Assessing Paychex (PAYX) Valuation After Prolonged Underperformance And Slowing Growth Concerns

Paychex, Inc. PAYX | 0.00 |

Why Paychex’s recent underperformance is back in focus

Paychex (PAYX) is back on investor watchlists after recent analysis flagged its weaker share performance versus the broader market, alongside concerns about slowing long term revenue growth and pressure on operating margins.

At the same time, Paychex has grown into a broad human capital management and HR outsourcing provider. The company serves roughly 800,000 clients with high retention, which gives investors concrete data points to weigh against these profitability and growth concerns.

After a weak patch that left long term shareholders with a 1 year total shareholder return decline of 34.49%, recent momentum has improved. A 1 month share price return of 10.01% has taken the stock to US$100.53 and tempered concerns about softening revenue growth and margins.

If Paychex’s recent move has you reassessing where growth and resilience might come from next, it can be useful to widen the lens and look at 21 top founder-led companies

With Paychex trading near US$100.53, modestly below one independent intrinsic value estimate and close to analyst targets, the key question now is whether recent weakness leaves genuine upside on the table or if the market already reflects future growth.

Most Popular Narrative: 40% Undervalued

At a last close of $100.53 versus a widely followed fair value narrative of about $100.93, the current price sits just under that anchor and keeps attention on whether the long term story is fully priced in.

The pending acquisition of Paycor is expected to strengthen Paychex's competitive position by expanding its customer base and offering a more comprehensive HCM portfolio, which could drive revenue growth through cross-selling opportunities.

For readers interested in what kind of revenue path and margin profile would need to occur to support this view, or how far profit expectations extend across the forecast horizon, the full narrative presents the numbers behind that story.

Result: Fair Value of $100.93 (UNDERVALUED)

However, the picture is not one sided. Paycor integration risk and choppy payroll and HR spending could potentially undermine the fair value narrative if they become more significant factors.

Another View on Paychex’s Valuation

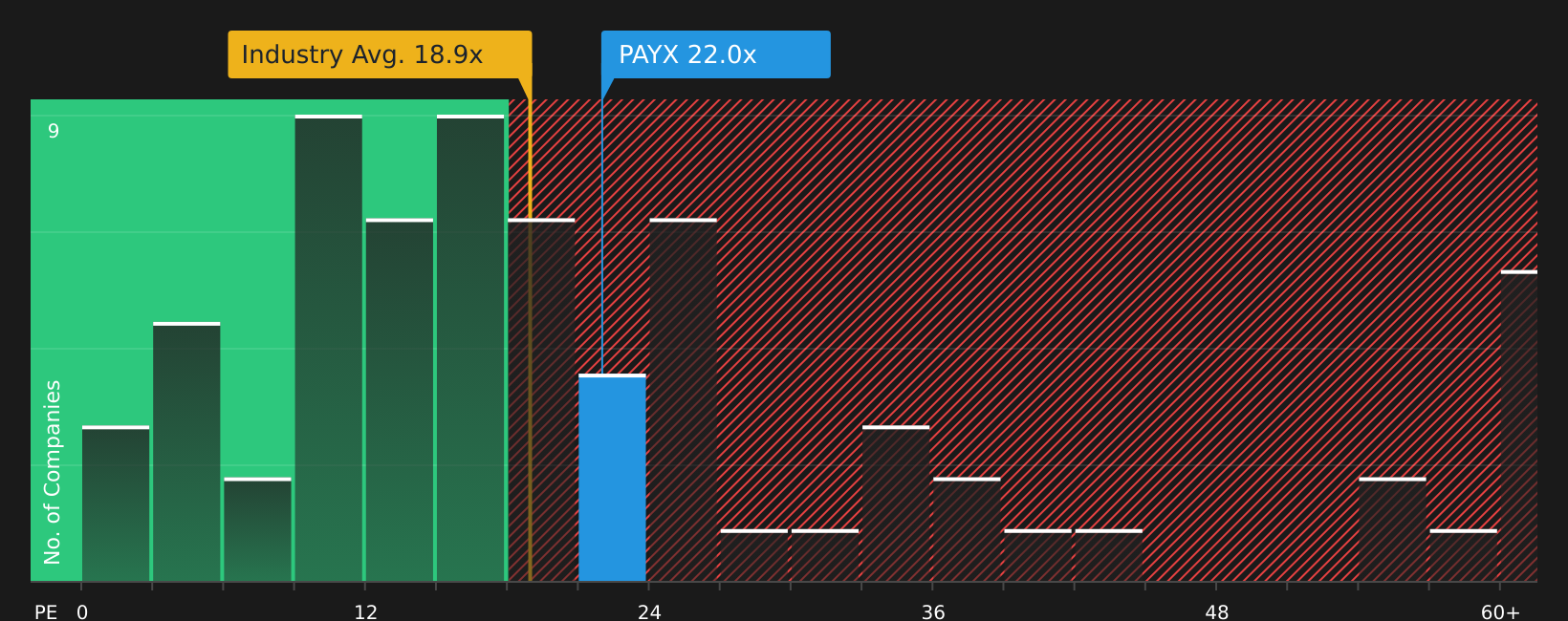

While the fair value narrative sits near $100.93, the market is paying about 22x earnings for Paychex compared with 17.8x for peers and 19.7x for the wider US Professional Services industry. That richer P/E points to higher valuation risk, so the key question is what justifies paying up.

Next Steps

With mixed signals around value, risk and reward, the next move really sits with you. Look through the details, stress test the assumptions and weigh the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Paychex has sharpened your focus, do not stop here. Fresh opportunities often sit just outside your current watchlist, waiting for a closer look.

- Target dependable cash generators by reviewing companies in the 49 high quality undervalued stocks that combine pricing below intrinsic estimates with solid fundamentals.

- Strengthen your income stream by scanning the 9 dividend fortresses for stocks with yields that stand out and payouts that matter.

- Prioritise resilience by checking the 64 resilient stocks with low risk scores to see stocks assessed with lower risk scores that may help balance a concentrated portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.