Assessing Ouster (OUST) Valuation After Rev8 OS Lidar Launch And NVIDIA Platform Qualification

Ouster, Inc. OUST | 0.00 |

Ouster (OUST) recently launched its Rev8 OS digital lidar family and secured qualification for NVIDIA’s DRIVE Hyperion and Jetson platforms, putting the company’s native color sensors and software stack directly in front of level 4 autonomy developers.

Alongside the Rev8 launch and multiple NVIDIA integrations, Ouster’s at-the-market follow on equity offering and recent quarterly update have all arrived during a period of strong share price momentum, with a 30-day share price return of 30.98% and a 1-year total shareholder return of 137.51% pointing to growing investor interest despite earlier years of weaker performance.

If you are watching how lidar and Physical AI are reshaping markets, it can be useful to compare Ouster with other opportunities in related areas using 38 AI infrastructure stocks

After a rapid share price move, double digit recent revenue growth, and a market cap of about US$1.71b, the key question is whether Ouster’s current valuation still leaves room for upside or if markets are already pricing in future growth.

Most Popular Narrative: 31.7% Undervalued

Ouster's most followed valuation narrative pegs fair value at about $39.67 per share, compared with the last close of $27.10. This puts a spotlight on its growth story and future earnings profile at this price level.

Ouster is tapping into the massive Intelligent Transportation Systems (ITS) market with their Blue City traffic management solution, which could drive significant revenue growth as they expand deployments across the US, Europe, and Asia. This is expected to positively impact revenue.

Want to see what kind of revenue trajectory and margin shift would justify this valuation gap? The narrative leans on rapid top line expansion, a turn toward profitability, and a premium future earnings multiple that is far from typical. Curious which assumptions matter most and how they feed into that fair value path?

Result: Fair Value of $39.67 (UNDERVALUED)

However, this hinges on Ouster holding its ground against strong lidar competitors while keeping legal, R&D, and other operating costs from squeezing already thin margins.

Another View: Valuation Looks Rich On Sales

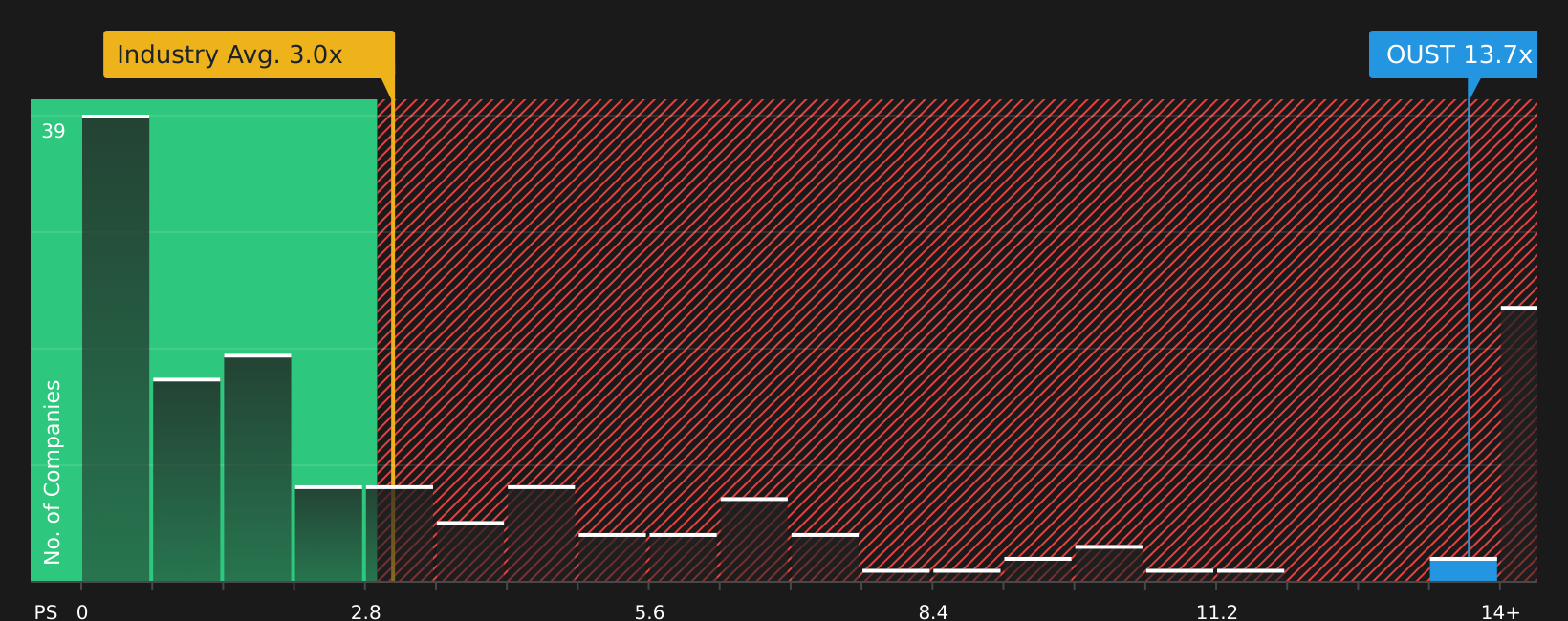

Analysts and the SWS model see Ouster as trading about 41.9% below a fair value of $46.66, but the P/S ratio tells a tougher story. At 9.3x sales, the stock is priced well above the US Electronic industry at 2.7x, the peer average at 4.9x, and even the fair ratio of 7x, which points to elevated valuation risk if growth or sentiment cool.

Next Steps

Given the mix of enthusiasm and concern in this story, it makes sense to review the underlying data yourself and decide quickly where you stand based on the 4 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Ouster has caught your attention, do not stop here. Broaden your watchlist with a few targeted stock ideas that could sharpen your overall strategy.

- Target potential mispricings by scanning 44 high quality undervalued stocks, and see which stocks currently trade below their estimated worth.

- Strengthen your income toolkit by reviewing 13 dividend fortresses, focusing on companies that combine yield with staying power.

- Cut down portfolio stress by checking 69 resilient stocks with low risk scores, highlighting stocks with lower risk scores that may help smooth returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.