Assessing Olaplex Holdings (OLPX) Valuation After A Year Of Mixed Returns And Earnings Pressure

Olaplex Holdings, Inc. OLPX | 0.00 |

Recent performance context for Olaplex Holdings (OLPX)

Without a specific news catalyst, Olaplex Holdings (OLPX) is drawing attention after a year of mixed signals, including a reported loss of US$15.004 million alongside a 1 year total return of 50.7%.

At a share price of US$2.05, Olaplex’s recent 90 day share price return of 15.2% and 1 year total shareholder return of 50.7% suggest momentum has been rebuilding after weaker 3 year total shareholder returns.

If you are comparing Olaplex’s recent recovery with other opportunities, this is a good moment to widen the search and check out 20 top founder-led companies

So with the stock trading around US$2.05, a reported US$15.004 million loss and an indicated 53.2% intrinsic discount, is this a genuine value opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 10.8% Overvalued

The most followed narrative puts Olaplex’s fair value at $1.85, which sits below the recent $2.05 close, framing the current price as ahead of that estimate.

Olaplex's accelerated new product development, launching three innovations including entry into the fast-growing scalp health segment, positions the company to increase repeat purchases, capture incremental market share, and support revenue growth and margin expansion through proprietary, science-backed offerings.

Curious what kind of revenue profile and margin rebuild have to line up for that fair value to hold? The narrative leans on specific growth assumptions and a richer future earnings multiple that sits above the broader Personal Products peer group. The tension between modest top line expectations and a premium valuation anchor is where the story really gets interesting.

Result: Fair Value of $1.85 (OVERVALUED)

However, there are still pressure points, including softer specialty retail sales and thinner EBITDA margins, that could quickly challenge the optimistic margin recovery narrative.

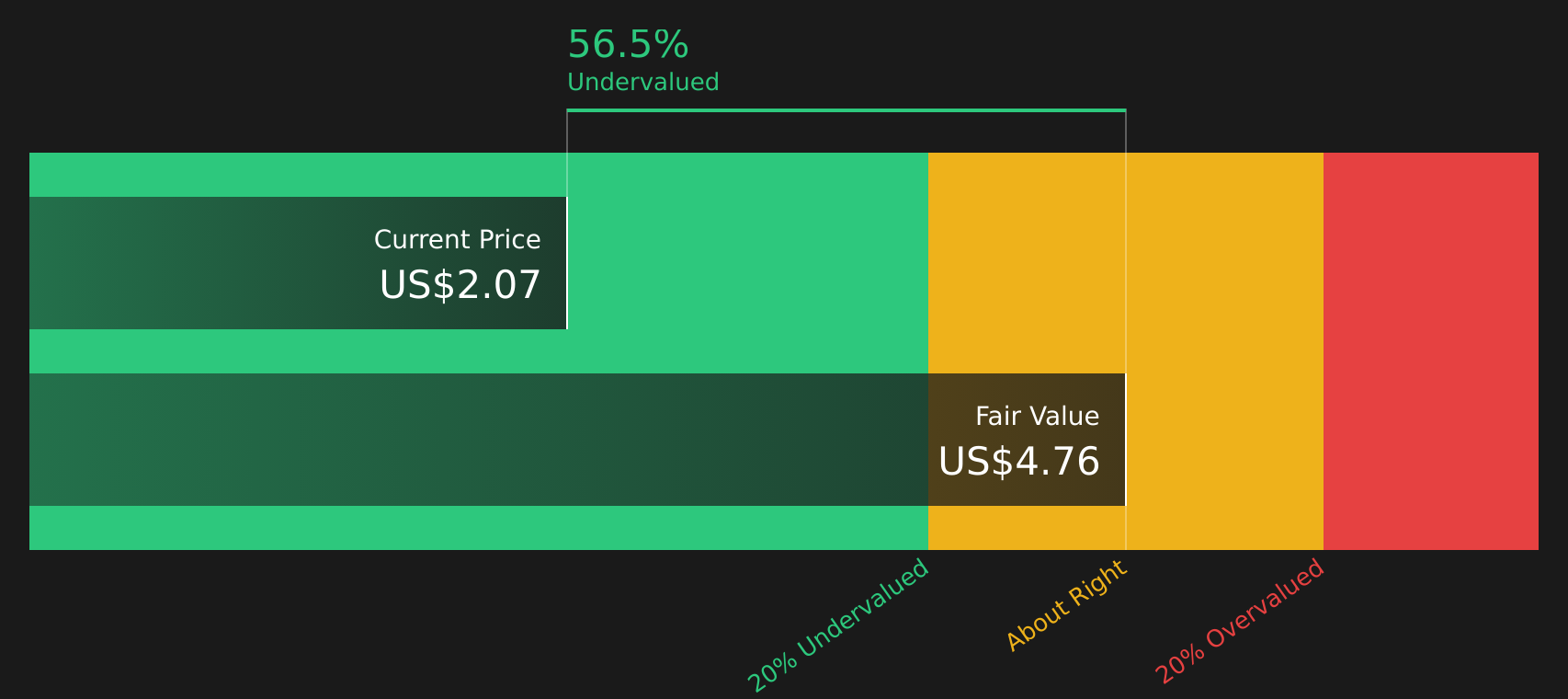

Another lens on value: cash flows vs market multiples

So far the focus has been on a fair value of $1.85 that frames Olaplex as 10.8% overvalued at $2.05. The SWS DCF model tells a different story, putting future cash flows at $4.38 per share, which implies the stock is trading at a steep discount. Which view do you think fits your expectations for the business?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Olaplex Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and sentiment, do you want to rely on headlines or get closer to the numbers yourself? Take a few minutes to weigh the potential upside and the areas of concern with 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you could miss other opportunities that fit your style, risk comfort and income needs, so widen the search with a few focused screens.

- Target potential mispricings by scanning a curated set of 46 high quality undervalued stocks that combine quality fundamentals with room for the market to reassess.

- Strengthen portfolio resilience by reviewing solid balance sheet and fundamentals stocks screener (47 results) that prioritise financial durability and healthier capital structures.

- Get ahead of the crowd by studying a screener containing 22 high quality undiscovered gems before they appear on more radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.