Assessing UGI (UGI) Valuation As Asset Sales Refocus The Business On Core Gas Profitability

UGI Corporation UGI | 0.00 |

Debt reduction, dividend focus and core gas profitability move into the spotlight

UGI (UGI) is reshaping its portfolio by selling non-core assets, directing the proceeds toward debt reduction and dividend support, while reporting improved profitability in its core natural gas and propane segments.

UGI's share price has softened in recent months, with a 7 day share price return of 6.8% and a 90 day share price return of 12.9%. At the same time, the 3 year total shareholder return of 39.4% signals that long term holders have still seen gains, suggesting sentiment is consolidating while the market weighs the impact of asset sales, debt reduction and core gas profitability.

If you are looking beyond utilities for your next idea, it could be a good moment to broaden your search and uncover 19 top founder-led companies

With UGI using asset sales to reduce debt and support its dividend, while the stock still trades below the average analyst price target, you need to ask whether there is genuine value here or whether the market already reflects future growth.

Most Popular Narrative: 20.9% Undervalued

UGI's most followed narrative pegs fair value at $44.50 per share, compared with the last close at $35.19, centering the story on earnings quality and capital deployment.

Divestiture of non-core, low-margin LPG assets and redeployment of proceeds into higher-return, regulated utility and energy services businesses enable greater financial flexibility, prudent deleveraging, and improved overall earnings quality.

Want to see what underpins that earnings upgrade story? The narrative leans on measured revenue growth, firmer margins, and a future profit multiple that implies rebuilt confidence in the business.

Result: Fair Value of $44.50 (UNDERVALUED)

However, you also need to factor in risks such as long term pressure on European LPG demand and ongoing customer attrition at AmeriGas, which could challenge this thesis.

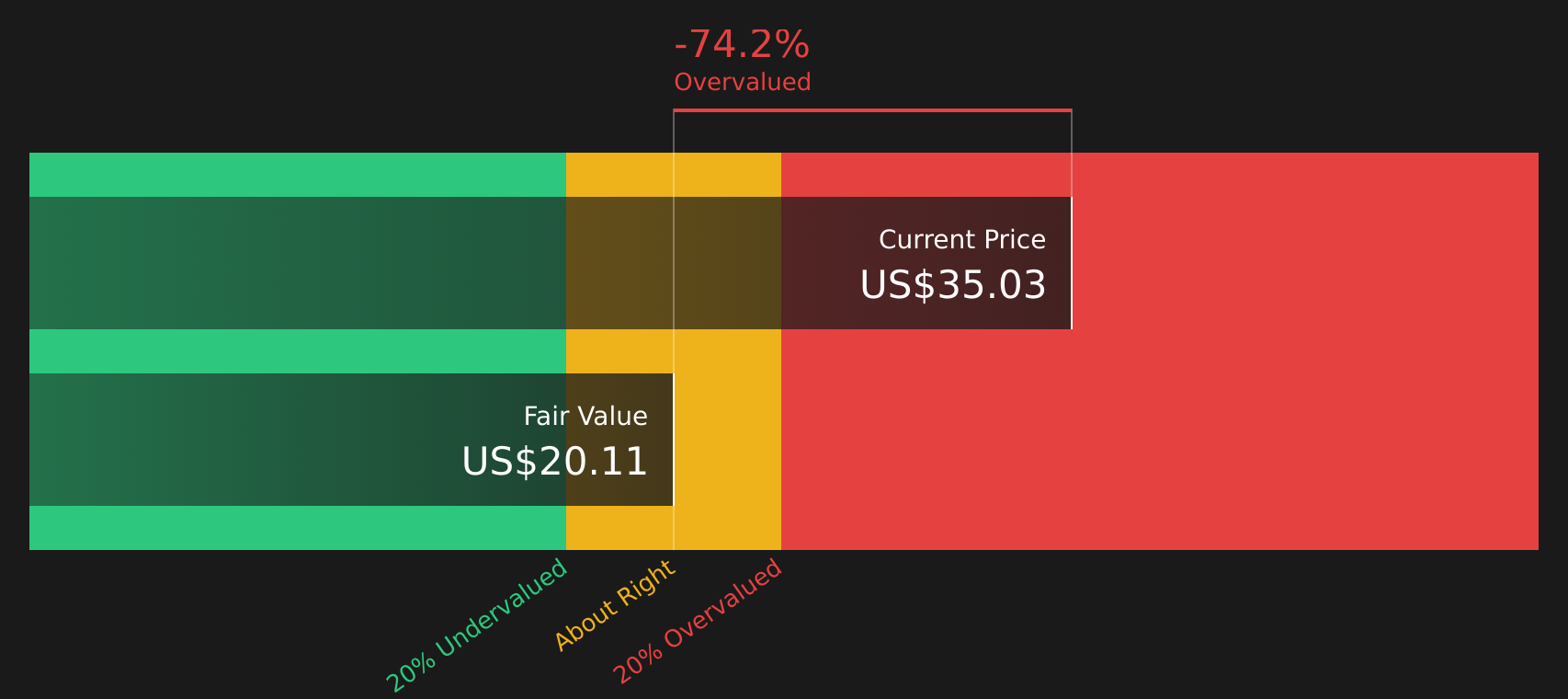

Another Angle on Value: Cash Flows Signal Caution

While the analyst narrative sees around 21% upside to a fair value of $44.50 per share, the SWS DCF model paints a different picture, with an estimated future cash flow value of $18.45. That gap suggests the key question is whether earnings quality or cash flow realism matters more for you right now.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out UGI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed on the story so far? Take a closer look at the numbers, compare the upside and downside, and weigh the 3 key rewards and 2 important warning signs.

Ready for more investment ideas?

If UGI has sharpened your focus, do not stop here. The Simply Wall Street Screener can quickly surface other stocks that fit the kind of profile you want.

- Pinpoint potential value opportunities by checking out 51 high quality undervalued stocks that combine quality fundamentals with room for a re-rating.

- Build a portfolio with staying power by scanning 72 resilient stocks with low risk scores that score well on resilience and downside protection.

- Get ahead of the crowd by reviewing a screener containing 25 high quality undiscovered gems that the market may not be watching closely yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.