Assessing Nuvalent (NUVL) Valuation After NDA Milestones Guardant Alliance And Quarterly Loss

Nuvalent, Inc. Class A NUVL | 0.00 |

Nuvalent (NUVL) is in focus after a cluster of company updates, including first quarter earnings that showed a net loss of US$109.28 million and new detail on late stage oncology milestones.

At a share price of US$102.40, Nuvalent has seen mixed short term moves, with a 1 day share price return of 1.78% decline but a 1 year total shareholder return of 43.02%. This points to stronger momentum over a longer window as investors weigh the NDA progress, Guardant collaboration and quarterly loss against the potential of its oncology pipeline.

If you are looking beyond a single biotech story, this is a useful moment to scan other cancer focused AI opportunities via the 35 healthcare AI stocks

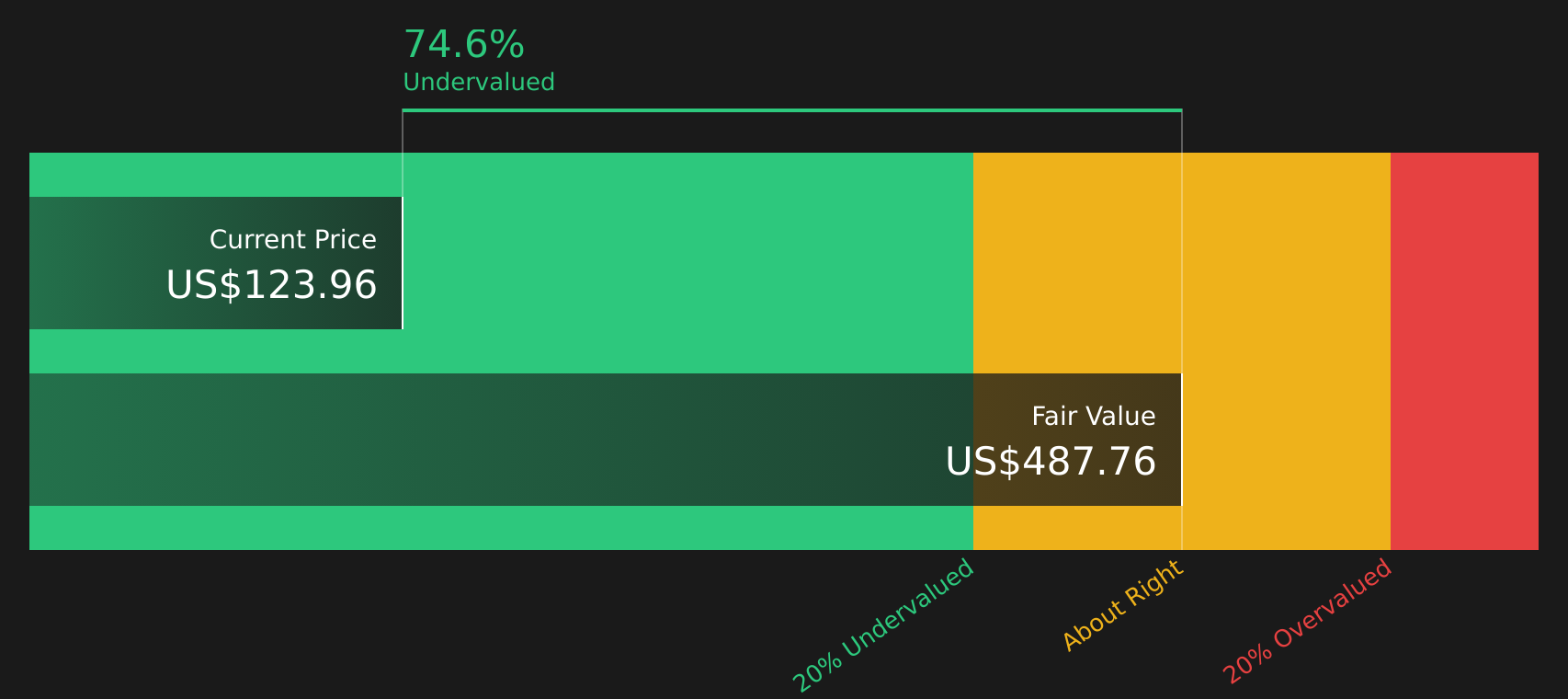

With Nuvalent still loss making, sitting at US$102.40 per share and trading at a sizeable discount to analyst targets and intrinsic estimates, you have to ask: is this a mispriced oncology pipeline, or is the market already banking on future growth?

Preferred Price-to-Book of 6.9x: Is it justified?

On one hand, Nuvalent trades at a P/B of 6.9x, which is inexpensive compared with its direct peers on this metric, but expensive against the broader US biotech industry.

The P/B ratio compares the company’s market value with its book value, which is essentially net assets on the balance sheet. For a clinical stage biotech with minimal revenue and ongoing losses, investors often focus on assets such as cash, intellectual property and the drug pipeline rather than current earnings.

Nuvalent is described as good value versus its peer group, where the average P/B sits at 46.1x, which is a very large premium to Nuvalent’s 6.9x. At the same time, the stock is flagged as expensive against the wider US biotech industry, where the average P/B is 2.5x, suggesting the market is assigning a richer valuation multiple than it does for the sector overall.

Result: Price-to-book of 6.9x (ABOUT RIGHT)

However, you still have to factor in clinical trial setbacks or funding pressures, which could quickly shift sentiment around a loss-making pipeline like this.

Another View: Our DCF Model Paints a Different Picture

The book value lens suggests Nuvalent sits somewhere in the middle, but the Simply Wall St DCF model tells a stronger story. With the stock at $102.40 and an estimated future cash flow value of $586.58, the model implies the shares are trading at a steep discount. Is the market being cautious, or are expectations simply too rich?

For a closer look at how that future cash flow estimate is built and what assumptions sit underneath it, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nuvalent for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals on value and growth potential can be unsettling. Move quickly, review the data for yourself and weigh up the stock’s risks and rewards using the 3 key rewards and 2 important warning signs.

Ready to uncover more investment ideas?

If you stop at a single stock, you risk missing other opportunities that better match your goals, risk appetite and preferred balance between income and growth.

- Target long term compounding potential by scanning 51 high quality undervalued stocks that combine solid fundamentals with room for market re rating.

- Strengthen your income stream by reviewing 12 dividend fortresses that focus on higher yields and robust payout profiles.

- Protect your downside by checking 71 resilient stocks with low risk scores designed to highlight companies with more resilient risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.