Assessing TechnipFMC (FTI) Valuation After Strong Multi Year Returns And Conflicting Fair Value Signals

TechnipFMC plc FTI | 0.00 |

TechnipFMC stock performance snapshot

TechnipFMC (NYSE:FTI) has drawn attention after a mixed recent trading stretch, with the stock down roughly 1% over the past month and up about 12% over the past 3 months.

For investors tracking longer horizons, TechnipFMC shows a year to date gain of about 51% and a 1 year total return of roughly 143%. These returns are supported by annual revenue of US$10.19b and net income of US$1.08b.

Recent trading has cooled slightly, with the share price down over the past week and month but still supported by a strong 3 month share price return and very large 5 year total shareholder return. This suggests momentum has been building over the longer term.

If TechnipFMC has you looking across the energy value chain, it could be a good moment to widen your research using our nuclear energy infrastructure stocks screener, starting with 88 nuclear energy infrastructure stocks.

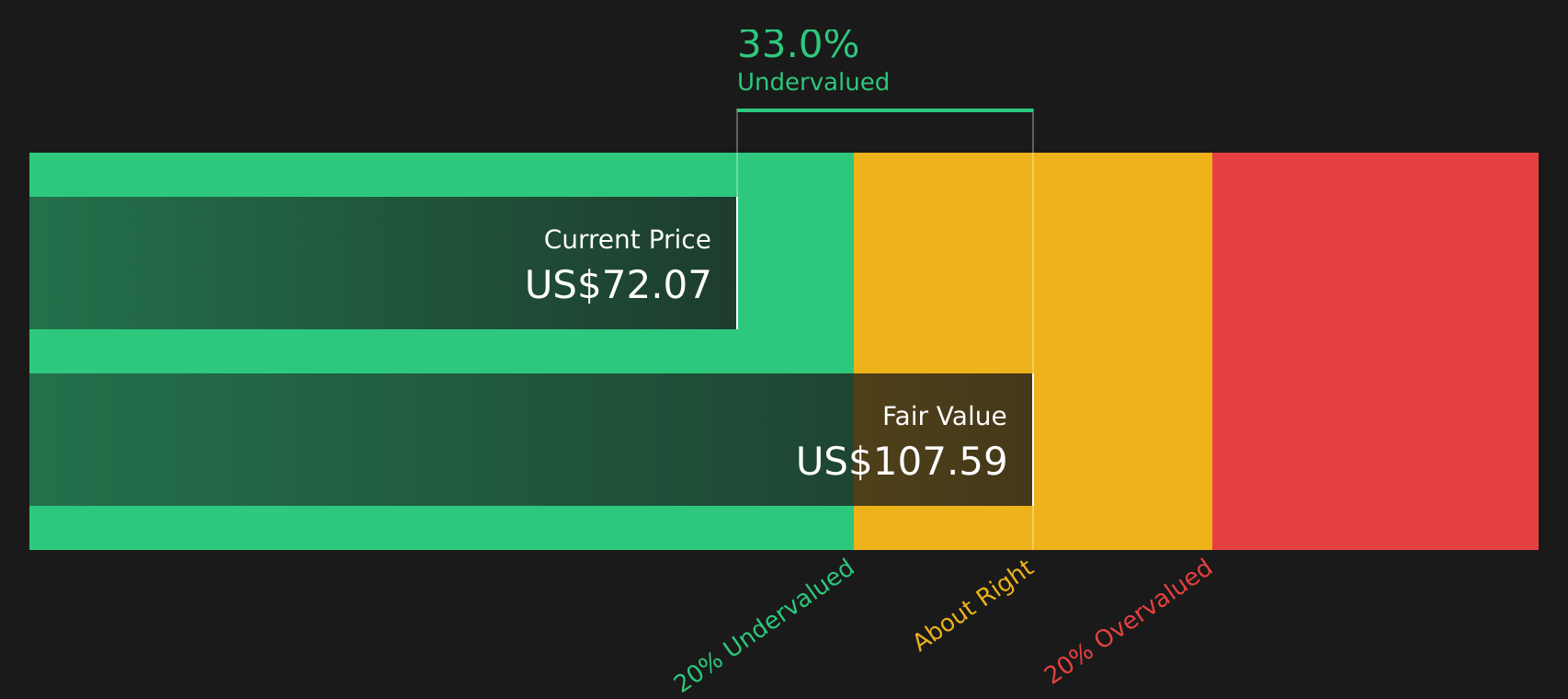

After such strong multi year returns and with the stock trading close to analyst targets, yet at an indicated 23% discount to intrinsic value, is TechnipFMC still mispriced or is the market already baking in future growth?

Most Popular Narrative: 9% Overvalued

The most followed narrative puts TechnipFMC's fair value at $65.62, below the last close of $71.41, framing the current share price as above that estimate.

Robust and growing pipeline of offshore oil & gas and deepwater projects globally, driven by increased capital allocation to longer-cycle offshore developments in regions such as Brazil, Guyana, Mozambique, and Namibia, is underpinning TechnipFMC's record Subsea order intake and high backlog, supporting visibility into sustained revenue growth over the coming years.

Curious what justifies that fair value gap? The narrative leans heavily on steady revenue expansion, firmer margins, and a future earnings multiple that assumes disciplined execution.

Result: Fair Value of $65.62 (OVERVALUED)

However, this hinges on oil and gas project spending holding up, and on geopolitical or project execution issues not hitting the Subsea backlog or margins.

Another valuation angle: multiples vs cash flows

Analysts see TechnipFMC as about 9% overvalued at $65.62 using their earnings based model, yet the SWS DCF model points to a fair value of $92.41, suggesting the stock trades at a 22.7% discount to estimated future cash flows. Which lens do you trust more when the signals conflict?

Next Steps

Mixed signals on value and growth potential can be hard to read, so move quickly, review the full data set, and weigh both the upside and the red flags with 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop at one stock, you might miss opportunities that fit your goals even better, so keep testing ideas and comparing options before committing fresh capital.

- Target long term wealth builders by reviewing companies with robust fundamentals using the solid balance sheet and fundamentals stocks screener (46 results).

- Hunt for value by scanning for quality stocks trading below their estimated worth through the 53 high quality undervalued stocks.

- Focus on resilience and sleep better at night by filtering for companies with steadier risk profiles via the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.