Assessing Tyler Technologies (TYL) Valuation After New Chesterfield County Cloud Payments Deal

Tyler Technologies, Inc. TYL | 338.03 | +1.36% |

Why the Chesterfield County deal is on investors’ radar

Tyler Technologies (TYL) has just signed an agreement to become Chesterfield County, Virginia’s single payment processing partner, using its cloud based Tyler Payments and Payment Insights platforms for nearly 400,000 residents.

This new client win arrives as the market is watching upcoming fourth quarter earnings and existing analyst expectations on earnings per share. It gives investors fresh context for how the company’s public sector cloud offerings are being adopted.

The Chesterfield County win and recent cloud deployments, such as the Midland County CAD rollout, come as the share price trades at US$452.0 after a 1 day share price return of 2.0% and a 90 day share price return of an 8.97% decline. The 1 year total shareholder return of a 20.96% decline contrasts with a 48.13% total shareholder return over three years, suggesting longer term holders have seen stronger momentum than recent buyers.

If you are interested in how other software names are positioning around cloud and AI, this could be a good moment to look at high growth tech and AI stocks.

With earnings expectations firm and the stock trading at US$452.0 after a weaker 1 year stretch, are investors looking at an undervalued public sector software leader here, or is the market already pricing in future growth?

Most Popular Narrative: 28.7% Undervalued

With Tyler Technologies last closing at US$452.0 against a narrative fair value of about US$633.90, the valuation gap is built on detailed growth and margin assumptions that go well beyond the Chesterfield win.

The analysts have a consensus price target of $678.778 for Tyler Technologies based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $800.0, and the most bearish reporting a price target of just $585.0.

Curious what kind of revenue path, margin profile, and earnings power would support that kind of upside spread? The narrative lays out specific compounding assumptions and a rich future P/E that many investors will want to stress test for themselves.

Result: Fair Value of $633.90 (UNDERVALUED)

However, that upside case can quickly look fragile if government budgets tighten or large SaaS and cloud migration deals continue to arrive in irregular, less predictable waves.

Another Take on Valuation

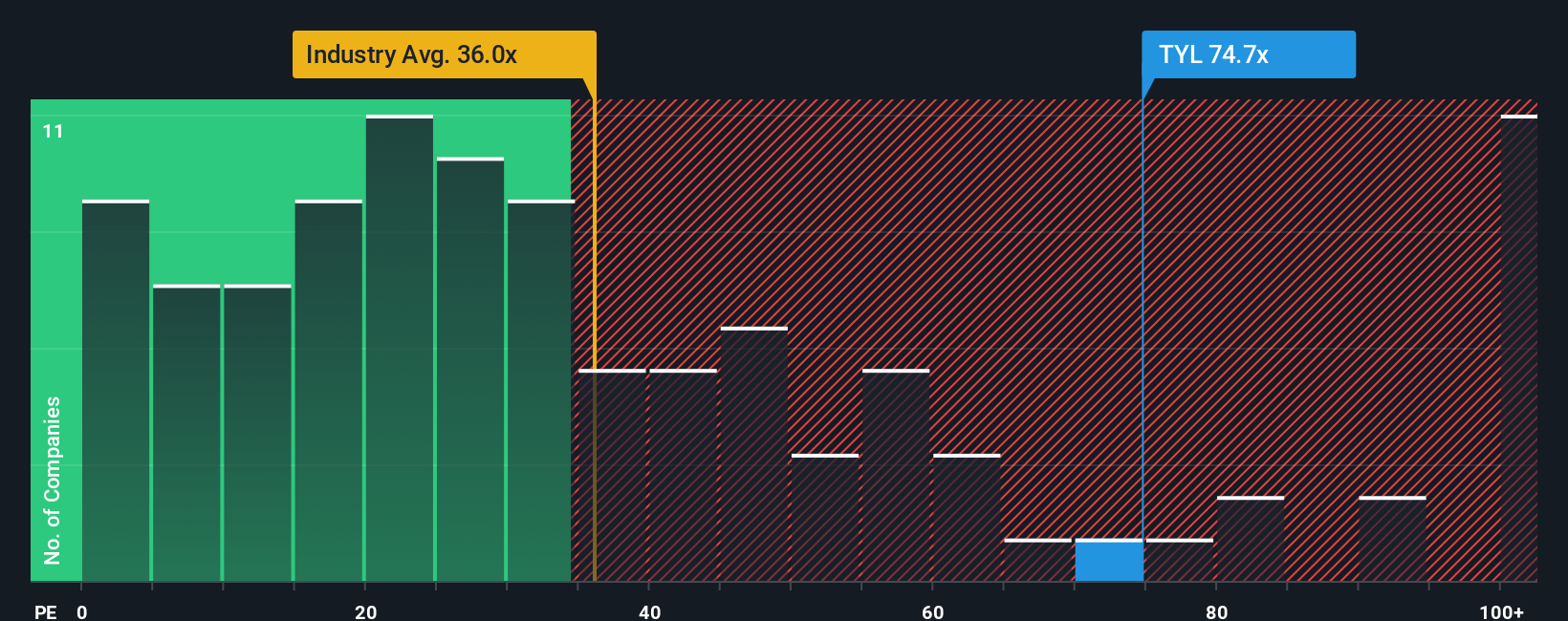

That 28.7% undervalued narrative sits awkwardly next to how the market is currently pricing Tyler on earnings. At a P/E of 61.7x versus 32.9x for the US Software industry and 34.1x for peers, and a fair ratio of 31.8x, the stock screens as expensive rather than cheap.

If the market eventually leans closer to that 31.8x fair ratio, it could mean less room for multiple expansion and more reliance on earnings growth to carry future returns. Does that make the narrative upside feel stretched to you, or just a premium you are comfortable paying for quality?

Build Your Own Tyler Technologies Narrative

If you are not fully on board with this view, or want to lean on your own work instead, you can quickly build a custom narrative in just a few minutes, Do it your way.

A great starting point for your Tyler Technologies research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Tyler has caught your attention, do not stop here. A few focused screens can quickly surface other opportunities that fit the style of portfolio you want to build.

- Target potential mispricings by checking out these 884 undervalued stocks based on cash flows that line up with your own expectations on cash flow strength and future earnings power.

- Ride long term technology shifts by scanning these 25 AI penny stocks that are tied to real business models rather than just headlines.

- Strengthen your income stream by reviewing these 12 dividend stocks with yields > 3% that may complement growth names like Tyler in a balanced portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.