Assessing Timken (TKR) Valuation As Leadership Restructuring Targets Technology And Regional Growth

Timken Company TKR | 0.00 |

Leadership shakeup puts technology and regional focus in the spotlight

Timken (TKR) is reworking its leadership chart, appointing a new chief technology officer and creating regional president roles. This move puts technology, AI and geographic execution more squarely in focus for shareholders.

These leadership changes come after a strong run in the shares, with a 90 day share price return of 28.79% and a 1 year total shareholder return of 27.83%. This suggests recent momentum around Timken's execution and growth plans.

If this kind of execution focused story interests you, it may be worth scanning aerospace and defense stocks for other industrial names with similar potential drivers.

With Timken trading at US$91.17, close to an average analyst price target of US$89.39 yet showing an indicated 4.4% intrinsic discount, investors might ask whether there is still upside potential or whether the market is already pricing in future growth.

Most Popular Narrative: 3% Overvalued

At a last close of US$91.17 versus a narrative fair value of US$88.49, the gap is small but still shapes how the setup is framed.

The analysts have a consensus price target of $83.952 for Timken based on their expectations of its future earnings growth, profit margins and other risk factors. In order for you to agree with the analyst's consensus, you would need to believe that by 2028, revenues will be $4.9 billion, earnings will be $474.3 million, and it would be trading on a PE ratio of 15.6x, assuming you use a discount rate of 9.0%.

Want to see what is baked into that fair value? The narrative leans heavily on steadier revenue progress, firmer margins and a future earnings multiple below many machinery peers. Curious how those ingredients fit together in detail?

Result: Fair Value of $88.49 (OVERVALUED)

However, you still need to weigh softer organic demand and tariff related cost pressure, which could keep margins and revenue from matching the current narrative.

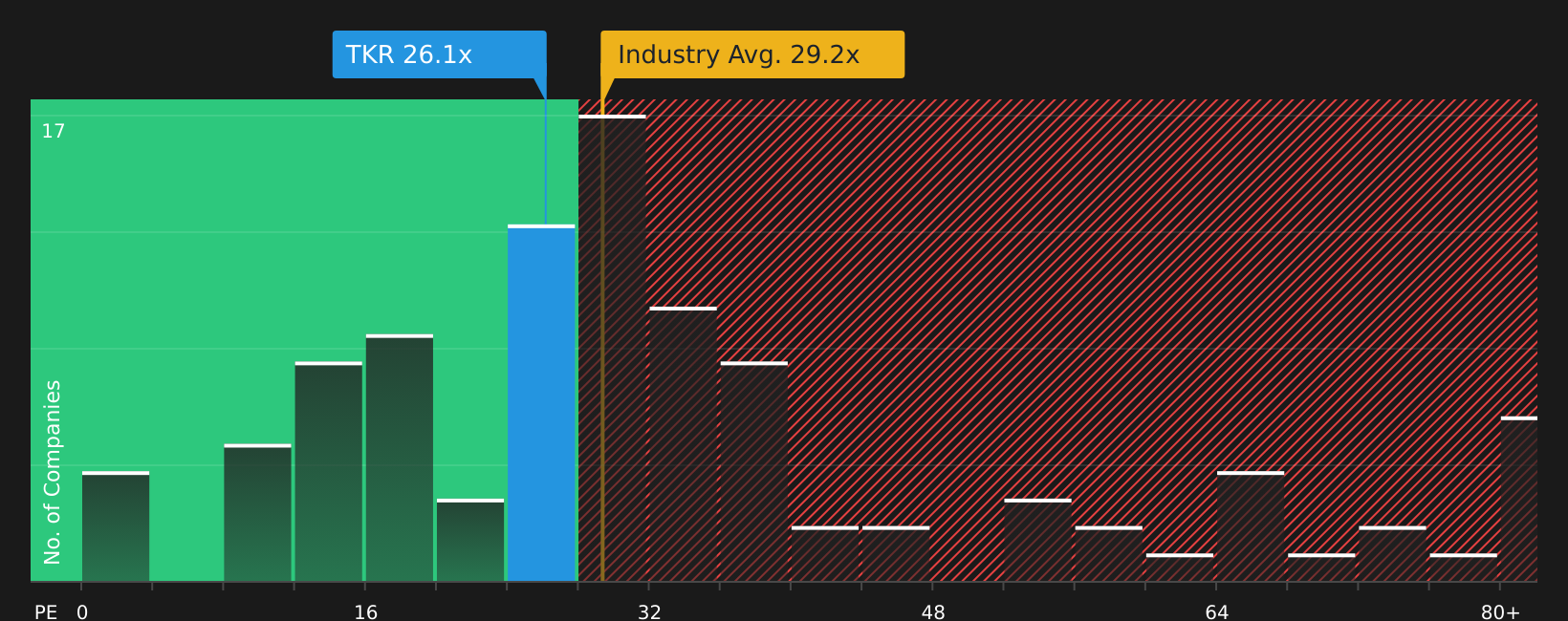

Another View: Market P/E Points To Value Support

While the narrative fair value suggests Timken is about 3% overvalued at US$91.17 versus US$88.49, the market multiples tell a different story. Timken trades on a P/E of 21.4x, compared with a fair ratio of 24.3x, the US Machinery industry on 26.3x, and peers on 35x.

That gap hints at some valuation cushion rather than excess optimism, even after the recent share price run. The question for you is whether those lower P/E levels simply reflect Timken’s softer past earnings trends and higher debt, or if the market is underpricing what the refreshed leadership and execution focus could deliver.

Build Your Own Timken Narrative

If this take does not fully line up with your own view, or you would rather test the numbers yourself, you can build a custom story for Timken in just a few minutes using Do it your way.

A great starting point for your Timken research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you like building your own view on Timken, do not stop here. A broader watchlist of fresh ideas can help sharpen your decision making.

- Tap into potential value by reviewing these 879 undervalued stocks based on cash flows that the market may not be fully paying attention to yet.

- Spot early movers in transformative computing by scanning these 29 quantum computing stocks for companies working at the edge of what is technically possible.

- Strengthen your income focus by checking out these 12 dividend stocks with yields > 3% that offer yields above 3% while you assess price risks and rewards.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.