Assessing Morgan Stanley (MS) Valuation After Earnings Beat And Wealth Management Momentum

Morgan Stanley MS | 165.81 | -0.22% |

Morgan Stanley (MS) is back in focus after fourth quarter earnings beat expectations, with wealth management and institutional securities driving the result, and a 6% share price jump underscoring renewed investor attention.

Those results sit against a share price of $183.05, with a 90 day share price return of 11.71% and a 1 year total shareholder return of 36.56%. This suggests momentum has been building, while recent earnings, capital returns and fresh euro and US dollar bond issuance keep Morgan Stanley in the headlines.

If strong earnings at a major bank have you thinking about where capital could move next, it may be worth sizing up opportunities across fast growing stocks with high insider ownership.

After a 36.56% 1 year total return, earnings beats, and active capital management, the key question now is simple: is Morgan Stanley still priced below its true worth, or are markets already baking in years of future growth?

Most Popular Narrative: 8% Overvalued

At a last close of $183.05 against a narrative fair value of $169.52, the current price sits above what this widely followed story suggests, raising clear questions about what is built into expectations.

The ongoing increase in global wealth, combined with the accelerating intergenerational transfer of assets, is boosting demand for comprehensive advisory and wealth management solutions evidenced by record net new assets and a growing client base which should drive higher recurring fee-based revenue and long-term earnings growth.

Curious what kind of revenue growth, margin profile and future earnings multiple are baked into that fair value line? The narrative spells out a detailed roadmap for where earnings and valuation assumptions could go next.

Result: Fair Value of $169.52 (OVERVALUED)

However, this story can change quickly if passive products keep chipping away at fee based advisory, or if fintech competitors pull younger clients off Morgan Stanley’s platforms.

Another View: Earnings Multiple Paints A Different Picture

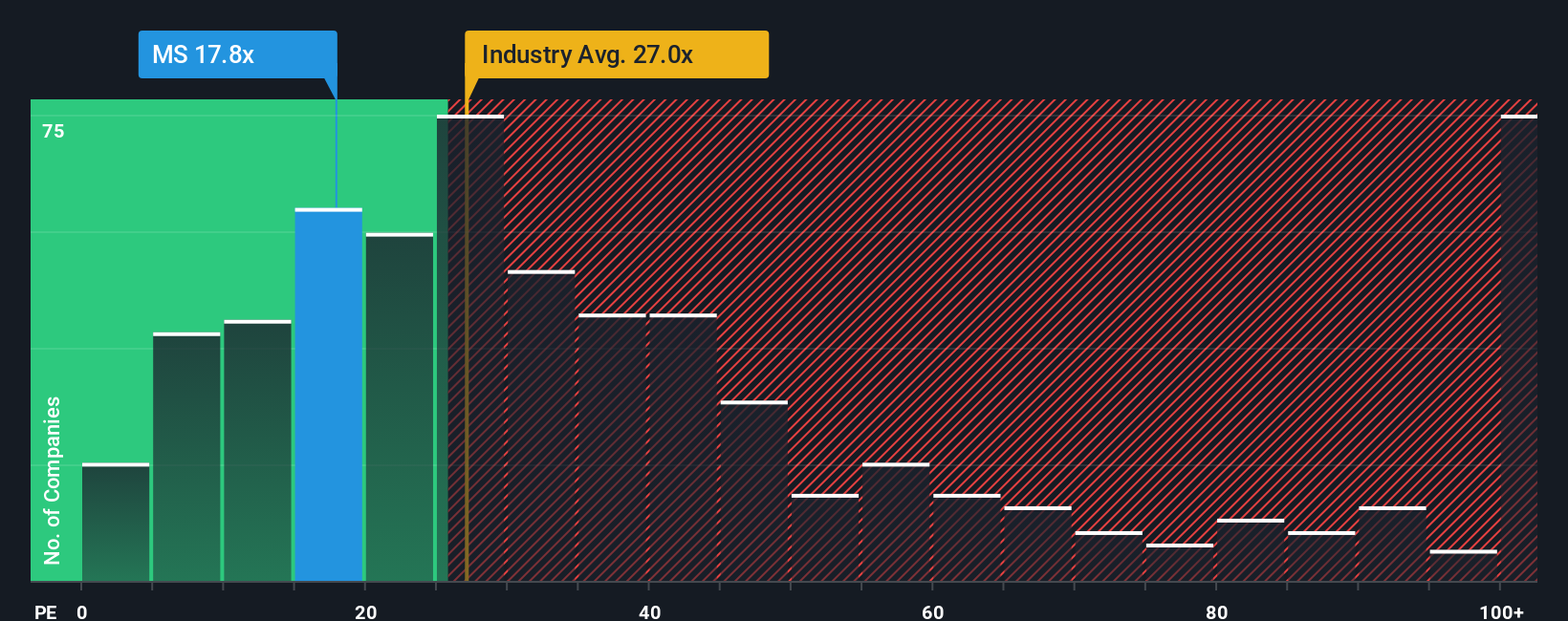

While the narrative fair value of $169.52 points to an 8% premium at $183.05, the earnings multiple tells a softer story. Morgan Stanley trades on a P/E of 17.8x, below the US market at 19.6x, the US Capital Markets industry at 25.9x, and a fair ratio of 19.5x, which suggests the market is not paying an especially rich price for each dollar of earnings. For you, that raises a simple question: is the risk really in overpaying here, or in assuming the story cannot keep evolving?

Build Your Own Morgan Stanley Narrative

If this story does not quite match how you see the numbers, you can run your own checks and build a custom view in minutes, Do it your way.

A great starting point for your Morgan Stanley research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Morgan Stanley is on your radar, do not stop there. Use Simply Wall Street screeners to quickly surface other potential ideas before the crowd gets there.

- Focus on value first and scan these 880 undervalued stocks based on cash flows that may be trading below what their cash flows imply.

- Target income potential by checking out these 12 dividend stocks with yields > 3% that aim to offer yields above 3%.

- Lean into future themes and review these 23 quantum computing stocks that are tied to advances in quantum computing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.