Assessing Liberty Energy (LBRT) Valuation After A Strong Share Price Run

Liberty Energy, Inc. Class A LBRT | 0.00 |

Recent performance context for Liberty Energy

Liberty Energy (LBRT) has drawn fresh attention after a strong run in its share price, with the stock showing gains over the past week, month and past 3 months, alongside a year to date return above 70%.

Looking beyond the recent rally, Liberty Energy’s momentum has been building, with a 78.97% year to date share price return and a 190.62% total shareholder return over the past year at a latest share price of $33.79.

If you are assessing energy related opportunities, it may also be worth scanning companies exposed to power infrastructure trends using our 35 power grid technology and infrastructure stocks

With Liberty Energy trading at $33.79, close to an analyst price target of $32.77 but with an intrinsic value estimate implying a large discount, you have to ask whether there is real value here or whether the market already anticipates additional growth.

Most Popular Narrative: 17.1% Overvalued

Liberty Energy's most followed narrative sets a fair value of $28.85 per share, which sits below the recent $33.79 close and frames the current optimism as rich.

Analysts have nudged the fair value estimate for Liberty Energy higher, with the implied price target moving from about $25.17 to roughly $28.85. This points to increased confidence around the company’s evolving mix of oil and gas completions and its growing Power business, despite geopolitical noise.

Want to understand why this valuation leans higher even with forecast earnings pressure? The narrative leans heavily on a revenue mix shift, firmer long term margins, and a richer future earnings multiple. Curious which specific growth and profitability assumptions have to line up for that price to make sense?

Result: Fair Value of $28.85 (OVERVALUED)

However, these assumptions could be knocked off course if completions activity softens, as flagged for 2025, or if Power projects take longer to contribute meaningfully.

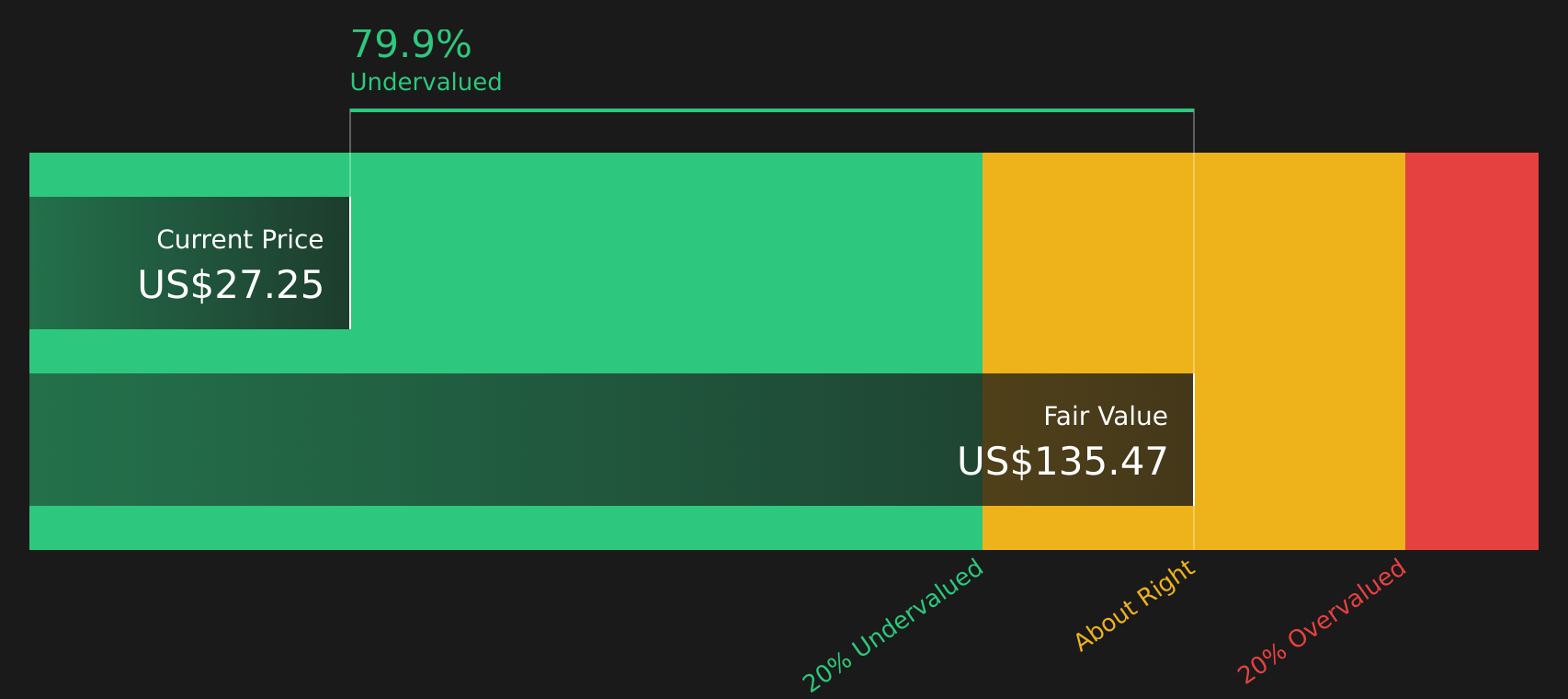

Another View: DCF Points To Deep Undervaluation

While the most popular narrative sees Liberty Energy as 17.1% overvalued at $33.79 versus a $28.85 fair value, the SWS DCF model paints a very different picture. On that framework, the shares trade about 76% below an estimated future cash flow value of $140.85, which is a significant gap for any investor to consider.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Liberty Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals on value and expectations, it helps to see the full picture quickly and decide where you stand using our 2 key rewards and 4 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you could miss sharper opportunities, so use the screener to quickly surface fresh ideas that fit your style.

- Target potential value opportunities by scanning 51 high quality undervalued stocks that combine quality fundamentals with attractive pricing.

- Prioritise resilience by reviewing 74 resilient stocks with low risk scores that focus on companies with lower risk scores and steadier profiles.

- Spot early standouts by checking the screener containing 25 high quality undiscovered gems that highlight quality businesses the market may not be focused on yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.