Assessing Pool Corp (POOL) Valuation After Prolonged Share Weakness And Perceived Undervaluation

Pool Corporation POOL | 0.00 |

Recent share performance and business scale

Pool (POOL) has drawn fresh investor attention after a stretch of weaker share performance, with the stock showing declines over the past day, week, month, past 3 months, year to date, and the past year.

At a last close of US$187.77 and a market value of about US$6.8b, Pool operates as a large distributor of swimming pool supplies, equipment, and related outdoor living products. The company generated US$5,355.884m in revenue and US$404.067m in net income.

For Pool, the pressure has been building rather than easing, with the share price seeing a 12.63% decline over the past month and the 1 year total shareholder return down 36.63%. This points to fading momentum and a more cautious market view on its earnings power and risk profile.

If Pool's pullback has you rethinking where growth might come from next, this could be a good moment to scan for other opportunities via our screener of 18 top founder-led companies

With the stock down sharply over 1, 3 and 5 years, yet trading at what appears to be a sizable discount to analyst targets and intrinsic estimates, are you looking at a potential opportunity or at a market that is already pricing in future growth?

Most Popular Narrative: 29.5% Undervalued

Pool's most followed narrative points to a fair value of about $266 versus the last close at $187.77, centering the debate on whether recurring pool maintenance demand can support that gap.

The aging installed U.S. pool base continues to create steady, nondiscretionary demand for renovation, maintenance, and parts, partially insulating revenues from new build cyclicality and underpinning durable long-term earnings growth.

Curious how a maintenance heavy business, modest revenue growth assumptions and a premium future earnings multiple combine to support that fair value estimate? The tension between slower projected growth and a higher implied P/E sits at the core of this narrative, along with assumptions about margins, share count and discount rate that you might want to test against your own expectations.

Result: Fair Value of $266 (UNDERVALUED)

However, you also need to weigh risks such as persistent housing and construction softness, as well as rising costs that Pool may not fully pass through to customers.

Another way to look at Pool’s valuation

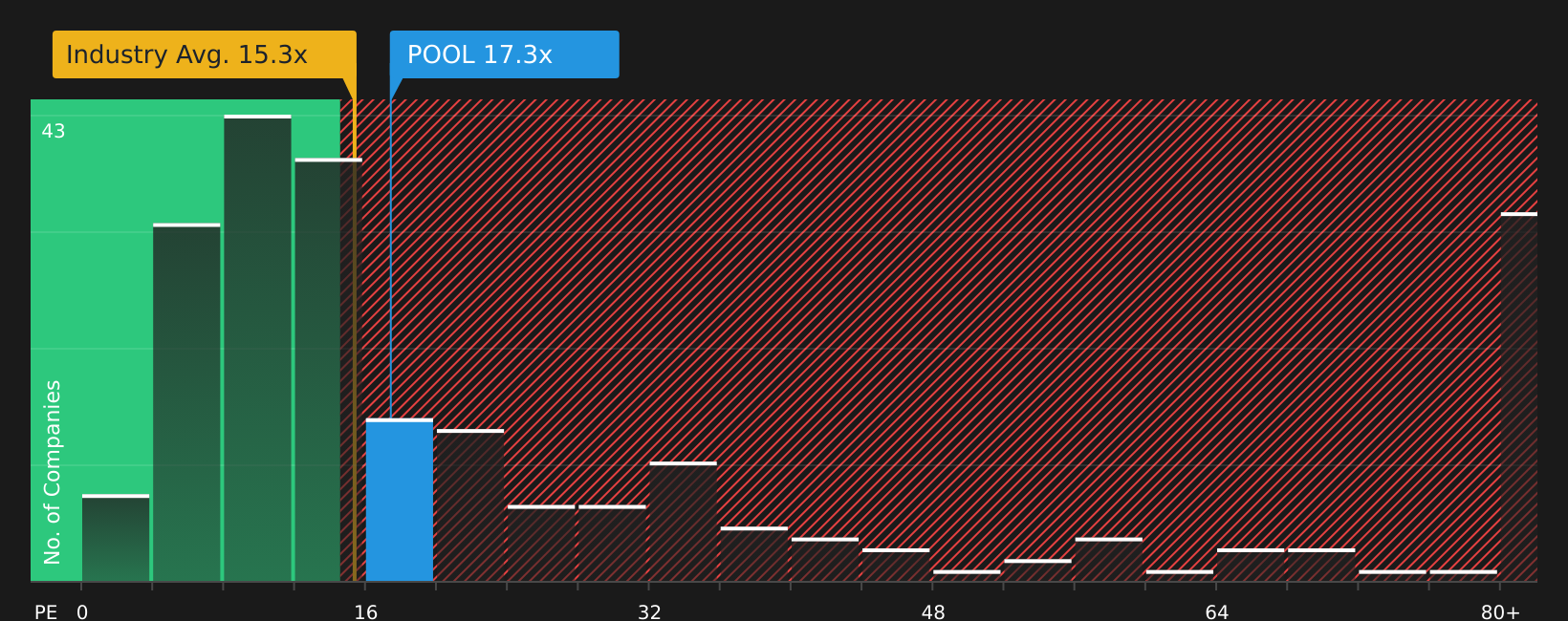

The fair value story so far leans on earnings forecasts and price targets, but the current P/E of 16.9x paints a tougher picture. That is higher than the global Retail Distributors average of 16.3x, above the peer average of 14.2x, and above a fair ratio of 15.1x. This suggests there may be less room for error if growth or margins disappoint.

When a stock trades above both its peers and a fair ratio that the market could move towards, it raises a simple question for you: is this a quality premium that still feels comfortable, or a valuation gap that could close the wrong way if sentiment turns?

Next Steps

Seeing mixed signals on quality and valuation so far? Take a closer look now, consider both the concern and the optimism, and ground your view in 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Pool has you reassessing where to put your capital next, do not stop here. Use focused screeners to spot stocks that better fit your goals today.

- Target resilient high yield opportunities by reviewing companies in the 12 dividend fortresses.

- Hunt for quality at a potential discount with stocks highlighted in the 51 high quality undervalued stocks.

- Prioritize capital preservation by scanning companies in the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.