Assessing Norfolk Southern (NSC) Valuation After Recent Share Price Gains And Undervaluation Signals

Norfolk Southern Corporation NSC | 0.00 |

Why Norfolk Southern (NSC) is on investors’ radar

Norfolk Southern (NSC) continues to attract attention as investors weigh its recent share performance against the company’s latest reported fundamentals, including revenue of US$12,185 million and net income of US$2,667 million.

With the stock up about 3% over the past month and roughly 8% year to date, readers are asking how that trajectory lines up with its value score of 2 and its longer term total returns.

Short term, the share price has been relatively steady. The 1-day move is down 2.0%, the 7-day share price return is up 0.41% and the 30-day share price return is up 2.54%. Over a longer horizon, the 1-year total shareholder return of 32.67% and 3-year total shareholder return of 57.80% point to stronger momentum.

If you are thinking beyond a single rail operator, this is a good moment to see what else is moving in infrastructure and transit by checking out 34 power grid technology and infrastructure stocks

Norfolk Southern’s solid recent returns, combined with a value score of 2 and an intrinsic value estimate above the current US$311.84 share price, raise the key question: is there still a buying opportunity here, or has the market already priced in future growth?

Most Popular Narrative: 6.1% Undervalued

Norfolk Southern’s most followed narrative points to a fair value of $332.22, which sits above the recent $311.84 share price and frames the current upside debate.

The company's focus on increasing customer confidence through consistent service improvements is leading to meaningful market share gains, particularly in merchandise and intermodal segments, which could bolster future revenue growth.

Strategic plans to capitalize on industrial development activity, particularly in sectors like steel and food production, along with the potential for highway to rail conversions, are expected to provide new demand drivers for volume growth, supporting long term revenue enhancement.

Want to see what sits behind that growth story, and how it feeds into the valuation model, margin assumptions and the earnings multiple baked into the target?

Using an 8.51% discount rate, this narrative ties together projected revenue expansion, higher profit margins and a future P/E profile to land at a fair value of $332.22. With the share price at $311.84, the valuation case currently hinges on whether those cash flow and profitability assumptions hold over time and justify the implied premium over today’s level.

Result: Fair Value of $332.22 (UNDERVALUED)

However, that upside story still runs into real tests, from storm restoration costs that pressure margins to weaker export coal pricing that could weigh on revenue assumptions.

Another angle on valuation

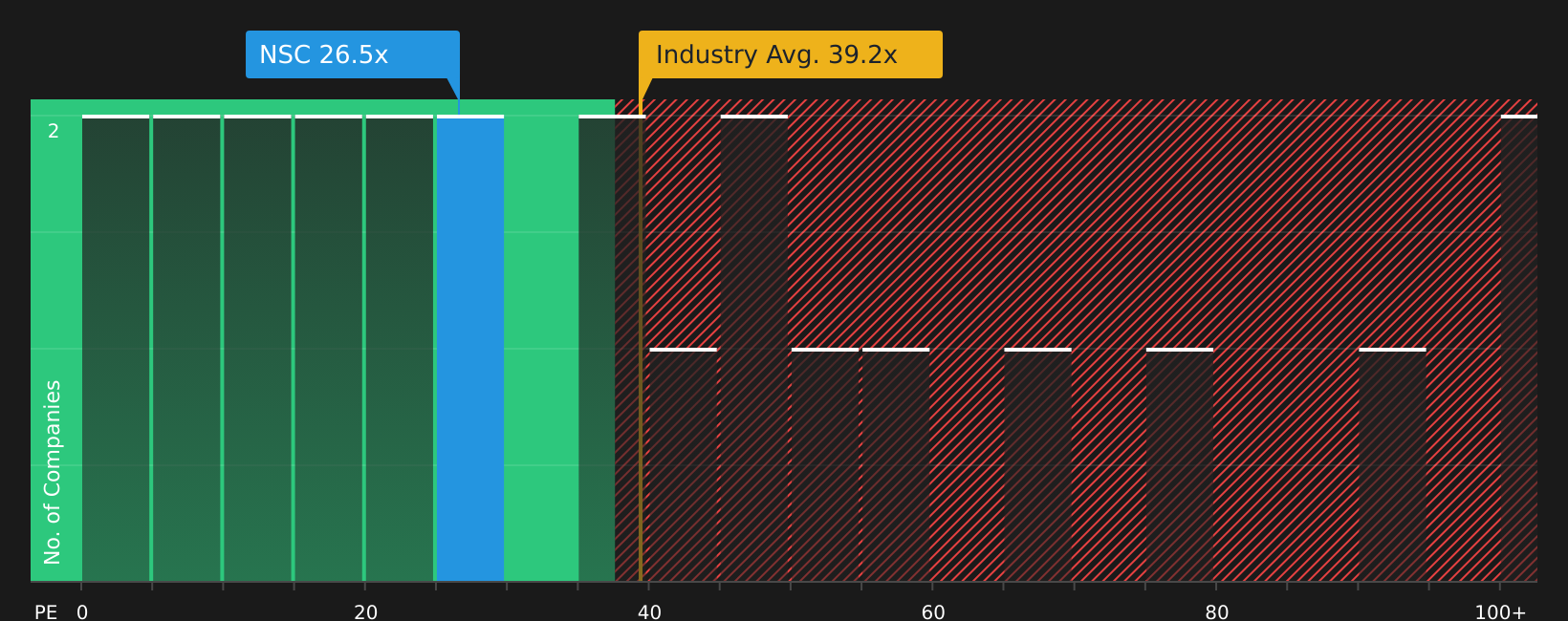

The analyst narrative points to fair value of $332.22 and frames Norfolk Southern as 6.1% undervalued, yet the stock trades on a P/E of 26.3x versus an estimated fair ratio of 23.3x. That richer multiple suggests less margin for error, so which signal do you trust more?

Next Steps

Mixed signals so far, right, with solid returns, a low value score and both risks and rewards on the table, so act now by checking the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop at just one stock today, you could miss out on other opportunities that better match your goals, time horizon and appetite for risk.

- Target potential mispricing by scanning for quality companies trading below their estimated worth with the 51 high quality undervalued stocks.

- Build a steadier income stream by reviewing stocks offering robust payouts through the 10 dividend fortresses.

- Focus on resilience by narrowing in on companies with strong financial foundations using the solid balance sheet and fundamentals stocks screener (46 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.