Assessing OneMain Holdings (OMF) Valuation After Expanded TPG Loan Sales And JPMorgan Downgrade

OneMain Holdings, Inc. OMF | 54.07 | +0.09% |

Recent news around OneMain Holdings (OMF) is pulling investors in two directions, with an expanded loan sale agreement to TPG Inc. on one side and a JPMorgan downgrade on the other.

Those mixed headlines have come after a softer patch for the stock, with a 6.5% 30 day share price return decline and a 6.7% year to date share price return decline, even as the 1 year total shareholder return sits at 20.7% and the 5 year total shareholder return at 132.9%. This signals that longer term holders have experienced much stronger momentum than recent traders.

If this kind of credit story has your attention, it could be a good moment to widen the lens and check out fast growing stocks with high insider ownership as you look for other interesting ideas.

So with JPMorgan turning cautious, a larger loan sale pipeline to TPG in place, and the shares trading below the average analyst price target, is OneMain now trading at a discount, or is the market already pricing in future growth?

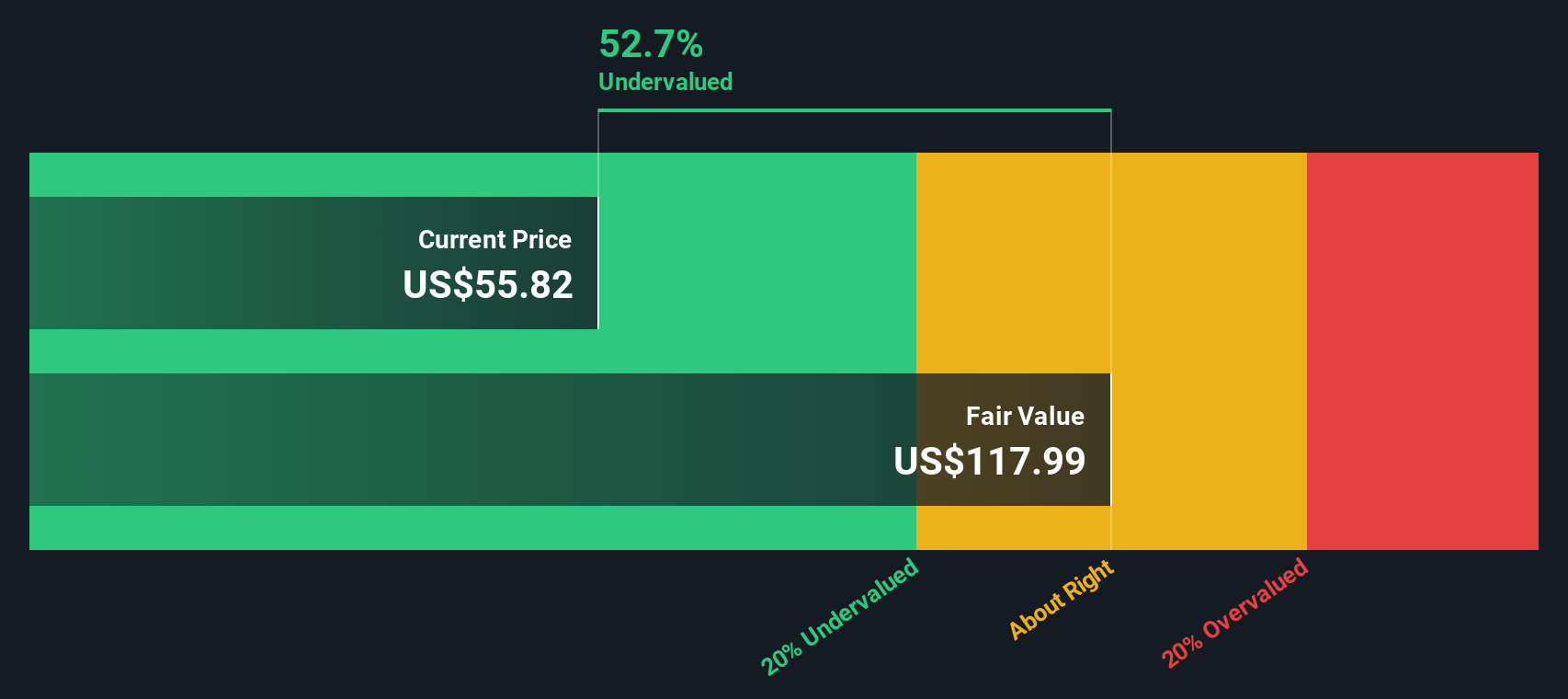

Most Popular Narrative: 12.3% Undervalued

The most followed narrative sees OneMain Holdings’ fair value at $73.47 versus a last close of $64.46, framing the current debate around upside versus risk.

Continued growth in consumer borrowing, particularly among non-prime consumers facing higher costs and stagnant real wages, supports long-term loan demand; OneMain's high-quality origination growth and expansion into debt consolidation and auto finance are positioned to capture this, driving sustained revenue and receivables growth.

Curious what drives that fair value gap? The narrative focuses on fast growing revenue, thicker lending margins, and a future earnings multiple that is very different from where the stock trades today. Want to see which numbers really move the model and how they fit together across growth, profitability and valuation? Read on and test whether those assumptions line up with your own view.

Result: Fair Value of $73.47 (UNDERVALUED)

However, that upside view still leans on tight credit discipline and steady funding, and both could be tested if nonprime borrowers or capital markets hit a rough patch.

Another Angle: DCF Points The Other Way

There is a catch. While the narrative model suggests OneMain is 12.3% undervalued, the SWS DCF model, based on future cash flows, comes in lower than today’s share price at $60.88 versus $64.46, which implies the stock looks slightly overvalued on that view. Which lens fits your expectations for cash generation best?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out OneMain Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 862 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own OneMain Holdings Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to weigh the data yourself, you can build a bespoke view in just a few minutes with Do it your way.

A great starting point for your OneMain Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one company, you might miss opportunities that match your style better, so cast the net wider and stress test your thinking across other ideas.

- Spot potential value plays early by scanning these 862 undervalued stocks based on cash flows that line up strong cash flow expectations with prices that may not fully reflect them yet.

- Ride major technology shifts by checking out these 24 AI penny stocks that are tied to real-world AI products, services, and supporting infrastructure.

- Tap into digital asset themes without holding tokens directly by reviewing these 18 cryptocurrency and blockchain stocks tied to exchanges, payment rails, and blockchain infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.