Assessing United Natural Foods (UNFI) Valuation After Strong Share Gains And Mixed Fair Value Signals

United Natural Foods, Inc. UNFI | 0.00 |

Recent performance snapshot

United Natural Foods (UNFI) has drawn fresh attention after a period of strong share price movement, with the stock up 4.8% in the past day and 8.1% over the past week.

Over the past month the stock has returned 7.2%, while the past 3 months show a much larger gain of about 52%. Year to date, United Natural Foods has returned 66.1%, and over the past year the total return is 99.3%.

Looking further back, the 3 year total return is very large at about 17x, while the 5 year total return is 56.8%. These figures frame a company that has already experienced substantial share price movement before today.

The recent 90 day share price return of 52.23% and 1 year total shareholder return of 99.28% point to building momentum, with the latest close at $55.52 adding to that trend.

If you are looking beyond a single distributor, this could be a good moment to broaden your search and check out 21 top founder-led companies

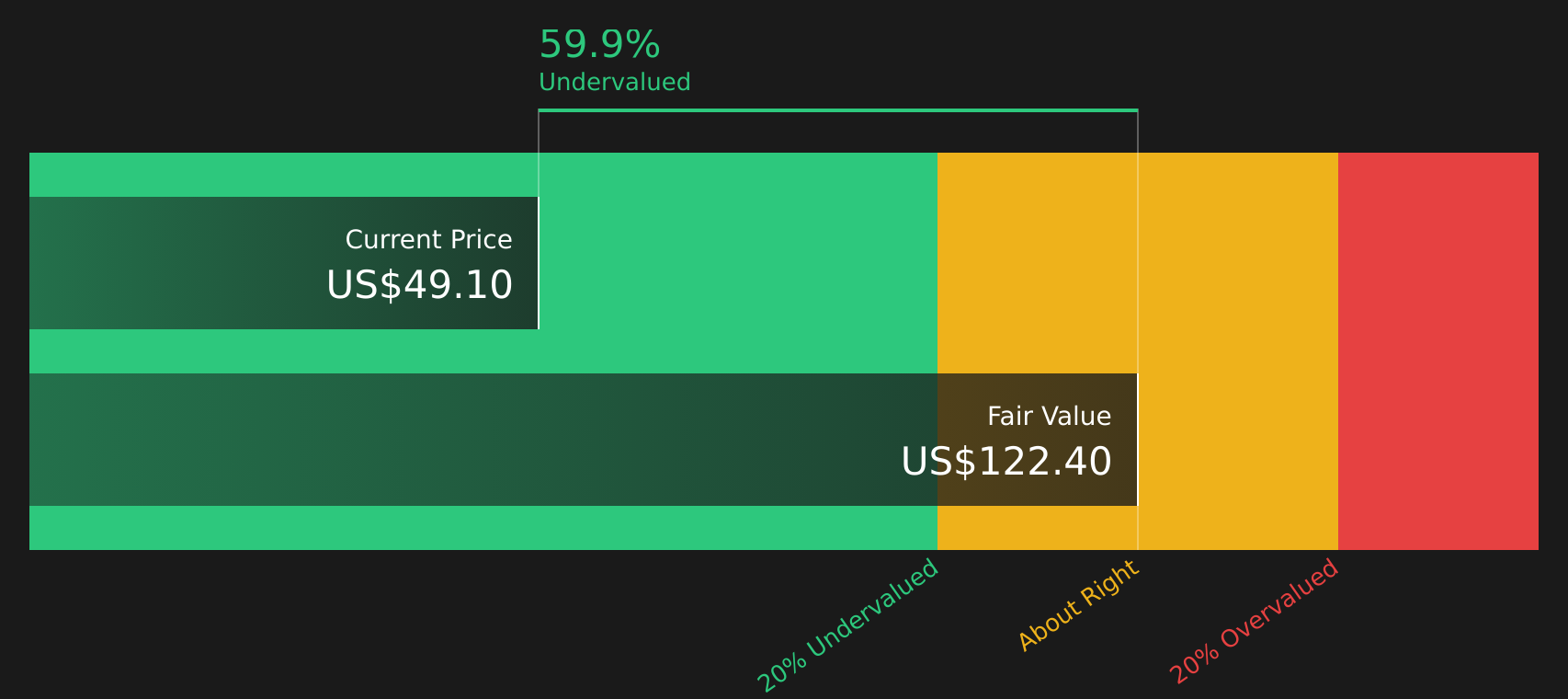

With United Natural Foods trading at $55.52 against an analyst price target of $46.25, but with a modelled intrinsic value implying about a 52% discount, should you interpret this as a potential buying opportunity or conclude that the market is already pricing in future growth?

Most Popular Narrative: 20% Overvalued

Against the latest narrative fair value of $46.25, United Natural Foods at $55.52 sits above that mark, and the valuation hinges on how much of the efficiency story is already reflected in the price.

The continued consolidation among food retailers and the expansion of differentiated, specialty, and e-commerce grocery models increases the value of scaled, flexible distributors like UNFI, allowing the company to win new business and further outpace industry benchmarks, driving incremental revenue and EBITDA growth as the sector evolves.

Want to see what revenue path, margin rebuild, and future profit multiple sit behind that fair value? The narrative leans on a detailed earnings roadmap, layered with assumptions about how cash flows compound if execution stays on track.

Result: Fair Value of $46.25 (OVERVALUED)

However, the recent cybersecurity breach and the exit from the Key Food contract could still unsettle customer relationships and challenge the efficiency-driven narrative.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another view: cash flows tell a different story

While the analyst narrative suggests United Natural Foods at $55.52 is about 20% above the $46.25 fair value, our DCF model presents a very different picture. It indicates a future cash flow value of $115.23, which implies the stock trades at a steep discount. Which signal do you put more weight on: a cautious earnings multiple or a richer cash flow outlook?

Next Steps

With such a mixed picture on valuation and recent events, it makes sense to move quickly, review the data yourself, and weigh both the upside and the risks. You can start with 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that better fit your goals, risk comfort, and income needs.

- Target resilient companies by checking out the 64 resilient stocks with low risk scores that may help you focus on steadier balance sheets and earnings profiles.

- Hunt for potential value opportunities by scanning the 49 high quality undervalued stocks and compare how their fundamentals line up with your expectations.

- Strengthen your income watchlist by reviewing the 9 dividend fortresses that prioritise yield alongside financial stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.