Assessing W. R. Berkley (WRB) Valuation After Insider Buying And Steady Earnings

W. R. Berkley Corporation WRB | 65.99 | +1.09% |

Insider buying and steady earnings put W. R. Berkley in focus

W. R. Berkley (WRB) is back on investors’ radar after fresh insider buying from Mitsui Sumitomo and a new earnings report that paired steady operating results with a slight revenue shortfall versus expectations.

At a share price of US$67.77, W. R. Berkley’s recent moves, including continued buybacks and steady quarterly earnings, come after a softer 90 day share price return of 8.48% alongside a 1 year total shareholder return of 16.9%. This suggests longer term holders have seen stronger momentum than more recent buyers.

If you are comparing W. R. Berkley with other insurance names, it can be useful to see how it stacks up against a wider set of solid balance sheet and fundamentals stocks screener (None results).

With the share price sitting close to analyst targets, and insider buying together with long running buybacks in the mix, the key question is whether W. R. Berkley is still mispriced or if the market already recognizes its future growth.

Most Popular Narrative: 3.6% Undervalued

With W. R. Berkley closing at $67.77 against a narrative fair value of $70.31, the current price sits slightly below that long term view and puts the spotlight on what is driving that gap.

The expanding complexity of global business and assets is driving strong demand for specialty insurance solutions, with record net written premiums and broad-based growth across all lines positioning W. R. Berkley to continue increasing revenue.

Digital transformation and the rise of technology-driven exposures (e.g., cyber, tech E&O) are prompting clients to seek innovative products, providing high-margin growth opportunities that W. R. Berkley, with its specialty focus and decentralized, agile underwriting model, is well positioned to capture, supporting future earnings.

Want to see what sits behind that valuation gap? The most followed narrative leans on steady earnings progress, tight margins, and a future earnings multiple that has to do some heavy lifting.

At the core of this fair value is a set of analyst assumptions about W. R. Berkley’s revenue, earnings and profit margins over the next few years, alongside a specific discount rate of 6.956% used to bring those future cash flows back to today’s dollars.

Analysts behind the narrative expect modest earnings growth from around $1.8b to about $2.0b by 2028, with profit margins edging higher but revenue essentially flat, and they pair that with a slightly higher future P/E than the broader US insurance group to arrive at the $70.31 fair value.

They are also assuming a small reduction in the share count over time, which supports earnings per share, and acknowledge that recent updates have trimmed earlier fair value estimates, reflecting more cautious assumptions on long term revenue trends, margins and the multiple investors may be willing to pay.

Result: Fair Value of $70.31 (UNDERVALUED)

However, there are real watchpoints here, including softer P&C pricing and the risk that higher loss costs or competition could squeeze margins and challenge those earnings assumptions.

Another View: Market Ratios Tell a Different Story

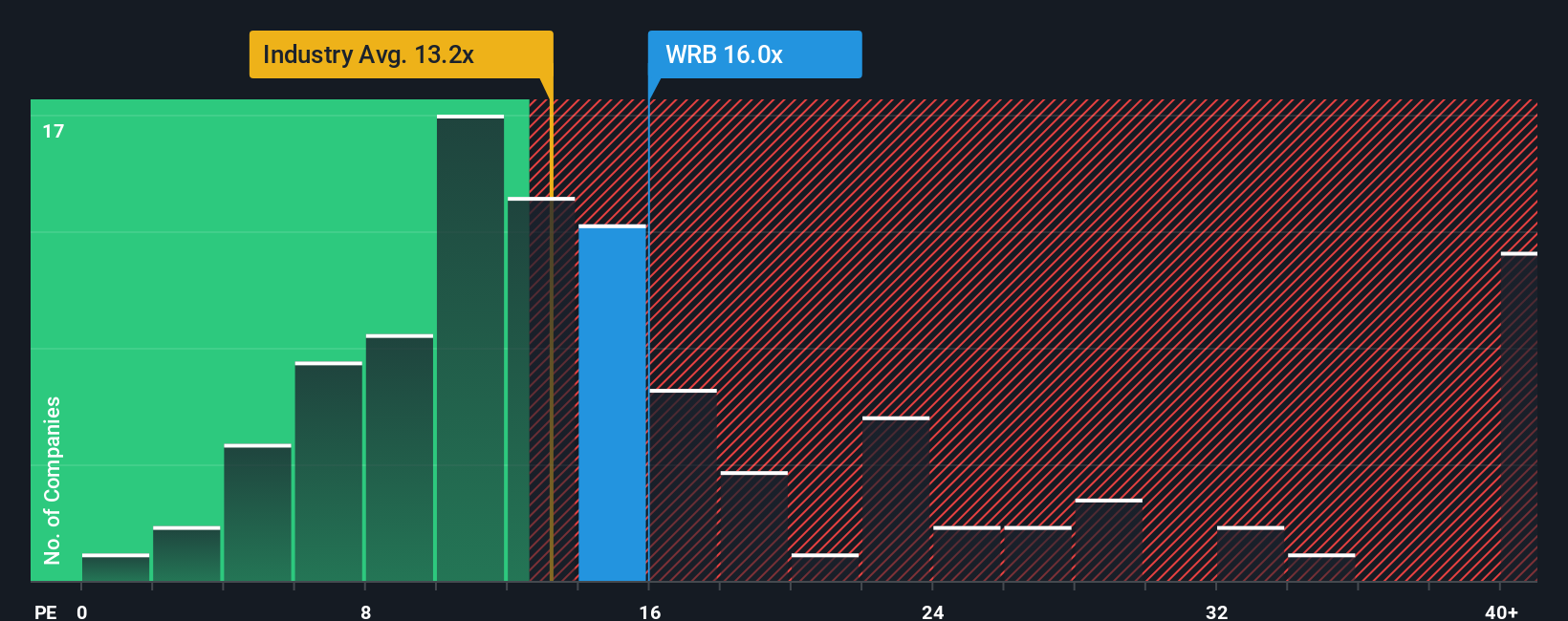

While the fair value narrative points to a 3.6% undervaluation, the market’s preferred yardstick sends a cooler signal. W. R. Berkley trades on a P/E of 14.4x versus 13.2x for the wider US insurance group and a fair ratio of 12.8x, which implies you are already paying a premium. So is this a margin of safety or a margin of error?

Build Your Own W. R. Berkley Narrative

If you look at the numbers and reach a different conclusion, or just prefer your own research, you can build a custom view in minutes with Do it your way.

A great starting point for your W. R. Berkley research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you stop at a single stock, you could miss opportunities that fit your style even better, so take a few minutes to scan a broader set of ideas.

- Spot potential turnarounds early by checking out these 3533 penny stocks with strong financials that pair smaller market caps with stronger financials than you might expect.

- Explore technology themes by reviewing these 24 AI penny stocks, which focus on companies tied to artificial intelligence and present key fundamentals up front.

- Hunt for value by reviewing these 872 undervalued stocks based on cash flows, which highlights stocks priced below what their cash flows may justify based on this methodology.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.