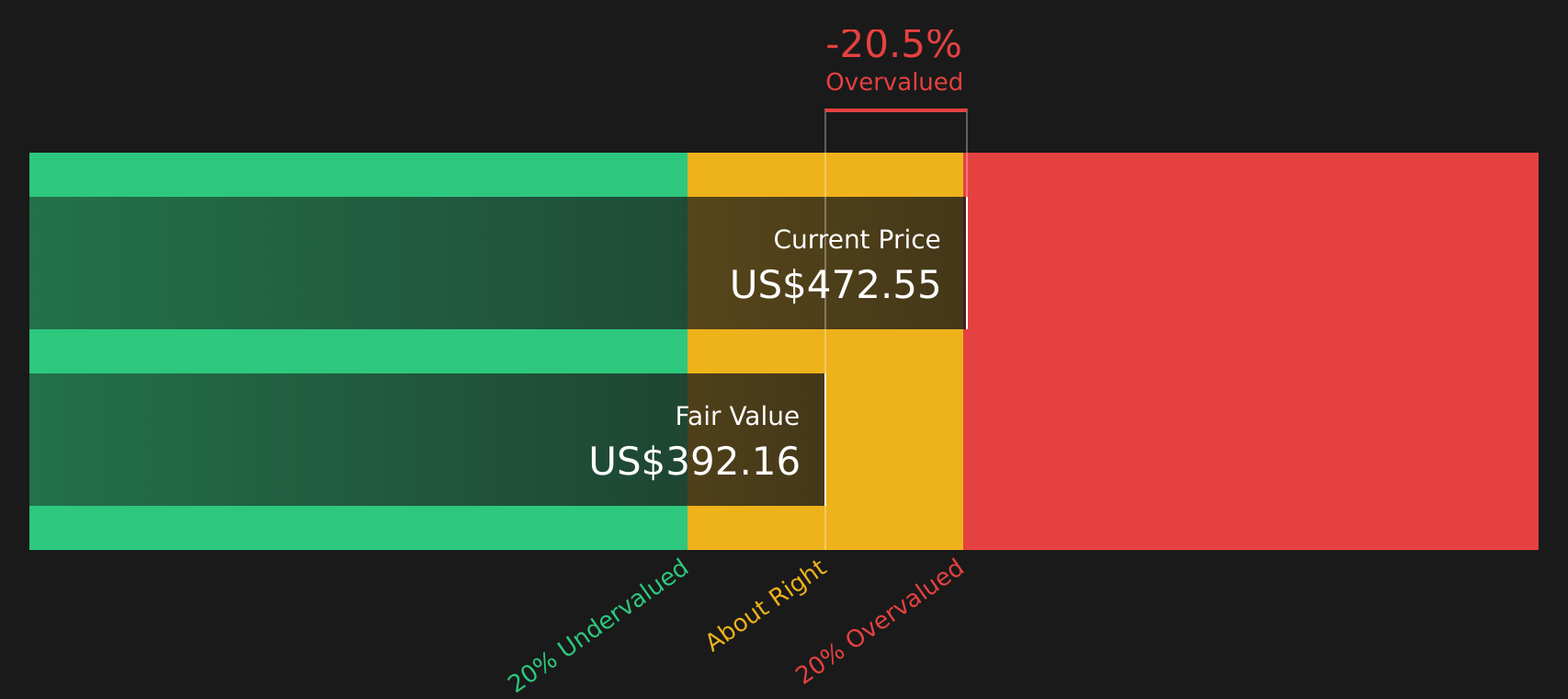

Another way to look at value

While the analyst narrative points to a fair value of $547.15, the Simply Wall St DCF model paints a very different picture, with an estimate of future cash flow value at $337.98. On that view, the current $482.03 share price looks expensive rather than cheap. Which story do you think is closer to reality?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hubbell for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals or a clear setup: either way, the next move is yours. Weigh the data, stress test your own thesis, and take a closer look at the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If Hubbell has sharpened your thinking about grids and valuation, do not stop here. Broaden your opportunity set now with a few focused stock idea lists.

- Target reliable cash generators by scanning 46 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their strengths.

- Strengthen your income stream by reviewing 14 dividend fortresses built around companies offering yields of 5% or more.

- Prioritise resilience first and hunt through 68 resilient stocks with low risk scores to see which stocks currently carry lower risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.