Assessing InterDigital (IDCC) Valuation After New IoT License And 6G ISAC Milestones

InterDigital, Inc. IDCC | 0.00 |

InterDigital (IDCC) is back in focus after two fresh catalysts: a new IoT patent license with a fintech payments player, and a high profile 6G ISAC technology showcase at the 2026 IEEE International Conference on Communications.

Even with the fresh IoT licensing deal and 6G ISAC showcase, InterDigital’s recent share price momentum has been weak, with the stock down 30% over the past month and 33% over the past quarter. At the same time, its 1 year total shareholder return of 19% and very large 3 and 5 year total shareholder returns suggest the longer term trend has been much stronger.

If this kind of wireless and AI story has your attention, it can be worth scanning for other potential opportunities using our screener of 33 AI small caps

So with InterDigital’s share price falling sharply in the short term, but longer term returns still strong, is the stock now trading below its true potential, or is the market already pricing in future growth?

Most Popular Narrative: 45.4% Undervalued

InterDigital’s most followed valuation narrative pegs fair value at $462.67 per share, well above the last close of $252.45, and anchors this view on how earnings, margins, and future licensing economics could play out.

With a business model exhibiting high incremental margins, where major license or renewal agreements can be close to 100% gross margin and significant free cash flow (expected to nearly double to over $400 million in 2025), the company's strong operational leverage, active share repurchases, and increased dividends enhance its ability to deliver higher earnings per share and shareholder returns over the long term.

Want to see what kind of revenue path and margin profile sit behind that fair value number. The narrative leans on recurring licenses, cautious growth, and a richer future earnings multiple that is very different from where the stock trades today.

Result: Fair Value of $462.67 (UNDERVALUED)

However, that upbeat story could be challenged if revenue growth stays flat while profit margins trend lower, or if regulatory pressure reshapes patent licensing economics.

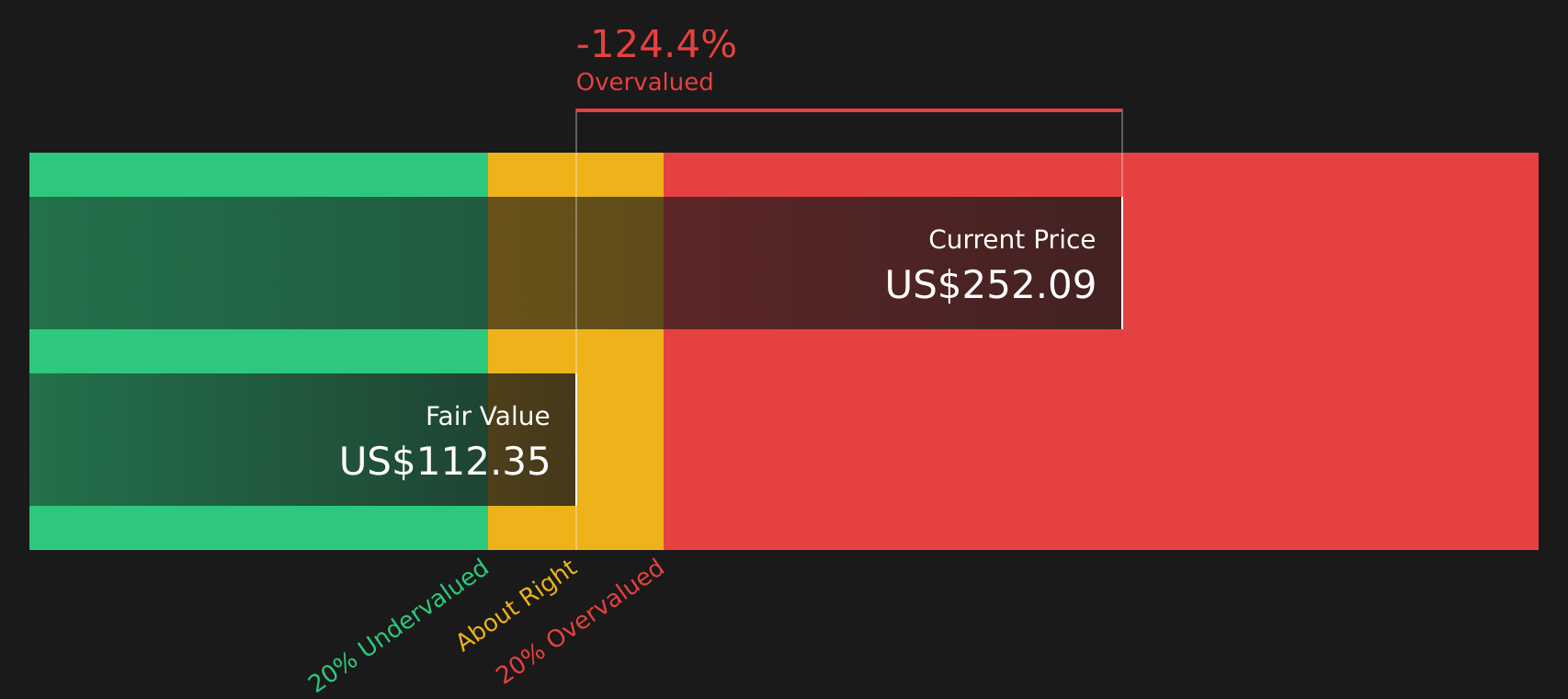

Another View On Value: Cash Flows Tell A Different Story

That 45.4% undervalued narrative leans heavily on earnings multiples, but our DCF model presents a very different perspective, with InterDigital trading at $252.45 compared with an estimated future cash flow value of $112.72, which appears overvalued on this approach.

When one method points to upside and another signals downside, it puts the focus back on your assumptions about how repeatable current cash flows really are and how long they can last before competition or regulation starts to have an impact.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out InterDigital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between upside potential and valuation risk, it makes sense to act promptly, review the numbers yourself, and weigh up the 3 key rewards.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities, so use these focused stock lists to quickly spot ideas that fit your style.

- Target reliable income by reviewing companies described as 9 dividend fortresses and see which payouts might suit your portfolio goals.

- Hunt for potential mispricings by checking the 47 high quality undervalued stocks that pair fundamentals with appealing valuations.

- Strengthen portfolio resilience by scanning the 64 resilient stocks with low risk scores that combine lower risk scores with more stable profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.