Assessing Teledyne Technologies (TDY) Valuation As Space And Defense Contracts Support Fresh Growth Momentum

Teledyne Technologies Incorporated TDY | 655.99 655.99 | +1.59% 0.00% Pre |

Teledyne Technologies (TDY) has just put fresh space and defense work into motion by starting production of infrared Focal Plane Modules for the Space Development Agency’s Tracking Layer Tranche 3 satellite program.

Those contract wins and product launches come as Teledyne Technologies’ share price sits at US$660.29, with a 30 day share price return of 13.51% and a 90 day share price return of 30.97%, alongside a 1 year total shareholder return of 34.83%. This performance suggests momentum has been building around the story in both the near term and over a longer holding period.

If this kind of defense and space activity has your attention, it could be a good moment to look across the wider supply chain with our screener of 25 power grid technology and infrastructure stocks as potential ideas beyond Teledyne.

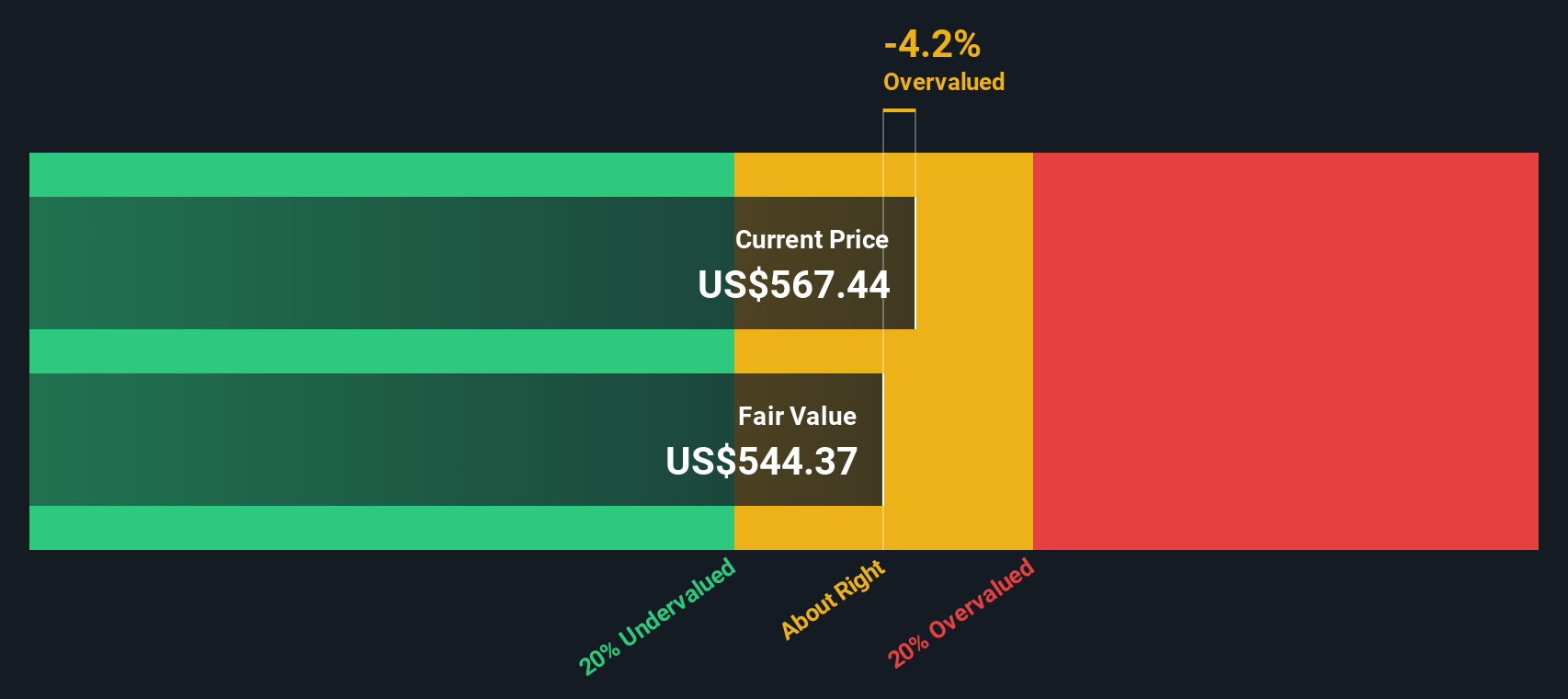

With the shares at US$660.29, a value score of 1, and an intrinsic value estimate sitting above the current price, investors now have to ask: is there still mispricing here, or is the market already baking in future growth?

Most Popular Narrative: 2% Undervalued

Teledyne’s most followed valuation narrative pegs fair value at about $674, just above the recent $660.29 close. This puts current enthusiasm to the test.

Strong defense, aerospace, and marine instrumentation demand, along with digital and sustainability trends, supports robust order growth and high-margin opportunities across Teledyne's core segments.

Successful acquisition integration and disciplined operational execution are driving higher-margin products, increased scale, and ongoing earnings and margin expansion.

Curious what kind of revenue path and margin profile sit behind that fair value line? The narrative leans on steady compounding, richer profitability, and a premium earnings multiple. Want to see exactly how those moving parts stack up against today’s price?

Result: Fair Value of $673.85 (UNDERVALUED)

However, there are still pressure points to watch, particularly if trade tensions, tariffs, and supply chain issues squeeze margins or if recent acquisitions take longer to improve profitability.

Another Angle On Valuation

Our DCF model points in the opposite direction to the $674 fair value narrative. On this view, Teledyne comes out at about $573 per share, which would make the current $660.29 price look expensive rather than slightly undervalued. Which set of assumptions do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Teledyne Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 54 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Teledyne Technologies Narrative

If you look at the numbers and reach a different conclusion, or simply prefer working from your own assumptions, you can build a tailored thesis in minutes with Do it your way.

A great starting point for your Teledyne Technologies research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Teledyne has piqued your interest, do not stop here. The screener can help you uncover other opportunities that might fit your portfolio just as well.

- Target potential mispricing by scanning our 54 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect their strengths.

- Build a steadier income stream by reviewing 13 dividend fortresses that combine higher yields with a focus on resilience.

- Sleep easier at night by checking 83 resilient stocks with low risk scores that screen for businesses with fewer red flags and more consistent profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.