Assessing MetLife (MET) Valuation After Earnings Weakness And Completed Share Buyback

MetLife, Inc. MET | 0.00 |

MetLife earnings and buyback update

MetLife (MET) just released its fourth quarter and full year 2025 results, pairing higher reported revenue with lower net income and diluted EPS, alongside an update on its recently completed share repurchase program.

MetLife’s earnings release and buyback update appear to have weighed on sentiment in the short term, with a 7 day share price return of a 4.45% decline and a year to date share price return of a 5.03% decline, while the 5 year total shareholder return of 59.48% points to gains that have built up over a longer horizon.

If this earnings update has you reassessing financials as a whole, it could be a good moment to broaden your watchlist and check out 22 top founder-led companies as potential long term compounders beyond large insurers.

With the shares weaker over the past year despite revenue of US$77.08b and net income of US$3.38b, plus a completed US$1.10b buyback, you have to ask: is MetLife undervalued here, or is the market already pricing in future growth?

Most Popular Narrative: 17.9% Undervalued

MetLife’s most followed narrative pegs fair value at about $92.93 versus the last close of $76.28, framing the latest pullback against a higher long term earnings story built on retirement income agreements and international growth.

Strong, sustained premium and sales growth in high-potential international markets (Asia, Latin America, EMEA) positions MetLife to capitalize on growing middle-class wealth and increased insurance penetration, supporting robust long-term revenue and top-line growth.

Ongoing investment in digital transformation (AI-driven underwriting, process automation, embedded insurance partnerships, and tech-enabled distribution) enables MetLife to reduce acquisition and operating costs, improve customer engagement and retention, and, over time, boost net margins.

Curious how that growth story turns into a higher fair value estimate? The narrative leans on steady revenue expansion, rising margins, and a future earnings profile that does not rely on aggressive assumptions. The tension sits between moderated growth forecasts and a valuation multiple that still expects solid execution. Want to see exactly how those pieces fit together?

Result: Fair Value of $92.93 (UNDERVALUED)

However, you also need to weigh risks, such as weaker investment margins and commercial mortgage loan losses, which could pressure earnings and challenge the optimistic earnings power story.

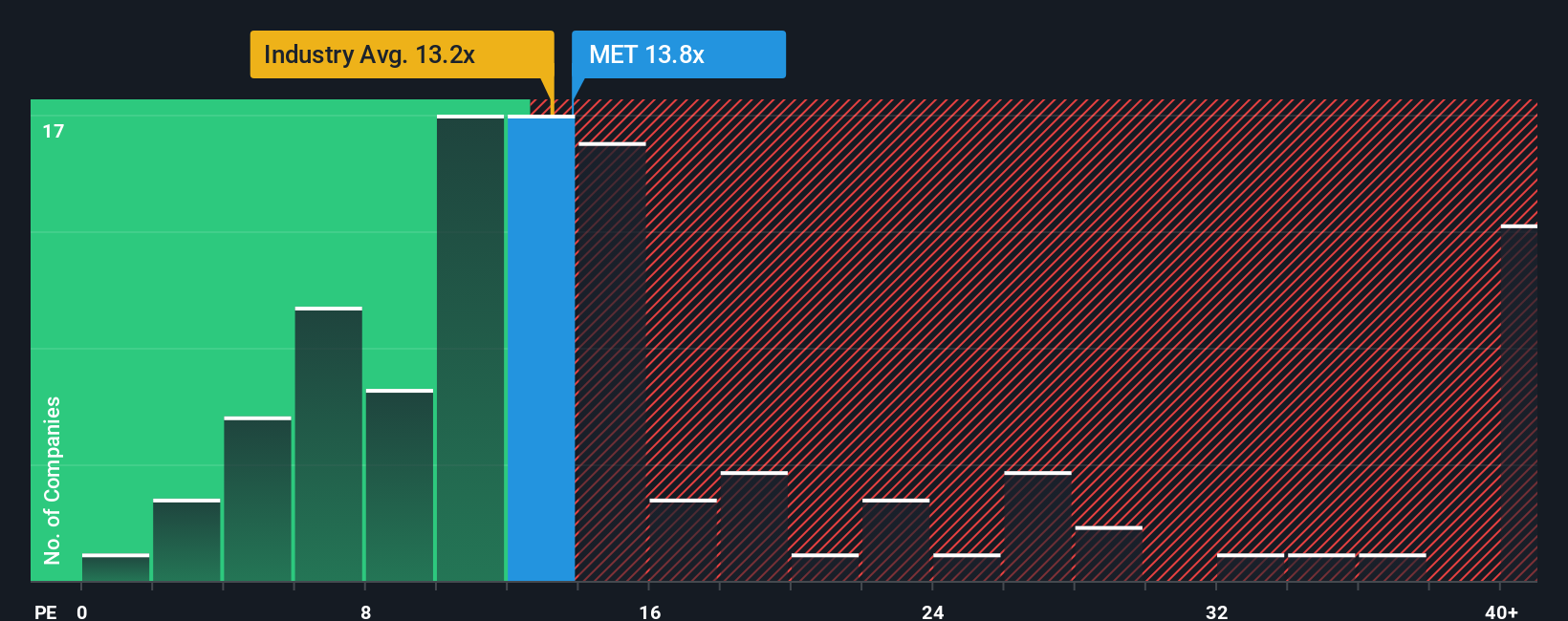

Another View: Earnings Multiple Sends Mixed Signals

Our fair value estimate of $92.93 suggests that MetLife is 17.9% undervalued. However, the current P/E of 15.8x is higher than both the US Insurance industry at 13x and the peer average at 13.9x, even though it remains below the 17.5x fair ratio. Is that a cushion or a value trap in the making?

Build Your Own MetLife Narrative

If you are not fully on board with this view or simply want to weigh the data yourself, you can build a customized MetLife story in just a few minutes, starting with Do it your way.

A great starting point for your MetLife research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If MetLife has sharpened your thinking, do not stop here. Broaden your search and line up a few more high quality candidates for your watchlist.

- Start with resilience and focus on companies that score well on balance sheet strength and fundamentals through our solid balance sheet and fundamentals stocks screener (45 results).

- Hunt for value and see which names our process flags as 52 high quality undervalued stocks that may warrant a closer look before others catch on.

- Spot early opportunities and scan our 25 elite penny stocks with strong financials for smaller businesses that still clear key financial quality hurdles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.