Assessing UGI (NYSE:UGI) Valuation As Shares Weaken And Analysts See Potential Upside

UGI Corporation UGI | 0.00 |

Recent performance snapshot and business mix

UGI (UGI) has been under pressure recently, with the stock down about 4% over the past day, 6% over the past week, and 5% over the past month, while the past 3 months show a decline of roughly 9%.

Over longer horizons, total return is down about 11% over 5 years and about 4% over the past year, while the 3 year total return figure is reported at about 43%, giving investors a mixed performance profile depending on entry point.

At a recent close of US$33.56 and a market value of about US$7.5b, UGI sits in the mid cap range among US utilities, with operations that extend beyond its home market into international propane and LPG distribution.

The company reports annual revenue of about US$7.4b and net income of about US$641 million, with the latest year showing reported annual revenue growth of about 2% and net income growth of about 9%.

UGI organizes its business into several segments that give you a sense of how earnings are spread across different activities:

- Utilities, contributing about US$1.97b of revenue, including natural gas and electricity distribution in Pennsylvania

- AmeriGas Propane, at roughly US$2.16b, focused on propane distribution to residential, commercial, industrial, agricultural and motor fuel customers

- UGI International, at about US$2.03b, distributing LPG and related services across international markets

- Midstream & Marketing, at roughly US$1.67b, involved in pipelines, storage, gathering infrastructure and energy marketing

- Segment adjustments and eliminations, which reconcile intercompany activity and reduce the consolidated revenue figure

This mix means your exposure with UGI is not just to a regulated utility, but also to propane distribution, midstream assets and international LPG operations, each with its own risk and earnings pattern.

Recent trading has been weak, with the share price down over the past quarter and year to date. However, the 3 year total shareholder return of about 43% points to a much stronger earlier period.

If you are comparing UGI with other utilities and infrastructure related ideas, it can help to widen the lens and review 33 power grid technology and infrastructure stocks

With UGI’s share price under pressure, yet trading at a discount of about 29% to the average analyst price target and an intrinsic value estimate that sits well above the market, is this weakness a buying opportunity or is future growth already priced in?

Most Popular Narrative: 24.6% Undervalued

Compared with the last close at $33.56, the most followed narrative pegs UGI’s fair value at $44.50, implying meaningful upside if those assumptions hold.

Strategic investments in renewable natural gas (RNG) projects, bonus depreciation potential, and stronger regulatory incentives through recent legislation (e.g., the One Big Beautiful Bill Act) are expected to drive long-term EBITDA growth and improve net margins.

Curious what kind of revenue path, margin profile, and future earnings multiple support that $44.50 tag, especially when it incorporates a specific discount rate and an assumption of steady expansion in profitability.

The narrative applies a 7.22% discount rate and incorporates measured growth in both revenue and earnings margins, along with a future P/E that sits below the current US Gas Utilities industry level. It also rests on analysts being in broad agreement about UGI’s path, with a consensus target that stands well above the current price and assumes continued progress on operational efficiency, divestitures and capital deployment.

Result: Fair Value of $44.50 (UNDERVALUED)

However, this hinges on key risks, including ongoing LPG demand erosion in Europe and rising utility operating costs that could squeeze margins if rate relief disappoints.

Another view on UGI’s value

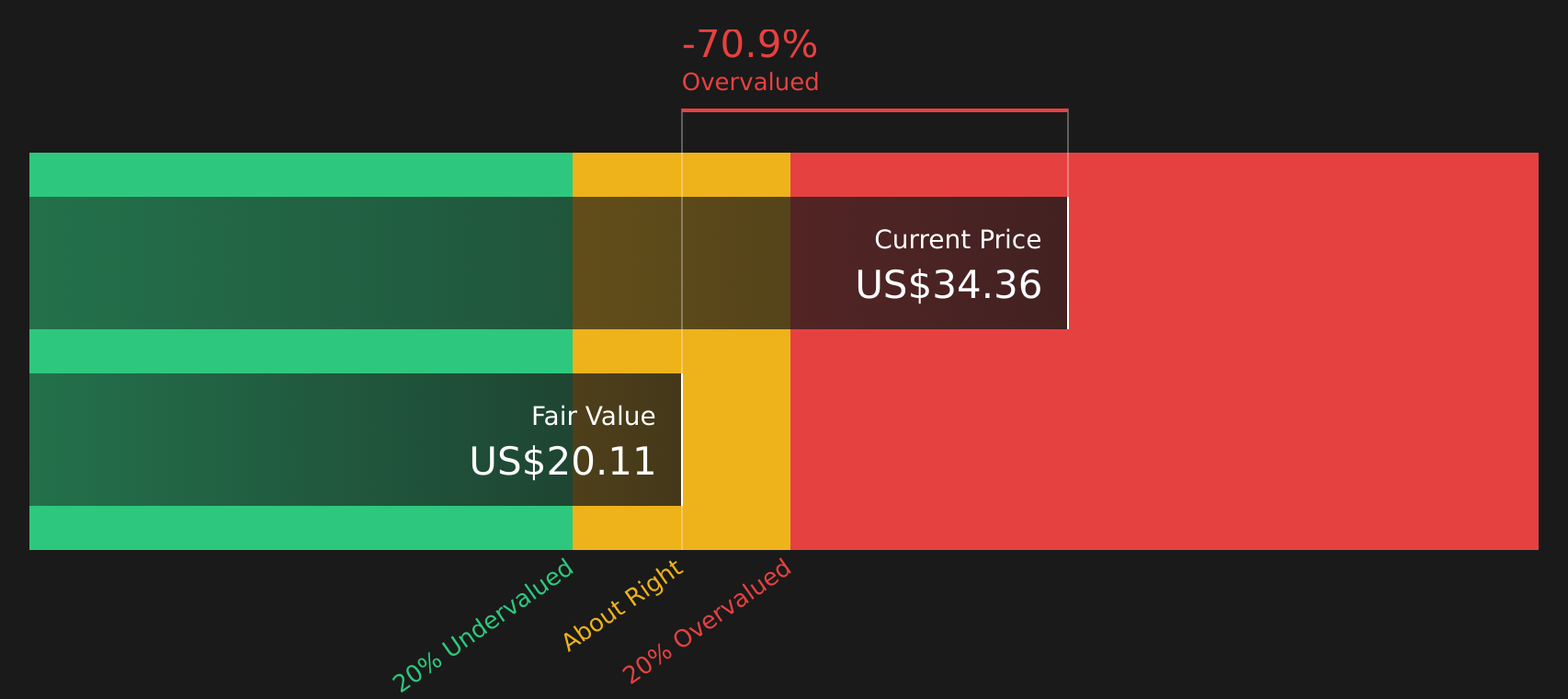

While the narrative fair value of $44.50 points to upside, the Simply Wall St DCF model tells a different story, with an estimate of $19.69 that sits well below the recent $33.56 share price. This raises the question of whether the market is overestimating future cash flows.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out UGI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment in this article leaning mixed, with both risks and rewards in play, move quickly to review the data yourself and weigh the 5 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you might miss out on other opportunities that better fit your goals, risk comfort, and preferred dividend or growth profile.

- Target reliable income and capital strength by reviewing companies in the 10 dividend fortresses.

- Hunt for quality at a reasonable price by scanning the 47 high quality undervalued stocks.

- Prioritize capital protection and steadier returns by assessing companies highlighted in the 62 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.