Assessing Viasat (VSAT) Valuation After Unified Global Ka-Band Network Fuels Strong Share Momentum

ViaSat, Inc. VSAT | 53.69 | +18.70% |

What Viasat’s latest satellite move could mean for the stock

Viasat (VSAT) recently launched a unified global Ka-band satellite network for government and military customers, an operational milestone that arrives alongside a period of strong share performance and a fresh 52-week high.

The Ka-band launch has arrived during a clear upswing in investor sentiment, with a 30-day share price return of 17.01% and a very large 1-year total shareholder return of 376.52%, even though the 5-year total shareholder return sits at a loss of 24.82%. This suggests that recent momentum has picked up after a tougher longer stretch.

If this kind of satellite story has your attention, it could be a good moment to see what else is moving across aerospace and defense stocks.

With Viasat trading around $44.03, sitting above the average analyst price target yet showing a very large intrinsic discount estimate of about 61%, you have to ask yourself whether this is a genuine mispricing or whether the market is already baking in years of growth.

Most Popular Narrative: 7.1% Overvalued

The most followed narrative pegs Viasat’s fair value at $41.13, a bit below the recent $44.03 close. This sets up a clear valuation tension.

The analysts have a consensus price target of $24.286 for Viasat based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $52.0, and the most bearish reporting a price target of just $10.0.

Curious how a business with ongoing losses, modest revenue growth, and a higher future earnings multiple still arrives at that fair value band? The full narrative spells out the exact revenue path, margin shift, and discount rate that need to line up to support that price.

Result: Fair Value of $41.13 (OVERVALUED)

However, you also have to weigh ongoing heavy capital spending and intense competition in broadband and satellite services, which could challenge the fair value story that investors are watching.

Another angle on Viasat’s value

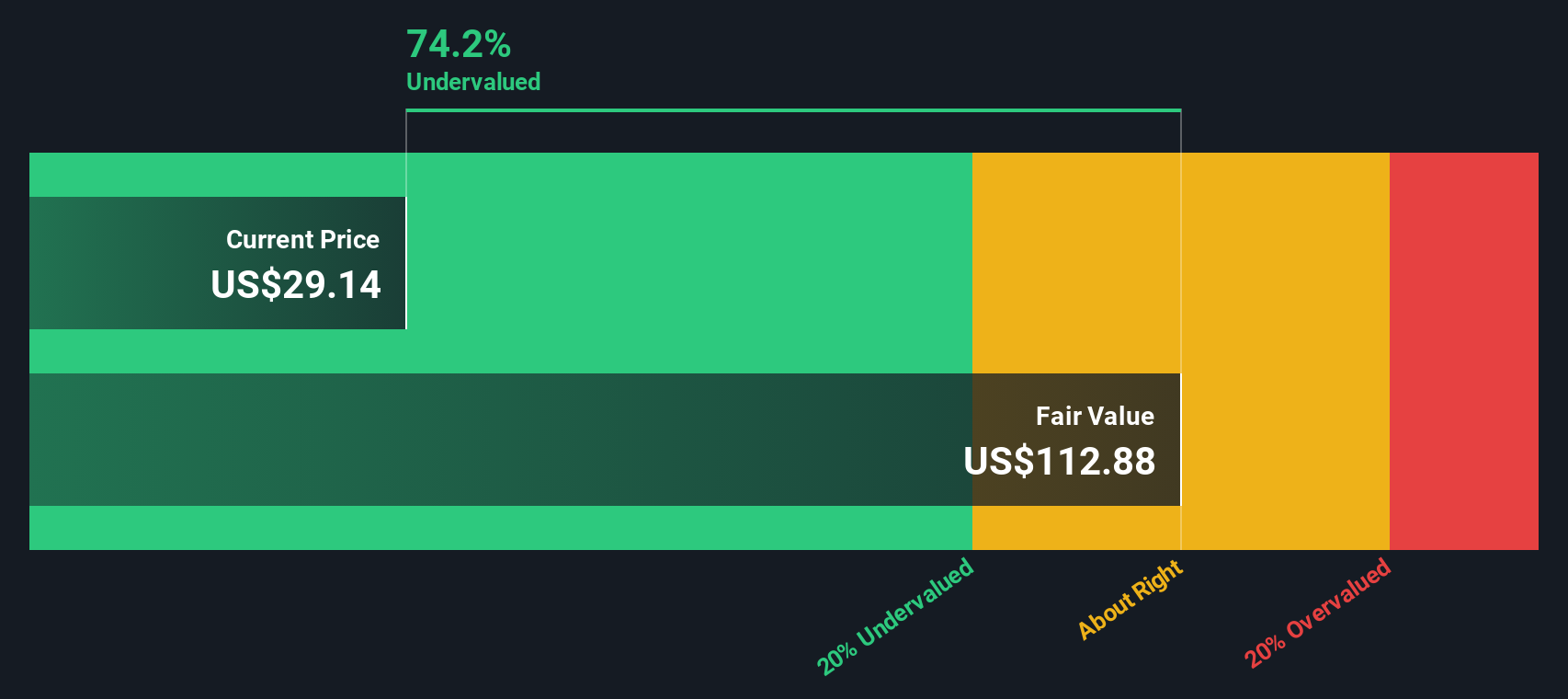

While the most popular narrative suggests Viasat is 7.1% overvalued at $44.03 versus a $41.13 fair value, our DCF model lands in a very different place, with an estimated future cash flow value of $113.44. That is a big gap. Which story do you trust more?

Build Your Own Viasat Narrative

If you look at these numbers and reach a different conclusion, or simply prefer to rely on your own work, you can build a personalised view in minutes starting with Do it your way.

A great starting point for your Viasat research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Viasat has sharpened your interest, do not stop here. Widen your research and pressure test your thesis against a broader set of opportunities on Simply Wall St.

- Target potential turnaround stories by reviewing these 3531 penny stocks with strong financials, which pair low share prices with stronger underlying financials.

- Tap into the AI trend by scanning these 25 AI penny stocks, which link artificial intelligence themes with smaller names.

- Zero in on value by checking these 873 undervalued stocks based on cash flows, which screens for companies priced below their estimated cash flow worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.