Assessing UGI’s Valuation As Refinancing Strategy And Earnings Progress Draw Investor Focus

UGI Corporation UGI | 0.00 |

Why UGI’s refinancing and earnings update matter for shareholders

UGI (UGI) has drawn fresh attention after completing a US$500 million senior notes issue, together with a €300 million offering by its subsidiary, while posting slightly higher quarterly revenue and net income and reaffirming its dividend.

Despite the refinancing news and earnings update, UGI’s 90 day share price return is down 12.31% and its year to date share price return is down 9.67%, while the 3 year total shareholder return of 42.13% points to stronger longer term momentum.

If you are reassessing your utilities exposure after UGI’s refinancing, it can help to compare it with other infrastructure focused opportunities, including 38 power grid technology and infrastructure stocks

With UGI’s share price weaker over the past year, analyst targets sitting higher than the current US$33.99 level and earnings still positive, the key question is whether this refinancing reset leaves the stock undervalued or if markets are already pricing in future growth.

Most Popular Narrative: 23.6% Undervalued

UGI’s most followed narrative places fair value at $44.50, above the last close of $33.99, and ties that gap to long term grid and energy investments.

Anticipated implementation of new, higher utility rates in Pennsylvania, pending regulatory approval, will provide substantial incremental revenue beginning in fiscal 2026, supporting continued investment in grid resiliency and modernization.

Strategic investments in renewable natural gas (RNG) projects, bonus depreciation potential, and stronger regulatory incentives through recent legislation (e.g., the One Big Beautiful Bill Act) are expected to drive long-term EBITDA growth and improve net margins.

Want to understand why this narrative supports a higher valuation gap to today’s price? It leans on steady revenue gains, rising margins, and a future earnings multiple that sits below many peers. Curious which specific growth rates, profitability targets, and discount rate are doing the heavy lifting in that $44.50 figure? The full narrative lays out those assumptions step by step.

Result: Fair Value of $44.50 (UNDERVALUED)

However, you still need to weigh risks such as long term LPG demand erosion in Europe and ongoing customer attrition at AmeriGas, which could pressure margins.

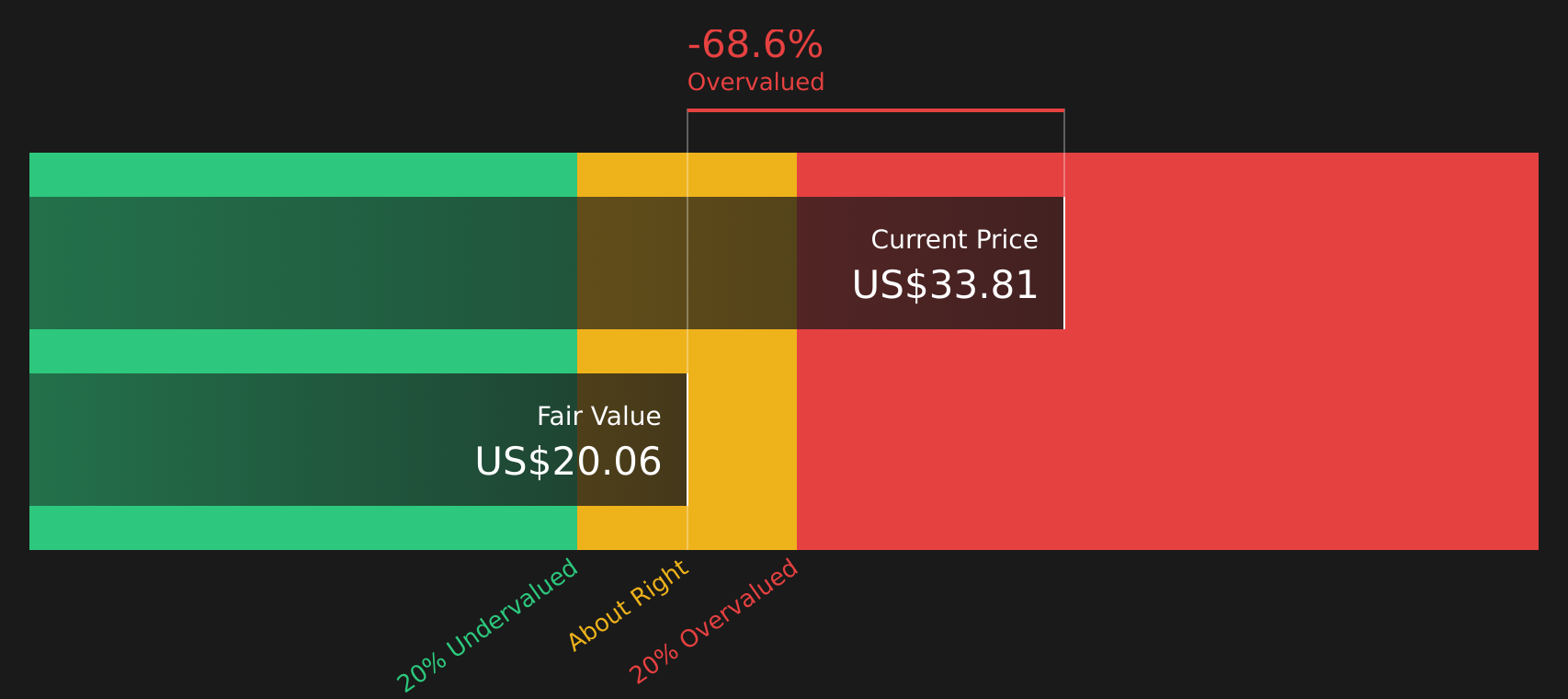

Another View: Cash Flows Paint a Tougher Picture

While the popular narrative suggests UGI is 23.6% undervalued with a fair value of $44.50, the Simply Wall St DCF model points the other way, with an estimated future cash flow value of $19.48 and the stock at $33.99, which implies UGI is trading above that cash flow based estimate.

This gap between earnings based optimism and cash flow caution raises a simple question for you: which set of assumptions feels closer to how UGI will actually fund and grow its business over time?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out UGI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such a mixed set of signals around value, risk, and future cash flows, it makes sense to look through the numbers yourself and decide quickly where you stand by weighing the 5 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you might miss opportunities that better fit your goals, risk comfort, or income needs. Consider widening your view with targeted ideas.

- Spot potential value opportunities before the crowd by reviewing 50 high quality undervalued stocks that combine solid fundamentals with room for rerating.

- Build a steadier income stream by focusing on 12 dividend fortresses that aim for higher yields with an emphasis on resilience.

- Prioritise capital protection by concentrating on 66 resilient stocks with low risk scores that score well on financial strength and earnings stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.