Assessing New York Times (NYT) Valuation After Earnings Growth, Buybacks And A Higher Dividend

New York Times Company Class A NYT | 79.34 79.34 | +0.42% 0.00% Pre |

New York Times (NYT) shares are in focus after the company reported fourth quarter and full year 2025 results, highlighted by higher revenue and net income, as well as completed buybacks and an increased quarterly dividend.

At a share price of $72.94, New York Times has seen momentum build recently, with a 7-day share price return of 7.09% and a 90-day share price return of 14.08%, alongside a 1-year total shareholder return of 48.48% that reflects strong recent compounding.

If this earnings-driven move has you thinking about where else growth stories might emerge, it could be a good moment to scan our 23 top founder-led companies for fresh ideas beyond media.

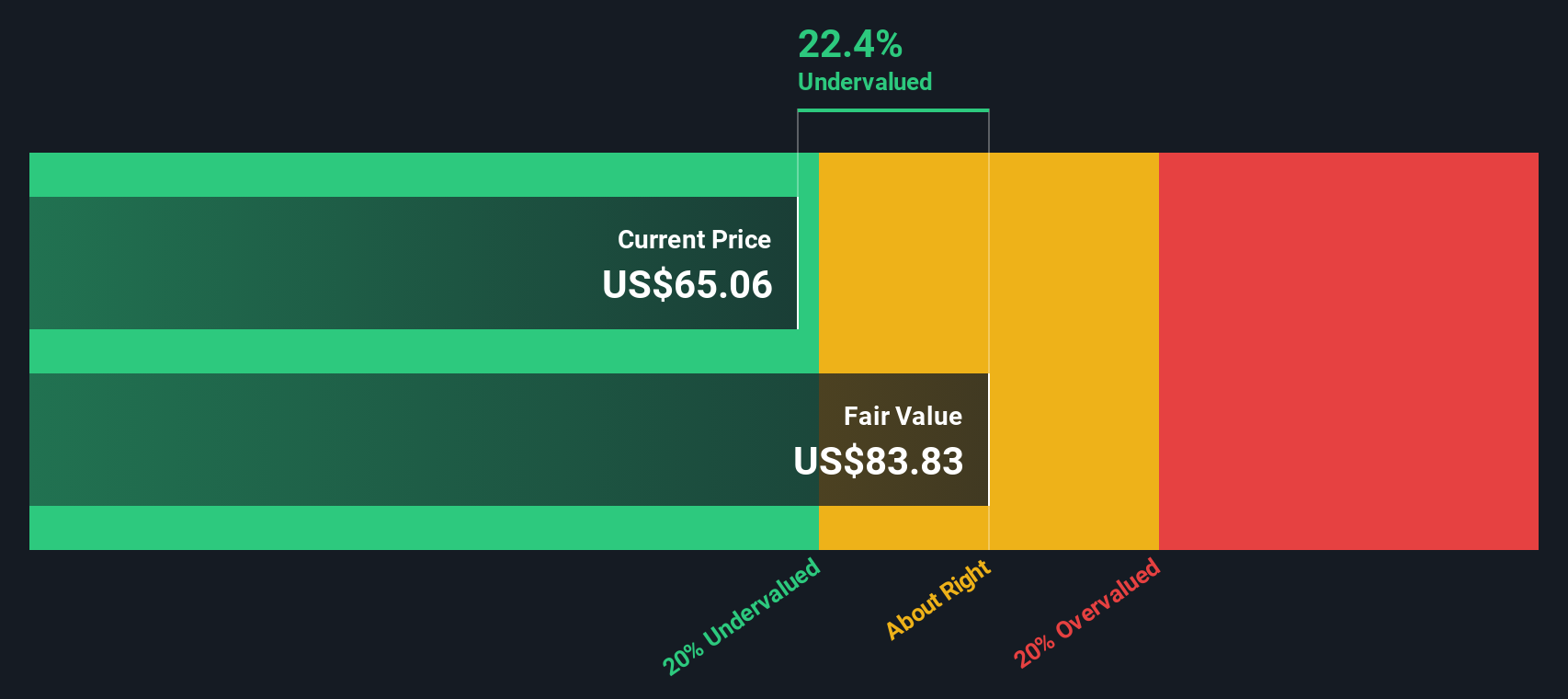

With NYT trading at $72.94, close to its analyst price target but at a reported intrinsic discount of about 34%, the key question is whether the market is already paying up for future growth or leaving a genuine buying window open.

Most Popular Narrative: 9.1% Overvalued

Against the latest close of $72.94, the most followed narrative points to a fair value of $66.88, so it frames NYT as pricing in a premium today.

Robust growth in digital subscriptions driven by an expanding portfolio of bundled offerings (news, Cooking, Games, The Athletic) and a focus on direct consumer relationships positions the company to capture more recurring revenue, strengthen ARPU, and reduce churn. This directly supports long term revenue and margin expansion.

Curious what sits behind that premium tag, and how much of it hangs on subscriber growth, bundle uptake, and richer margins over time? The full narrative lays out the numbers.

Result: Fair Value of $66.88 (OVERVALUED)

However, there is still the risk that traffic shifts from big tech platforms and rising content costs could challenge subscriber growth assumptions and squeeze future margins.

Another View: Cash Flows Point in the Opposite Direction

While the popular narrative flags NYT as about 9.1% overvalued at a fair value of $66.88, our DCF model points the other way. On this view, NYT at $72.94 trades roughly 33.9% below an estimated future cash flow value of $110.33. This paints a very different picture of upside and risk. Which story do you think fits your expectations better?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out New York Times for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own New York Times Narrative

If you look at this and think the story should read differently, you can test the numbers yourself and shape a fresh view in minutes, Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding New York Times.

Looking for more investment ideas?

If NYT has sharpened your thinking, do not stop here; the real edge comes from regularly sifting through fresh, high quality ideas before the crowd notices.

- Target resilient compounding potential by reviewing our 85 resilient stocks with low risk scores that could help steady your portfolio through different market conditions.

- Hunt for mispriced quality using the 53 high quality undervalued stocks that highlights companies with solid fundamentals trading below their estimated worth.

- Build a watchlist of under the radar potential by scanning the screener containing 23 high quality undiscovered gems where strong financial profiles have not yet attracted wide attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.