Assessing Peoples Bancorp (PEBO) Valuation After Dividend Strength And Banking Sector Stabilization

Peoples Bancorp Inc. PEBO | 0.00 |

Peoples Bancorp (PEBO) has drawn fresh attention after its share price moved above its long term average. This coincides with steadier banking sector conditions and renewed focus on the stock’s dividend and earnings outlook.

The latest move above its long term average comes on top of a 9.19% 1 month share price return and a 12.49% 3 month share price return. The 1 year total shareholder return of 35.73% and 3 year total shareholder return of 60.23% point to momentum that investors are reassessing against current earnings expectations and dividend income.

If this kind of momentum has you looking at banks and beyond, it could be a good time to broaden your search with the 19 top founder-led companies

With a 4.84% dividend yield, recent share price strength and an intrinsic value estimate that sits below the current market price, is Peoples Bancorp still undervalued or is the market already pricing in future growth?

Price-to-Earnings of 11.6x: Is it justified?

On a P/E of 11.6x, Peoples Bancorp sits at a level that lines up closely with the broader US Banks industry and below its peer group average.

The P/E ratio compares the company’s current share price to its earnings per share, so it gives you a quick read on how the market is valuing each dollar of profit. For a bank like Peoples Bancorp, which the data shows has high quality earnings and a record of profit growth over the past 5 years, P/E is a commonly watched yardstick.

Here, the picture is mixed. The stock is described as good value versus both peers and the wider US Banks industry on P/E, yet it screens as slightly expensive relative to an estimated fair P/E of 10.8x that our fair ratio work points to as a level the market could move towards. At the same time, earnings are forecast to grow, but not significantly, which can help explain why the market is not assigning a much higher multiple.

Compared with the peer average P/E of 14.8x and the US Banks industry average of 11.9x, Peoples Bancorp trades at a discount to similar companies and only slightly below the sector bar. This suggests the market is applying some restraint despite the longer term earnings growth record and the view that the shares are trading below an estimate of future cash flow value.

Result: Price-to-Earnings of 11.6x (ABOUT RIGHT)

However, investors still need to weigh banking sector credit quality risks and the possibility that earnings expectations may reset, which could challenge the recent valuation support.

Another View: Cash Flow Tells a Different Story

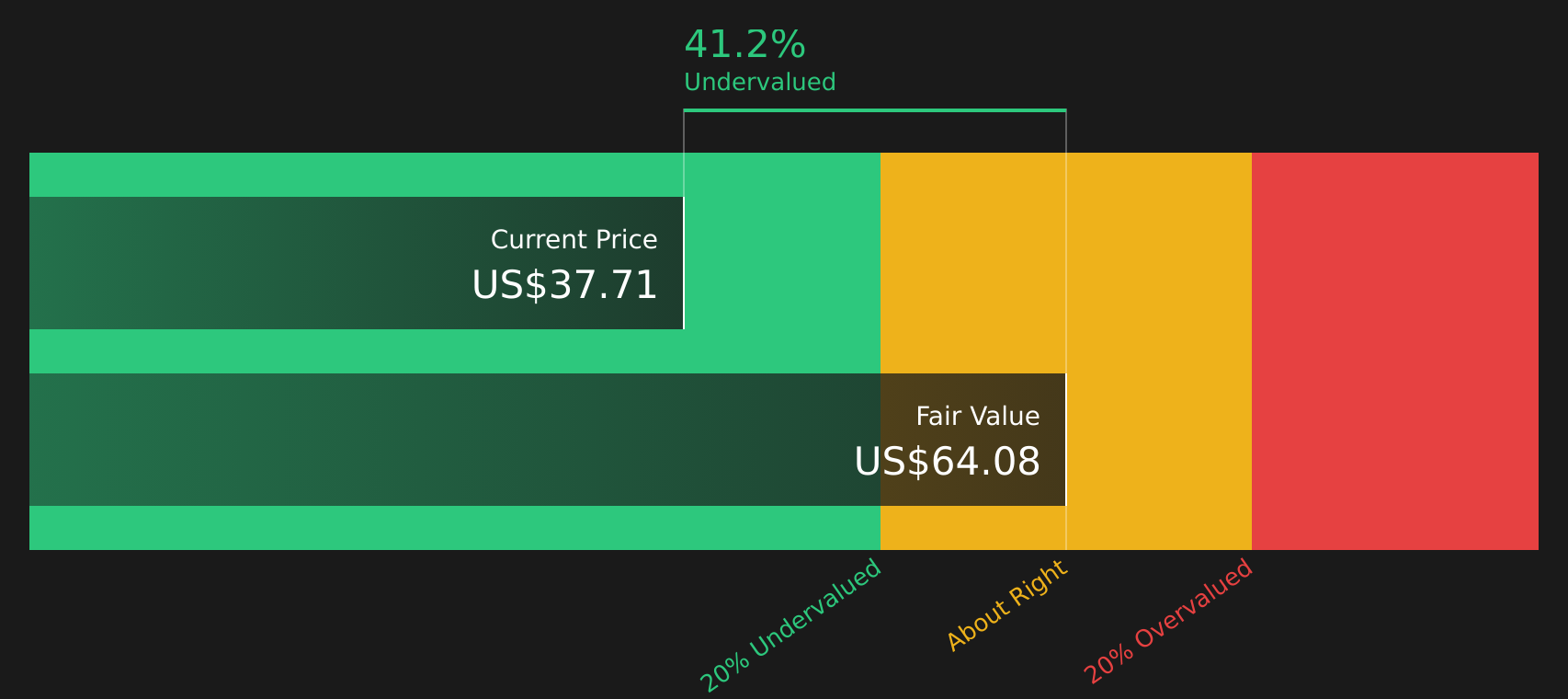

While the P/E of 11.6x suggests Peoples Bancorp is roughly in line with banks as a group, the SWS DCF model offers a sharper contrast. On that basis, the shares trade at $34.68 versus an estimated future cash flow value of $59.68, which indicates a valuation gap investors may wish to consider.

That kind of difference between earnings based pricing and a cash flow driven estimate raises a simple question: is the market being cautious for a specific reason, or is sentiment lagging the fundamentals?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Peoples Bancorp for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 62 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of strong recent returns and questions around valuation and risks can feel finely balanced, so it makes sense to look through the data yourself and move quickly to form your own view with the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Peoples Bancorp has you thinking about what else might be out there, do not stop here, use the screening tools to uncover ideas that fit your style.

- Target steady cash generators by scanning for companies in the solid balance sheet and fundamentals stocks screener (40 results) that can help anchor a diversified portfolio.

- Hunt for potential mispricings by reviewing the screener containing 24 high quality undiscovered gems that may not yet be widely followed.

- Prioritise resilience by focusing on the 73 resilient stocks with low risk scores and see which names stand out for lower risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.