Assessing Simpson Manufacturing (SSD) Valuation After Earnings Beat And Improved Analyst Sentiment

Simpson Manufacturing Co., Inc. SSD | 0.00 |

Why the latest earnings and buyback matter for Simpson Manufacturing (SSD)

Simpson Manufacturing (SSD) is back in focus after first quarter earnings topped analyst expectations, with higher sales, stronger profit metrics, and fresh details on a recently completed share repurchase program.

The earnings beat and completed buyback appear to have supported sentiment, with a 15.48% 1 month share price return and a 16.59% year to date share price return contributing to a 25.05% 1 year total shareholder return.

If strong construction demand has caught your attention, it may be worth seeing what else is moving and checking out 35 power grid technology and infrastructure stocks

With earnings ahead of expectations, an active buyback, and mixed analyst views but a double digit implied upside to average targets, the key question now is simple: is Simpson Manufacturing undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 8.6% Undervalued

With Simpson Manufacturing last closing at $192.05 and the most followed fair value estimate at $210.20, the current price sits below that narrative view of worth.

The analysts have a consensus price target of $210.2 for Simpson Manufacturing based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.6 billion, earnings will come to $428.0 million, and it would be trading on a PE ratio of 25.2x, assuming you use a discount rate of 8.5%.

Curious what sits behind that higher fair value tag? The narrative leans heavily on steadier revenue growth, thicker margins, and a richer future earnings multiple. The exact mix of these levers is where the story really gets interesting.

Result: Fair Value of $210.20 (UNDERVALUED)

However, there are still pressure points to watch, including exposure to housing cycles and the risk that higher input costs squeeze margins if pricing power weakens.

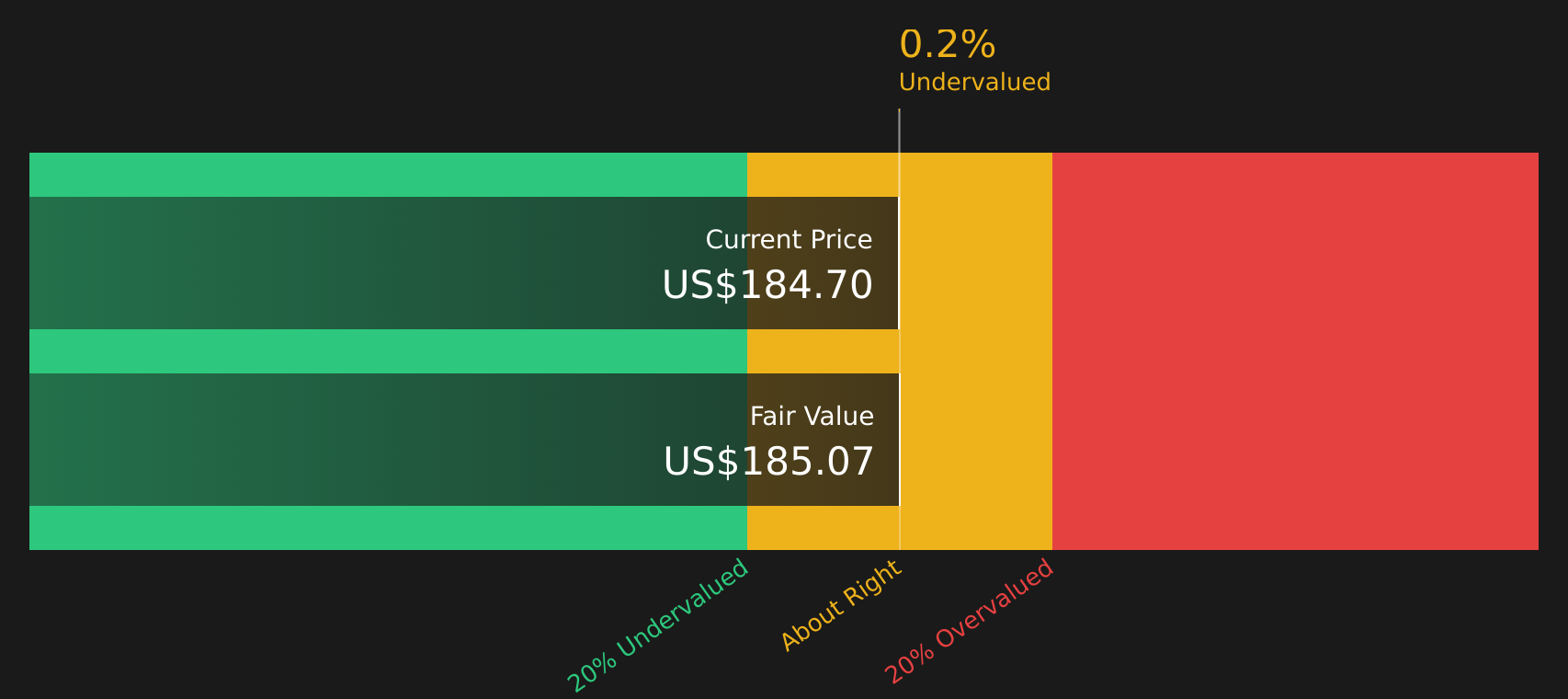

Another View: Cash Flows Point To A Tighter Picture

While the popular narrative frames Simpson Manufacturing as about 8.6% undervalued at $210.20, the SWS DCF model tells a different story. On that cash flow view, SSD at $192.05 sits above an estimate of $183.33, which implies a margin of safety that is already quite thin. So which signal should carry more weight for you: earnings multiples or cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Simpson Manufacturing for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals so far, it makes sense to look through the underlying data yourself and decide whether the optimism holds up. To see what investors are focusing on, review the 2 key rewards.

Looking for more investment ideas?

If Simpson Manufacturing has sharpened your focus, do not stop here. Put that momentum to work by lining up a few more opportunities that fit your style.

- Target potential mispricings in solid businesses by scanning 51 high quality undervalued stocks that pair quality fundamentals with attractive entry points.

- Strengthen your income stream by reviewing 13 dividend fortresses offering higher yields with an emphasis on durability.

- Prioritize resilience over drama by checking 71 resilient stocks with low risk scores that score well on balance sheet strength and risk metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.