Assessing Primo Brands (PRMB) Valuation After A Tough Year And Recent Share Price Rebound

Primo Brands Corporation Class A PRMB | 18.72 | -0.79% |

Primo Brands (PRMB) has caught investor attention after recent trading, with the share price at $17.99 and mixed total returns, including about 11% over the past week and a roughly 41% decline over the past year.

The recent 11.1% 7-day share price return comes after a difficult period, with the 1-year total shareholder return down about 40.6% and momentum still rebuilding from that weaker longer-term performance.

If Primo Brands has you reassessing your watchlist, it could be a good moment to broaden your search and check out healthcare stocks as another area to research.

With the share price at $17.99, a roughly 41% 1 year total return decline and a value score of 5, the key question now is whether Primo Brands is trading below its worth or if the market is already pricing in future growth potential.

Price to Sales of 1x: Is It Justified?

On a P/S of 1x, Primo Brands looks cheap compared with peers and the wider US beverage sector, even after the share price weakness down to $17.99.

The P/S ratio compares the company’s market value with its revenue, which can be useful for a business that is currently loss making but still generating sales.

For Primo Brands, the P/S of 1x sits well below the peer average of 4x and the US beverage industry average of 1.9x. This suggests the market is assigning a lower value to each dollar of sales. The estimated fair P/S of 1.1x also sits above the current level, indicating a gap that could close if sentiment and fundamentals align.

Result: Price-to-Sales of 1x (UNDERVALUED)

However, the current loss of $48.2 and the 40.6% 1 year total return decline mean profitability and sentiment shifts could quickly change how that low P/S is viewed.

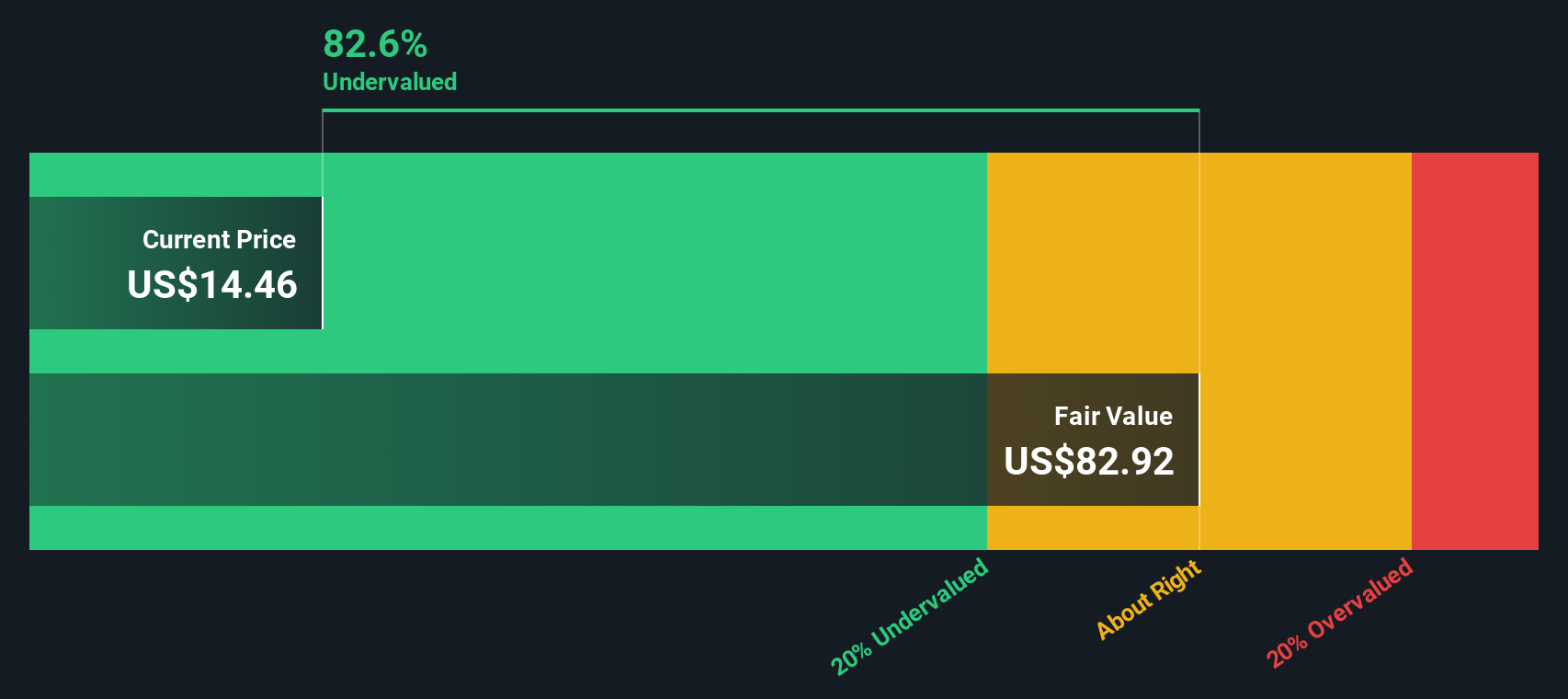

Another View: What Our DCF Model Suggests

If you look at Primo Brands through our DCF model instead of sales, the picture is very different. At a share price of $17.99, the stock is trading about 72.9% below our fair value estimate of $66.28, which points to a very steep implied discount.

That gap is far wider than what the P/S of 1x versus a fair ratio of 1.1x might suggest. This raises a tough question: is the DCF being too generous, or is the market being too harsh on a loss-making business that is expected to become profitable within three years?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Primo Brands for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 882 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Primo Brands Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a custom view of Primo Brands in minutes with Do it your way.

A great starting point for your Primo Brands research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Primo Brands has sharpened your focus on pricing and risk, do not stop here. Widening your search now could surface opportunities you would otherwise miss.

- Hunt for potential value plays that the market may be overlooking by screening for these 882 undervalued stocks based on cash flows with solid underlying cash flows.

- Ride the wave of artificial intelligence by scanning these 28 AI penny stocks that are tied to real business models, not just headlines.

- Target income-focused ideas by reviewing these 12 dividend stocks with yields > 3% that offer yields above 3% while you assess their long term sustainability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.