Assessing Teekay Tankers (TNK) Valuation After Earnings Beat And Supportive Analyst Ratings

Teekay Tankers Ltd Class A TNK | 0.00 |

Why Teekay Tankers (TNK) is drawing fresh attention

Teekay Tankers (TNK) is back on many watchlists after fourth quarter earnings and revenue came in ahead of analyst forecasts, followed by supportive analyst commentary that reinforced earlier positive ratings.

That earnings beat and the reaffirmed positive ratings have arrived alongside strong momentum, with a 21.77% 90 day share price return and a very large 5 year total shareholder return of 560.27%, which suggests sentiment has strengthened recently.

If this kind of strong move has your attention, it can be a good moment to see what else is setting up across the market through the 19 top founder-led companies.

With Teekay Tankers trading close to analyst targets after a strong run and an intrinsic value estimate that still implies a wide discount, the key question is simple: is there genuine value left here or is the market already pricing in future growth?

Most Popular Narrative: 19.9% Overvalued

The most followed narrative currently pegs Teekay Tankers' fair value at $67.80, below the last close of $81.27, which sets up a clear valuation gap.

Fair Value Estimate: revised up from $64.33 to $67.80, representing a modest uplift in the assessed share value. Revenue Growth: contraction assumption reduced from a 19.19% decline to a 14.58% decline, implying a less severe pullback in expected revenue.

Want to see what justifies a higher fair value despite projected revenue and earnings contraction, expanding margins, a higher future P/E and a steady discount rate? The full narrative lays out how these moving pieces fit together and why they still add up to that $67.80 figure.

Result: Fair Value of $67.80 (OVERVALUED)

However, this depends on tanker demand remaining strong, while slower projected oil demand and ongoing fleet renewal risks could still undermine the current valuation story.

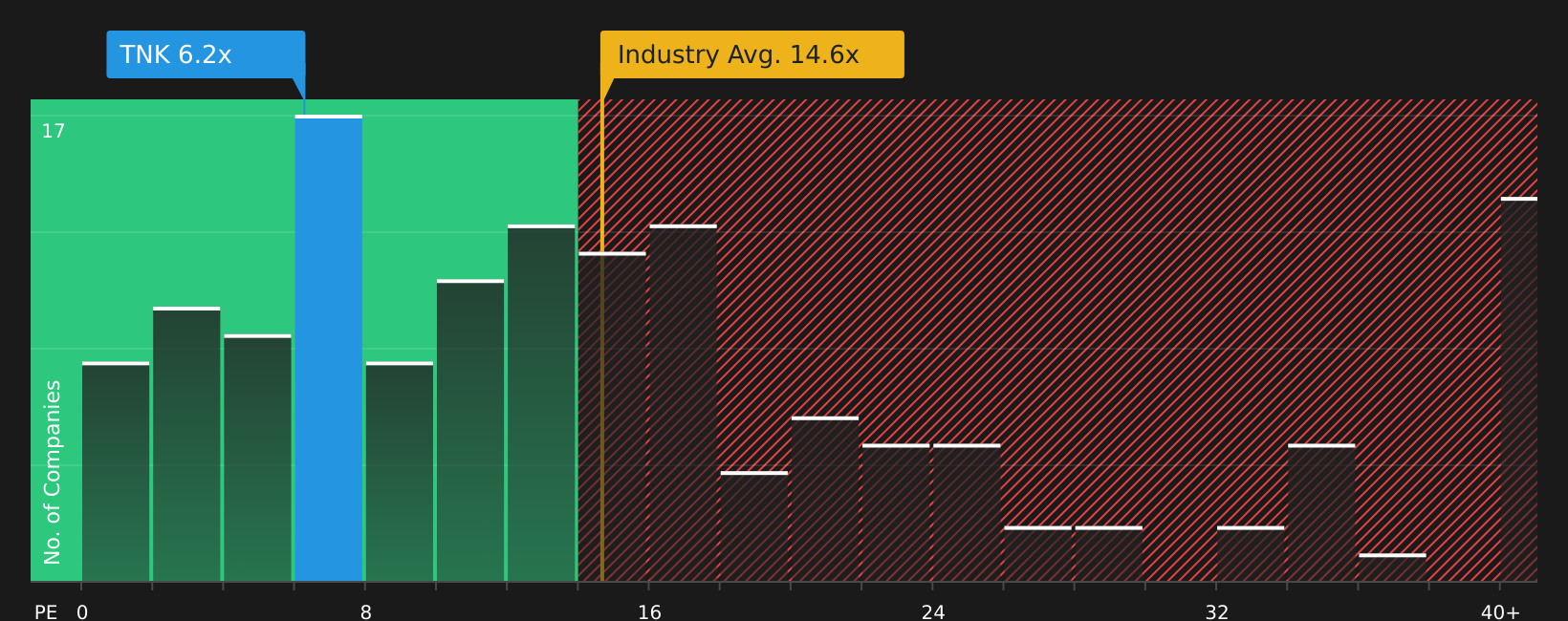

Another take using earnings multiples

The narrative model flags Teekay Tankers as 19.9% overvalued versus a $67.80 fair value. The current P/E of 8x screens as low compared with both the US Oil and Gas industry at 13.9x and peers at 10.2x, and it is also below a fair ratio of 13.3x.

That spread suggests the market is already building in meaningful earnings and cycle risk, which could limit downside if sentiment cools further. It also leaves less room if the tanker cycle softens faster than expected.

Next Steps

Mixed signals like these can be unsettling. To respond effectively, it can help to move quickly, review the numbers yourself, and weigh both sides using the 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Teekay Tankers has sharpened your focus, do not stop here. The next standout opportunity on your list could come from a very different corner of the market.

- Target stronger income potential by checking out companies built around generous cash returns through the 12 dividend fortresses.

- Hunt for quality at a discount by scanning stocks that combine appealing pricing with fundamentals using the 51 high quality undervalued stocks.

- Prioritize resilience first by focusing on companies with robust finances through the 72 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.