Assessing OGE Energy (OGE) Valuation After Recent Share Price Pullback And Mixed Fair Value Signals

OGE Energy Corp. OGE | 48.76 | +1.04% |

Recent performance snapshot

OGE Energy (OGE) has moved quietly on the screens recently, with the stock slipping about 1.1% over the past day and 2.2% over the past week, keeping interest on its underlying fundamentals.

Over the past month the share price has been broadly flat, while the past 3 months show an 8.2% decline. This backdrop may prompt you to compare recent returns with the company’s longer term profile.

Looking beyond the latest moves, OGE Energy’s 1 year total shareholder return of 2.7% and 5 year total shareholder return of 74.38% contrast with the weaker 90 day share price return of an 8.15% decline. This points to fading short term momentum after a strong longer run.

If OGE’s recent pullback has you reassessing your watchlist, this can be a good moment to broaden your search and check out fast growing stocks with high insider ownership.

With OGE Energy showing moderate 1 year gains, solid multi year total returns and a recent 8.2% 3 month pullback, investors may ask whether this is a quietly mispriced utility or if the market is already pricing in expectations for future growth.

Most Popular Narrative: 9.3% Undervalued

OGE Energy’s most followed narrative points to a fair value of $47.05 per share, compared with the latest close of $42.69, putting its assumptions in focus.

Ongoing and planned investments in generation capacity and transmission infrastructure, with legislative and regulatory support (e.g., CWIP and PISA mechanisms), enable accelerated asset deployment with minimized lag in rate recovery, supporting consistent future earnings and improved return on equity.

Curious what has to go right for that valuation to hold up? The narrative leans on steady load growth, firm margins, and a richer earnings multiple. The full set of assumptions is where the story really gets interesting.

Result: Fair Value of $47.05 (UNDERVALUED)

However, this hinges on industrial and oilfield demand not staying weak, and on large capital projects avoiding cost overruns or higher than expected financing costs.

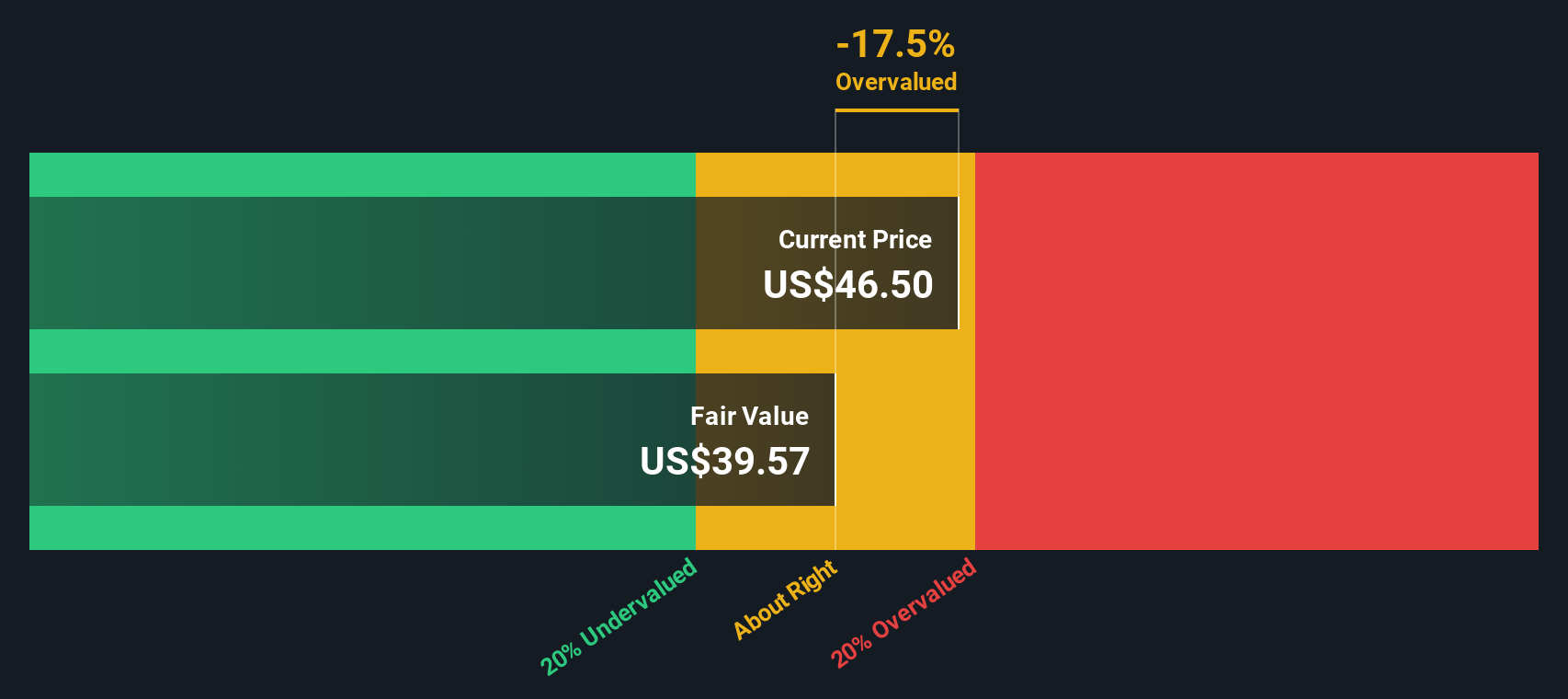

Another View: Cash Flows Point The Other Way

The narrative and analyst targets lean toward OGE Energy being undervalued, but our DCF model tells a different story. On that view, the current price of $42.69 sits above an estimate of future cash flow value of $38.15, which screens as overvalued instead.

For you, that kind of gap can feel less like a clear bargain and more like a trade off between paying up for a smoother utility earnings profile and insisting on a wider margin of safety. Which lens fits your own expectations for OGE’s long term cash generation?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out OGE Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 873 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own OGE Energy Narrative

If this story does not quite match your view and you would rather lean on your own research, you can quickly build a custom thesis with Do it your way.

A great starting point for your OGE Energy research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

You have done the work on OGE Energy, so do not stop there. Use the same focus to spot other opportunities before they slip past you.

- Scan for potential growth stories early by checking out these 3524 penny stocks with strong financials that already show stronger financial footing than many expect from smaller names.

- Target the intersection of healthcare and AI where new use cases are emerging, and let these 109 healthcare AI stocks surface companies already operating in this space.

- Hunt for potential mispricings by reviewing these 873 undervalued stocks based on cash flows that appear inexpensive relative to their projected cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.