Assessing Kinsale Capital Group (KNSL) Valuation After A Sharp Pullback From Recent Highs

Kinsale Capital Group, Inc. KNSL | 0.00 |

Kinsale Capital Group stock performance snapshot

Kinsale Capital Group (KNSL) has seen its stock decline around 27% year to date, with the price at about US$295.40 and a total return over the past year down roughly 38%.

Recent trading has been weak, with the 7 day share price return down 5.33% and the 90 day share price return down 22.97%, while the 5 year total shareholder return remains up 81.66%. This suggests recent momentum has faded after a strong longer term run.

If Kinsale's pullback has you thinking about where else to put fresh capital, this can be a good moment to broaden your search and uncover 20 top founder-led companies

With Kinsale trading well below its recent highs yet still carrying a sizeable market value of about US$7.0b, is this pullback an opportunity to buy a quality insurer at a discount, or is the market already pricing in future growth?

Most Popular Narrative: 16.7% Undervalued

At a last close of about $295.40 versus a narrative fair value of roughly $354.67, the core question is whether Kinsale's earnings profile justifies that gap.

The secular shift of risks from standard markets into the E&S channel, particularly for homeowners and catastrophe-exposed lines (e.g., in California, Texas, and coastal regions), is broadening Kinsale's long-term premium base and enabling sustainable top-line growth even as competition intensifies in select lines.

Curious what earnings path and profit margins are baked into that higher fair value. The narrative leans on slower growth, firm profitability, and a richer future P/E. The full story is in how those pieces fit together over time.

Result: Fair Value of $354.67 (UNDERVALUED)

However, you also need to weigh the risk that slower premium growth and tougher competition in key lines could pressure margins, especially if inflation and catastrophe losses become more severe.

Another angle on valuation

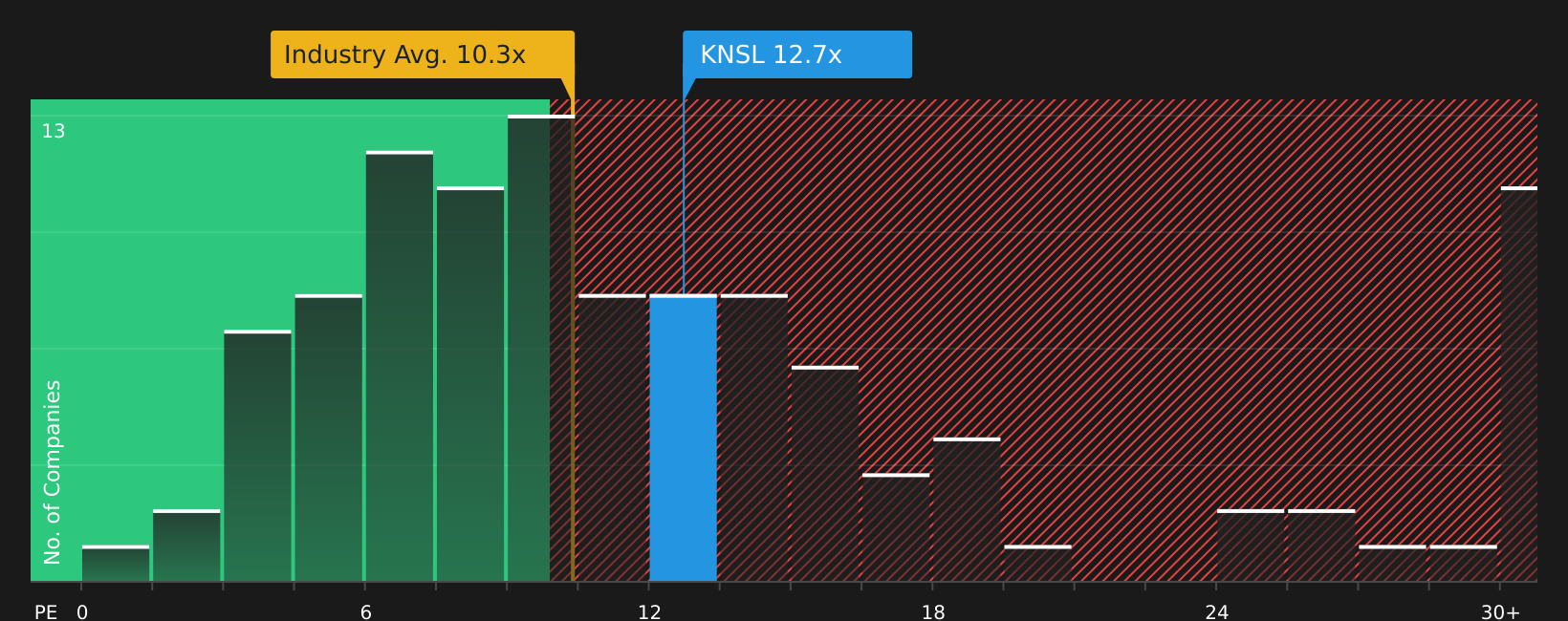

The narrative and analyst targets suggest Kinsale looks undervalued, but the P/E tells a different story. At about 12.9x, the stock trades richer than the US Insurance industry at 10.7x and its own fair ratio of 10.7x. This points to less room for error if growth underwhelms.

That premium versus both peers at 7x and the fair ratio implies investors are already paying up for quality and execution. As a result, any slip in earnings or reserve confidence could hit the share price faster than a textbook model suggests. Does that trade off match the role you want this stock to play in your portfolio?

Next Steps

If this mix of caution and opportunity feels familiar, use it as a prompt to look at the underlying data, compare it with your own expectations, and move before sentiment shifts too far in either direction by weighing 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

Do not stop your research with a single stock; widen your watchlist now and give yourself more options before the next set of opportunities moves away.

- Target quality at a discount by scanning 46 high quality undervalued stocks that combine solid fundamentals with prices that may still be catching up.

- Prioritise resilience by checking 63 resilient stocks with low risk scores that score well on stability and financial strength when conditions get tougher.

- Get ahead of the crowd by reviewing the screener containing 22 high quality undiscovered gems that most investors are not watching yet but already show strong underlying metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.