Assessing Ladder Capital (LADR) Valuation As Options Volatility And Analyst Caution Intensify

Ladder Capital Corp. Class A LADR | 0.00 |

Options traders have zeroed in on Ladder Capital (LADR) after the August 21, 2026 $2.50 call option showed some of the highest implied volatility, coinciding with analysts maintaining a strong sell rating.

Beyond the options spike, Ladder Capital’s recent 1-day share price return of 2.87% and 90-day share price return of 2.36% sit against a year to date share price decline of 6.31%. Its 5-year total shareholder return of 31.67% points to a very different long term picture of how dividends and price moves have combined for holders.

If this kind of volatility has you thinking about where else to look in the market, it could be a useful moment to scan for other opportunities through 20 top founder-led companies

So with analysts firmly bearish, options pricing pointing to a sharp move, and the stock trading below its US$12.32 target, is Ladder Capital quietly undervalued here or is the market already pricing in any future growth?

Price-to-Earnings of 24.1x: Is it justified?

On a P/E of 24.1x against a last close of $10.40, Ladder Capital currently looks expensive compared with its own fair P/E estimate and Mortgage REIT peers.

The P/E ratio tells you how much investors are paying today for each dollar of current earnings, which matters a lot for an income focused REIT with forecast profit growth on the table.

Here, the picture is clear. Ladder Capital is described as expensive on a P/E of 24.1x versus an estimated fair P/E of 15.2x and a US Mortgage REITs industry average of 11.2x. This signals the market is paying a premium relative to both its peer group and the level that regression based models suggest could be more in line if sentiment cools.

Result: Price-to-Earnings of 24.1x (OVERVALUED)

However, investors still face risks if property values weaken or commercial borrowers struggle to refinance, which could pressure loan performance and any implied valuation premium.

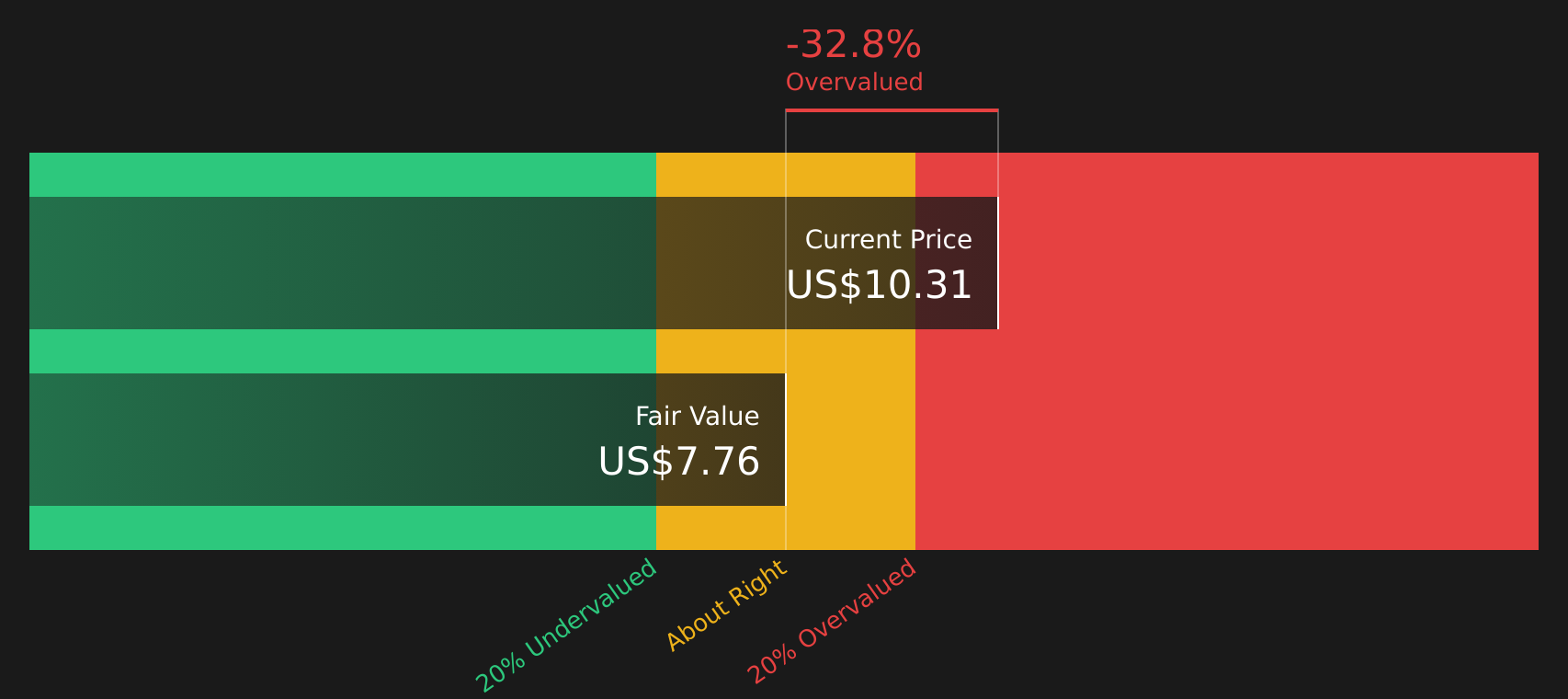

Another View: Our DCF Model Sees Less Upside

While the P/E ratio presents Ladder Capital as expensive compared with peers, the SWS DCF model goes a step further and values the stock at $7.74 per share, which is below the current $10.40 price. That suggests limited margin of safety if cash flows follow this path.

For readers who want to see how this cash flow view is built, and how sensitive it is to different assumptions, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ladder Capital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this setup feels mixed to you, that is exactly the point. The stock carries both risks and potential rewards, so take a moment to review the 1 key reward and 4 important warning signs

Looking for more investment ideas?

Before moving on, take a moment to scan other opportunities so you are not relying on a single stock when there may be better fits for your goals.

- Target more resilient payers by checking out companies labelled as 9 dividend fortresses that may appeal if reliable income is high on your list.

- Hunt for potential bargains by reviewing the 46 high quality undervalued stocks and see which stocks line up better with the kind of pricing you prefer.

- Strengthen your watchlist by focusing on the solid balance sheet and fundamentals stocks screener (46 results) so you can prioritise businesses with sturdier financial foundations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.